Think Bitcoin™ Issue #34

Why you shouldn't have to invest to be wealthy (an ode to saving money); why Bitcoin is different from "crypto"; debunking environmental FUD; decentralization vs. correlation

Hey friends, welcome back to Think Bitcoin™ for issue #34. Special welcome to the new subscribers. I’m glad you’re here. As always, if you have any questions or comments, feel free to reach out. You can also find me on Twitter (@TheWhyOfFI).

In this issue:

Long Reads: Why saving should be easier than investing

Content Round-Up: 3 articles, 1 Twitter thread

FAQ: Dispelling some common confusion about the difference between decentralization and correlation

As always, if you find this newsletter interesting or useful, please share it with others who might find it interesting or useful, too!

Long Reads

You Shouldn’t Have to Invest: An Ode to Saving Money

If you’ve spent any time in the personal finance / FIRE space you’re almost certainly familiar with the popular and widely proclaimed tenet that one cannot save one’s way to wealth; that, rather, one must invest to achieve wealth.

Scroll through the Instagram accounts of popular finfluencers and you will encounter a plethora of colorful graphics and charts underlining the paltry yield one makes on a savings account versus the divinely guaranteed 7% return one can expect to make in the stock market every year.

These posts invite the viewer/scroller to draw the obvious, unimpeachable conclusion that the only way to get wealthy is to invest. Savings = bad. Investments = good. This formulation has never really been questioned because, in our current economic environment, it is unassailably true.

We celebrate how easy investing has become. It’s so easy, everyone can do it!

This, of course, has helped create the booming industry of personal finance, with its panoply of coaches, advisors, and gurus. Empowered by the discovery of how easy investing truly is, these acolytes now charge for one-on-one sessions to share a historical chart of the S&P and point you in the direction of a Vanguard account. Some charge hourly rates equivalent to those of partners at white shoe law firms.

In the personal finance space, “investing” is often contrasted with “gambling,” with the former meaning simply to hold an investment for a long time and the latter referring to day-trading and shorter term stock picking. In practice, however, these concepts, as understood and implemented in the personal finance space, are less distinguishable. No one is really doing security analysis, reading SEC filings, etc. Instead, one is just sanctimoniously anointed as an investor if one simply buys and holds index funds no matter what price they’re trading at, and one is even more sanctimoniously maligned as a gambler if one does anything else.

I want to turn this orthodoxy on its head and question the underlying tenet about saving versus investing. What does it say about money when simply saving it is a losing enterprise? What does it say about money when every single earner who wants to grow or merely sustain his or her wealth must step out onto the risk curve and invest? And what does it say about our collective psychology, with respect to money, if we all know saving is, oxymoronically, a sure way to lose purchasing power?

I would argue that this simply illustrates the fundamental flaw of fiat currency, which is that it debases the currency so thoroughly that everyone is forced to become an investor and be thankful for the privilege. Because fiat money bleeds purchasing power (as a result of inflationary monetary policies), merely saving money won’t grow or even preserve wealth.

But saving should create wealth, or at the very least preserve it. And everyone should not have to invest.

Not only should investing not be easy; it should be difficult. Not difficult in terms of access, but difficult in terms of execution. And it should not carry the illusion of being low-risk or risk-free, no matter its iteration or implementation. Because when investing is “easy” what this really means is that more people can price-insensitively shovel money into the market or gamble it on meme stocks and shitcoins. Statements like “it’s never been easier to invest,” are ridiculous. Sure, access to investing is easier, but nothing about actual security analysis has become easier. And if, by “investing,” we mean something akin to the “effective, efficient, creative, and differentiated allocation of capital”1, then we haven’t made investing any easier at all.

We’ve sort of just made risk-taking easier and more palatable and celebrated it as an achievement for the little guy. The modern necessity that everyone be an investor to preserve or grow his/her wealth, coupled with the crop of tools and exchanges developed to service (and profit from) this necessity, paints it with a veneer of egalitarianism that tends to blind us to the downstream effects of such “achievements,” and prevents us from coalescing around a real achievement, which would be making saving effective.

Before discussing how Bitcoin seeks to fix saving, let’s briefly examine some of the negative downstream effects of everyone being an investor and indiscriminately piling money into index funds:

First, this type of investing is almost entirely price-insensitive. I would further argue that it’s largely strategy-insensitive, too. This makes markets less efficient. When a growing percentage of the market is doing this type of passive investing into index funds, companies that are already large get rewarded with the most incremental dollars. In a market-weighted S&P index fund, for example, roughly 25% of the dollars coming in are going toward shares of the 10 biggest companies.

This investment money is not going to those companies because these passive investors perceive them to be mispriced or because of some data- or sentiment-based thesis. This outsized proportion of each incremental dollar is going to those companies simply and solely because of their size.

It’s worth continuously noting that the only signals index funds receive are “buy” when money comes in and “sell” when money is taken out. There is no analysis, no diligence, no thought, and no strategy. When money comes in, that sends a “buy” signal and securities are purchased in proportion to their weight in the index. The world could be burning down to the ground, but as long as an index fund is receiving inflows, it’s buying securities.

On a large scale, this seriously degrades (and, arguably, totally destroys) any conception of efficient markets. Both Mike Green and Allen Farrington have written and discussed this point.

But most people have day jobs that do not involve investing and finance. The average American possesses neither the time nor the skills to analyze companies and actively manage a portfolio like an investment professional.

Back in the day this problem was solved by turning your money over to a professional money manager who charged you an exorbitant fee. Then Jack Bogle came along and gave us the low-cost index fund, which, though a markedly better option than the high-fee money managers, is still merely the best bad option to address the more fundamental and seemingly unaddressable problem of saving money (as opposed to investing it) being disincentivized and punished.

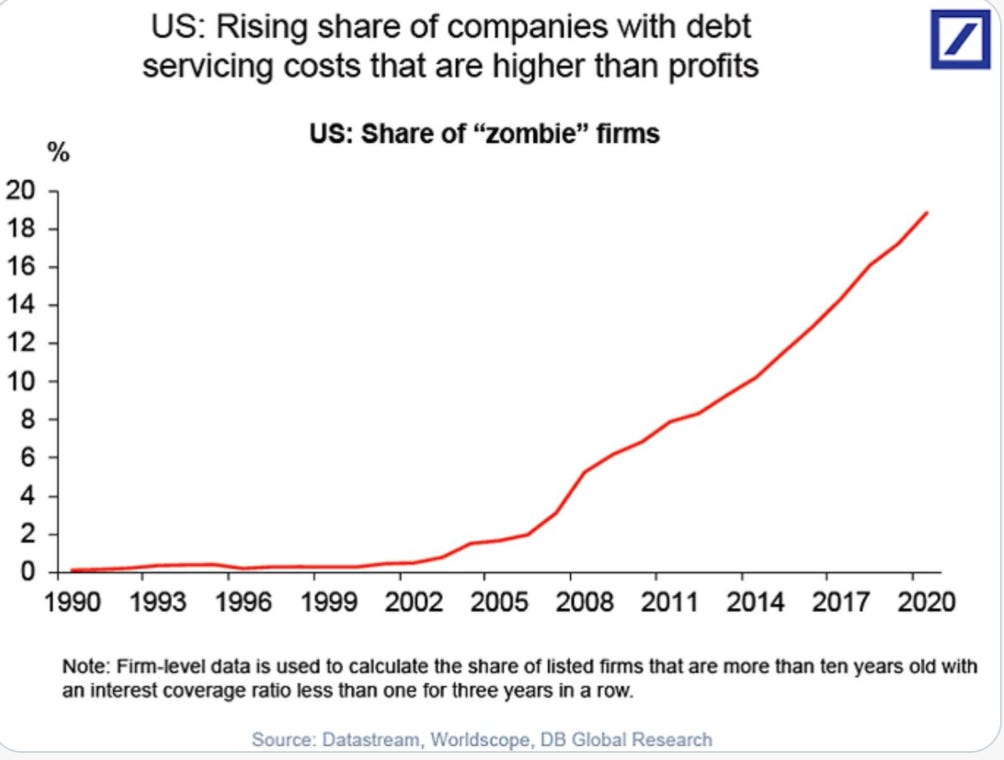

The second big problem is that this environment encourages and perpetuates widespread malinvestment. When everyone is throwing money at indexes, firms within an index that are unprofitable and over-leveraged are propped up by the inflows.

This is why we’ve seen an increasing amount of zombie companies. Roughly 25% of the companies in the Russell 3000, for example, are zombie companies.

Needless to say, malinvestment is not good for markets.

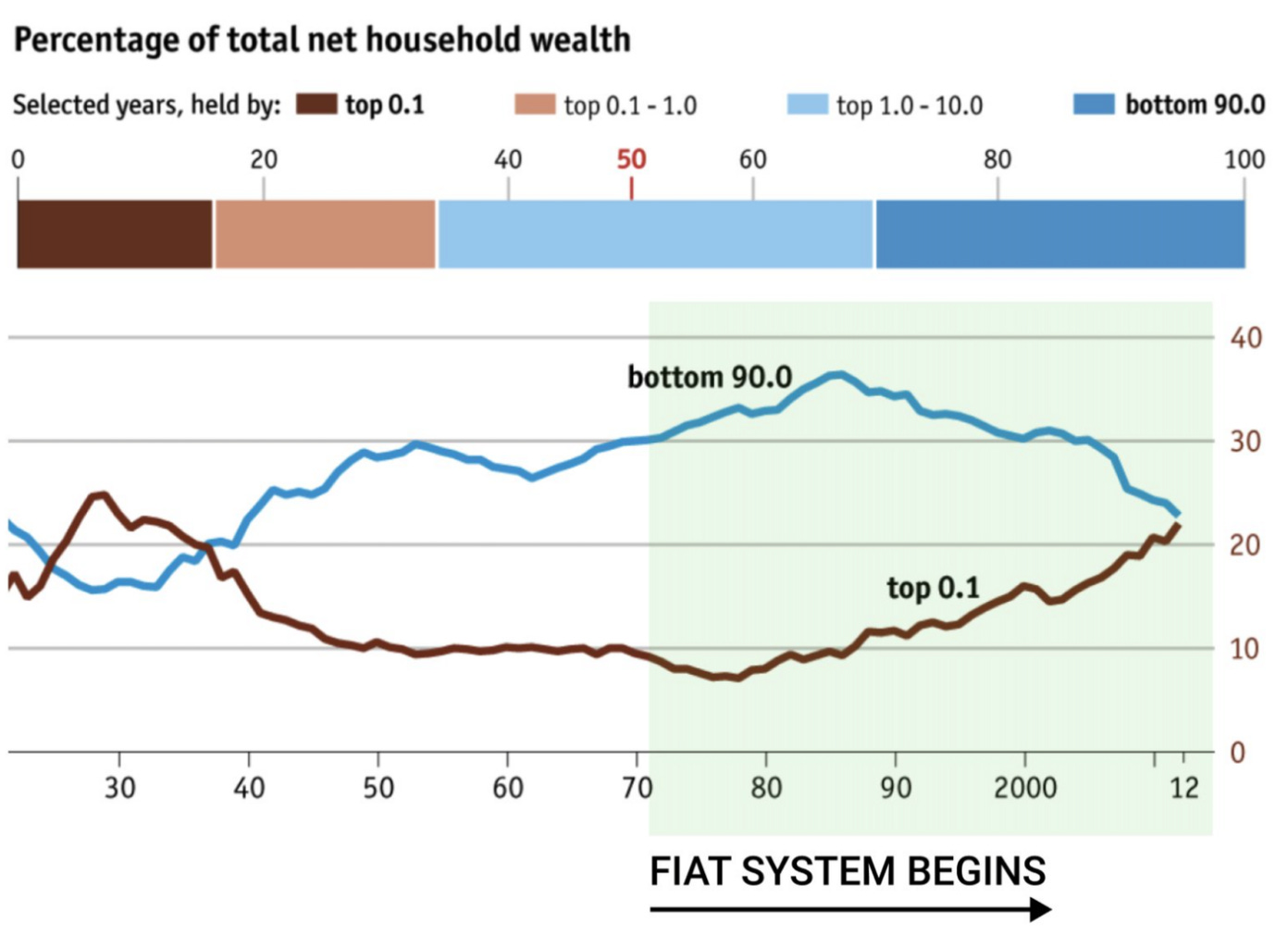

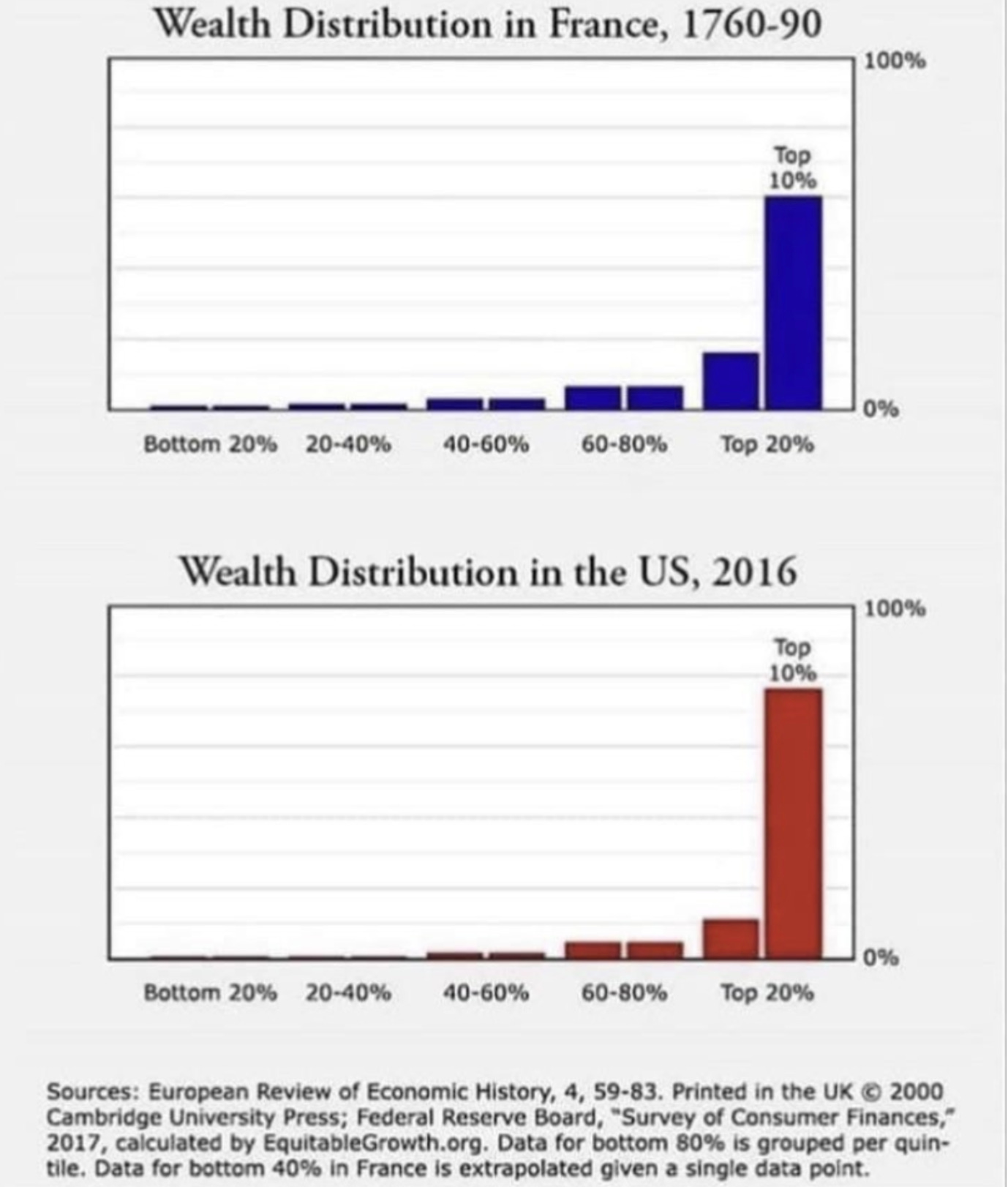

Third, the three largest low-cost asset managers, each of which has grown in size and influence to service the ever-growing demand for investment products in a world where everyone is forced to be an investor, now hold $22 trillion of assets under management. This has severely centralized ownership of America’s corporations in the sense that these three firms (Vanguard, BlackRock and State Street) hold more than half of the combined value of all shares for companies in the S&P 500. This means a handful of people at Vanguard, BlackRock and State Street cast a profoundly outsized number of shareholder votes. In 2019, an analysis conducted in a Boston University Law Review article estimated that these three firms could control as much as 40 percent of shareholder votes in the S&P 500 in a mere 20 years.

This concentration of ownership is deeply anticompetitive. Jack Bogle himself acknowledged this toward the end of his life.

Fourth, the reality that everyone must be an investor has contributed to the proliferation of financial products and the financialization of everything that has so profoundly reshaped our domestic economy. The finance, insurance, and real estate industries now account for a higher percentage of GDP than all other industries.

Fifth, this economic environment perpetuates wealth inequality and the impact of the Cantillon Effect, which I’ve written about extensively, most recently here and here.

One of Bitcoin’s most seemingly banal, yet utterly transformative use-cases is as a way to restore the power of saving money and, in doing so, fundamentally change our collective economic reality. If money is unmanipulable, it incentivizes saving and obviates the need for every single person to be a full-time investor.

This has a multitude of positive downstream effects. It leads to less malinvestment, less concentration of corporate ownership, more competition, more efficient markets, a radical diminution of the Cantillon Effect, and a disempowering of rent-seeking industries like finance. It means working people are not compelled by dire necessity to put their hard-earned money at risk because their purchasing power won’t be continuously diluted through inflationary monetary policies.

So yes, putting your money in a savings account will not make you wealthy in our current economic system. But instead of accepting this somewhat dystopian fate, we should question the value and the utility of a system in which saving money actually reduces wealth. And then we should change it.

Content Round-Up

1. “Bitcoin Stands Apart from Other Crypto, and What That Means for U.S. Public Policy,” an article by Andrew Bailey, Bradley Rettler, and Craig Warmke, each of whom is a college professor and a fellow at both the Bitcoin Policy Institute and the Resistance Money research collective. In this piece, the authors explain the crucial ways in which Bitcoin is distinct and distinguishable from the rest of “crypto.”

If you’re someone who is relatively new to Bitcoin and wants to know what makes it different from Ethereum, Solana, Dogecoin, etc. this is a good, succinct explainer.

2. “Why Bitcoin Speaks to Me as an Indigenous-Descent Woman,” an article by Ayelen Osorio. This is an older piece, but I’m working my way through Osorio’s Substack and wanted to share this one. It’s a moving article about Osorio’s grandmother, the plight of indigenous people all over the world, and how Bitcoin can serve as a powerful step in the direction of uplift and equity.

Here’s an excerpt I love:

“When I think about my grandma’s generation, I notice that it’s about the colonialist powers consolidating that power. When I think about my generation, it’s about disintegrating that centralized power.

Bitcoin is doing that, but with wealth. It’s taking concentrated wealth and dispersing it back to the people. Because bitcoin is a savings account that cannot be touched, taken away, diluted or manipulated, a person has agency of their financial life.”

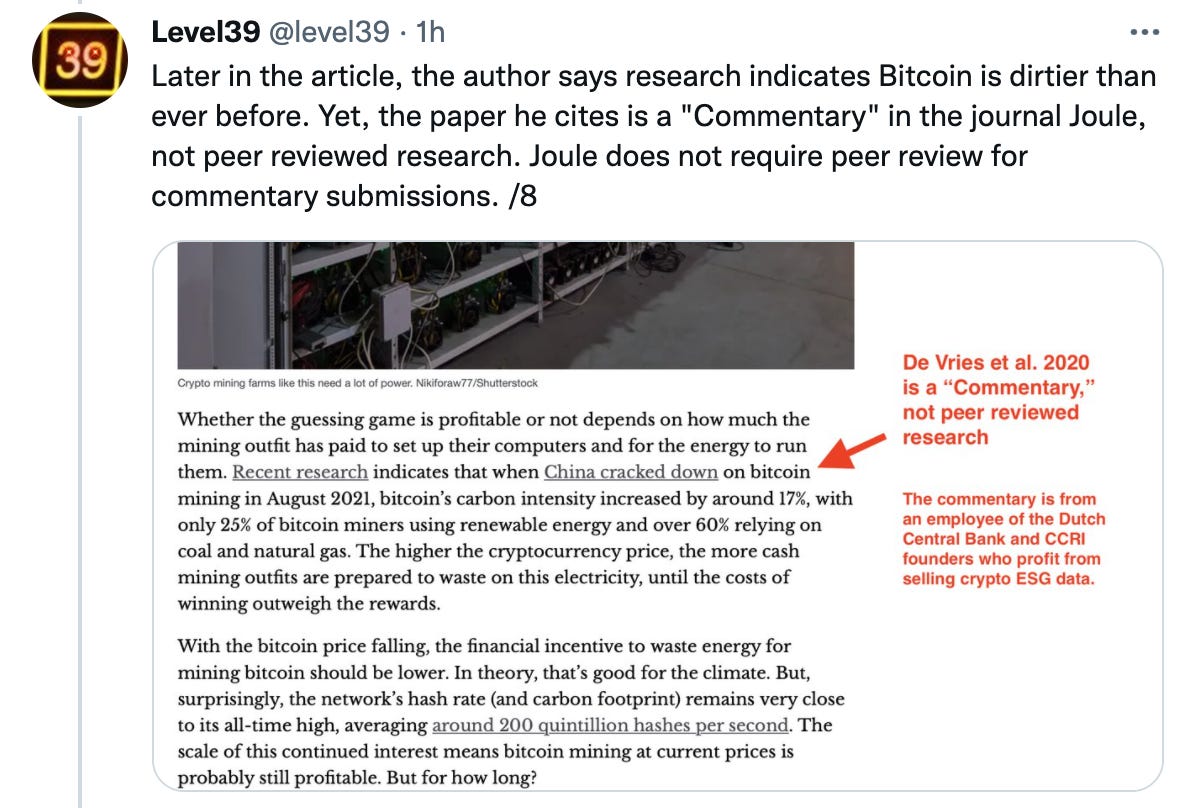

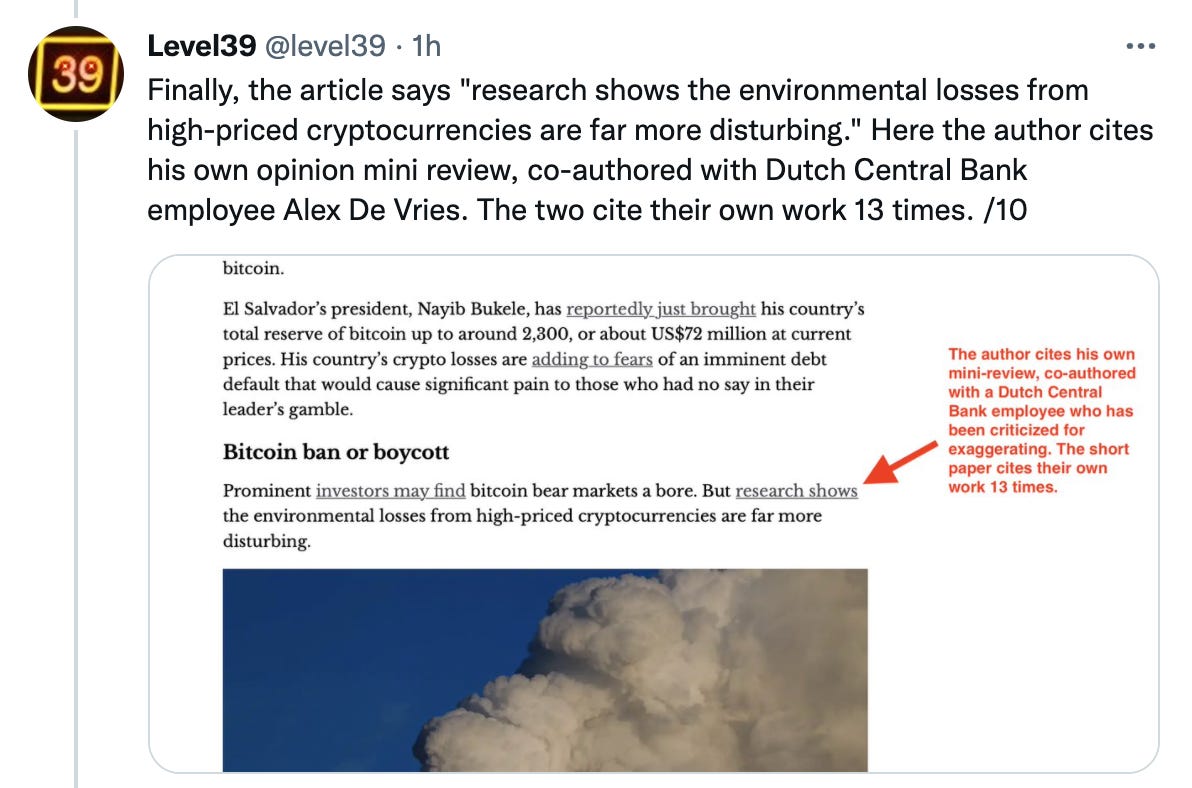

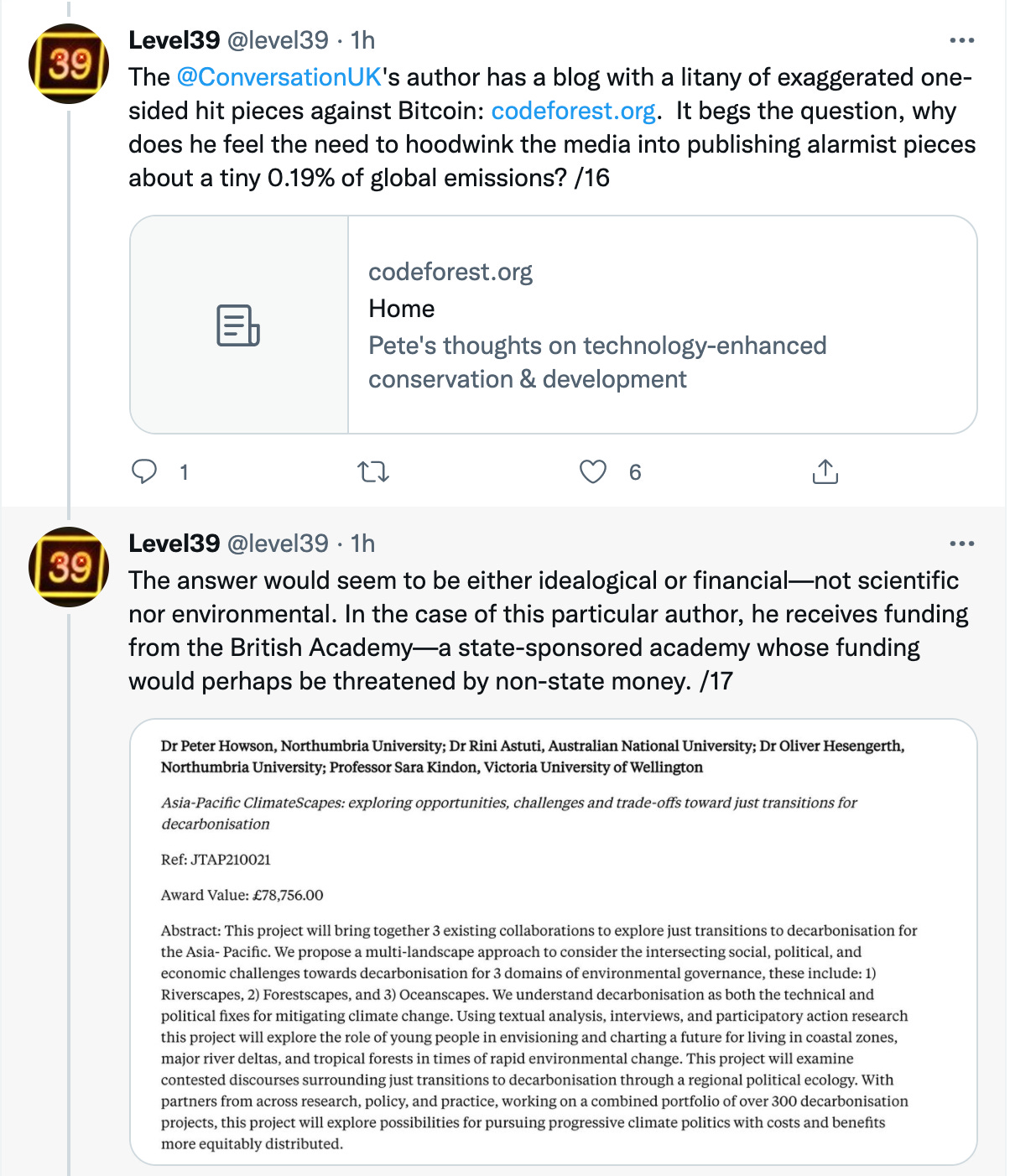

3. A Twitter thread from @level39 debunking some recent environmental misinformation:

Level39 has been doing incredible work investigating the specious rigor and illusory factual grounding of many of these environmentally-angled hit pieces on Bitcoin. This particular thread demonstrates the unflagging ubiquity of Alex de Vries’ work in the world of Bitcoin criticism, despite the fact that his work has been repeatedly debunked.

4. “Bitcoin: Inflating the Prospects of Deflation,” an article by Seb Bunney. Bunney is one of my personal favorite Bitcoin writers on the topic of macroeconomics. This piece is a useful primer on the effects of inflation vs. deflation, which can be confusing for some folks. To the extent that we are taught anything at all about deflation, it’s usually in the context of the Great Depression, which casts an indelible pall over the d-word. Bunney, like Jeff Booth, explains some of the benefits of deflation that aren’t as frequently discussed.

Consider the following excerpt:

“Under a deflationary world, we are allowing technological advancement to drive up the currency’s purchasing power. However, we can only reap the rewards if we fix our money supply. We need to prevent the destruction of purchasing power through monetary expansion. If we can fix our money supply, this will allow the currency to capture any technological gains resulting in the cost of goods, services, and assets to slowly decline as the currency’s purchasing power increases.”

Bunney also argues for the removal of the monetary system “from the clutches of the government,” something I’ve also argued for myself here.

Check out more of his writing on the Looking Glass Education platform, where you can also take a free course on how the monetary system works.

FAQ

What does decentralization actually mean and is Bitcoin still “decentralized” if its price goes down when the stock market and/or other cryptocurrencies go down?

This is a question I’ve been getting a lot lately, particularly on Instagram. It’s certainly been a brutal couple of months for markets, with seemingly no safe havens (other than energy). The entire crypto space, along with the NASDAQ, has gotten thoroughly shellacked.

In light of all this, some folks have been asking me if Bitcoin’s present failure to decouple from the broader markets means that it’s not, in fact, decentralized. One of the guys from Earn Your Leisure posted a video on a particularly rough day for prices, proclaiming that there was no such thing as decentralization. His argument seemed to be that since everything was dropping, decentralization clearly didn’t exist.

The problem with this view, which I think is a common one, is that it doesn’t have anything to do with decentralization. It’s a conflation of two separate concepts: correlation and decentralization. So let’s distinguish these two things.

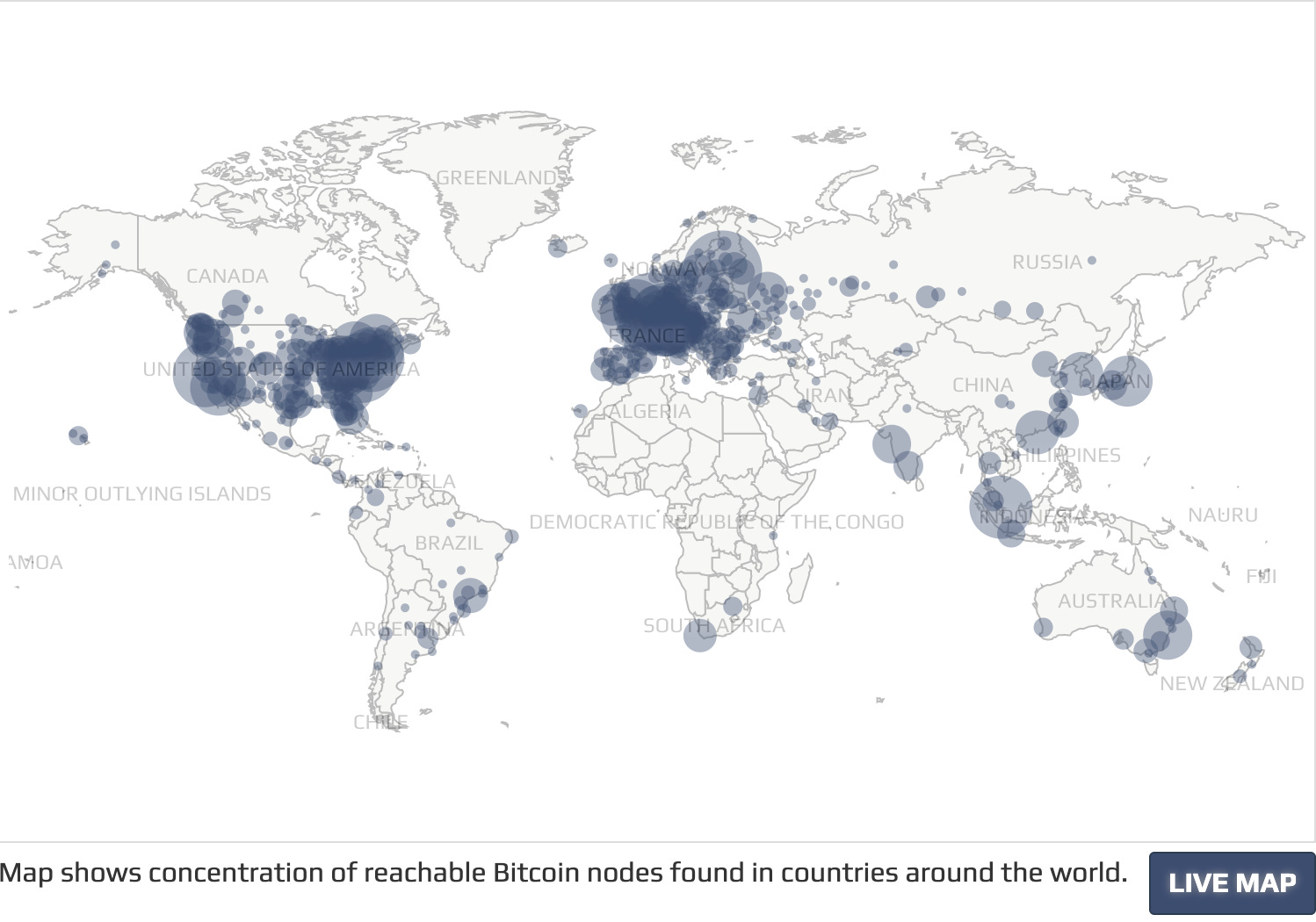

Decentralization fundamentally refers to how many nodes are running the Bitcoin software. That’s it. The more nodes that are running it, the more decentralized the network is. Nodes hold a full copy of the Bitcoin blockchain and their function is to verify transactions.

Correlation refers to how different asset classes move in relation to each other. Correlated assets go down at the same time, and they go up at the same time. Uncorrelated assets do not move in the same direction at the same time. The degree to which they move in different directions varies and depends on just how uncorrelated they are. But, suffice to say, they do not move in the same direction at the same time.

These two concepts (decentralization and correlation) are not really related. That Bitcoin’s price drops when the NASDAQ drops or when other crypto prices drop has nothing to do with how many nodes are running the Bitcoin software. This, in turn, means it doesn’t have anything to do with Bitcoin’s degree of decentralization. Conversely, if Bitcoin’s price were to rise while the NASDAQ or other crypto prices dropped, that also would say nothing about its level of decentralization.

Decentralization and correlation are two different concepts. Bitcoin remains the most decentralized crypto protocol, with about 16,000 active nodes worldwide.

(Chart from Bitnodes.io)

As always, thanks for reading! If you enjoyed it or found it useful, share this newsletter widely and freely!

“Civilization is in a race between education and catastrophe. Let us learn the truth and spread it as far and wide as our circumstances allow. For the truth is the greatest weapon we have.” -H.G. Wells

See you in two weeks,

Logan

SUPPORT

Send bitcoin to my Strike

SOCIAL

DISCLAIMER: I am not investment advisor and this is not investment advice. This is not, nor is it intended to be, a recommendation to buy or sell any security or digital asset. Nothing in this newsletter should be interpreted as a solicitation, a recommendation, or advice to buy or sell any security or digital asset. Nothing in this newsletter should be considered legal advice of any kind. This newsletter exists for educational and informational purposes only. Do your own research before making any investment decisions.

© Copyright Logan Bolinger

“I Finance the Current Thing” by Allen Farrington.