Think Bitcoin™ Issue #6

Coinbase vs. the SEC; El Salvador; Bitcoin's monetary policy; We're still early

Hey friends, welcome back to Think Bitcoin™. This past week was a big one in terms of Bitcoin news and developments. Since I think the issues raised by some of the headlines are exceedingly important to discuss and think about, I’ve devoted significant space to them. In an attempt to still keep things condensed, I thought it appropriate to skip the “For the new and new-ish section” this week. We’ll pick back up with it next week!

In this issue:

Content Round-up: 5 articles, 2 podcasts

Headlines/News: Coinbase rips the SEC; status update on El Salvador; Tuesday’s flash crash; SEC sues Rivetz

Bonus: The mathematical formula that is Bitcoin’s monetary policy

As always, if you find this newsletter interesting or useful, please share it with others who might find it interesting or useful!

Content Round-Up

1. “Bitcoin Fixes This,” a Wolf of All Streets podcast episode with Alex Gladstein. As you know, I’m always trying to foreground Bitcoin’s use and adoption as it relates to the advancement of human rights and economic empowerment. Alex Gladstein is a human rights activist, reporter, and Chief Strategy Officer at the Human Rights Foundation. He speaks at length here on how Bitcoin can be a tool for human rights, why central bank digital currencies will be tools of government control and surveillance, and why Bitcoin is superior to other crypto tokens.

If you’re someone interested in Bitcoin’s promise with respect to human rights and financial access, and how it’s currently being used in various countries to those ends, this is a great podcast. I’d highly recommend following Gladstein’s work and following him on Twitter.

For more on Gladstein, his work, and his background, check out the interview he did for Natalie Brunell’s excellent podcast, “Coin Stories.”

2. “Bitcoin and Addiction: A Life in (Fiat) Recovery,” an article by OtterBTC. This is a moving piece by a recovering alcoholic comparing the body’s addiction to substances to society’s addiction to debt. Society, after all, is like a body, and, as we know, breaking an addiction can have severe effects on the body. Obviously, the severe and painful effects of withdrawal ultimately subside and allow for restoration of health and growth. Contrarily, an accelerating addiction eventually kills the body.

OtterBTC also writes about discovering Bitcoin in recovery, how Bitcoin has lowered his/her time preference (i.e. made him/her a long-term thinker), fostered an interest in self-sovereignty, and improved other areas of his/her life.

I like this quote:

“If we are to recover from the ills of wasteful consumerism, re-election seeking, bought-and-paid for government officials, and the unsustainable dependencies we as a society have on the cheapest goods and labor, we must adopt better money by which to use as the conduit for change. Bitcoin fixes this.”

3. “3 Reasons Why It’s Not Too Late to Buy Bitcoin,” an article by Nik Bhatia. Bhatia is the author of the excellent book, Layered Money, which I highly recommend. He has also been a guest on Robert Breedlove’s What is Money Show podcast, which I also highly recommend.

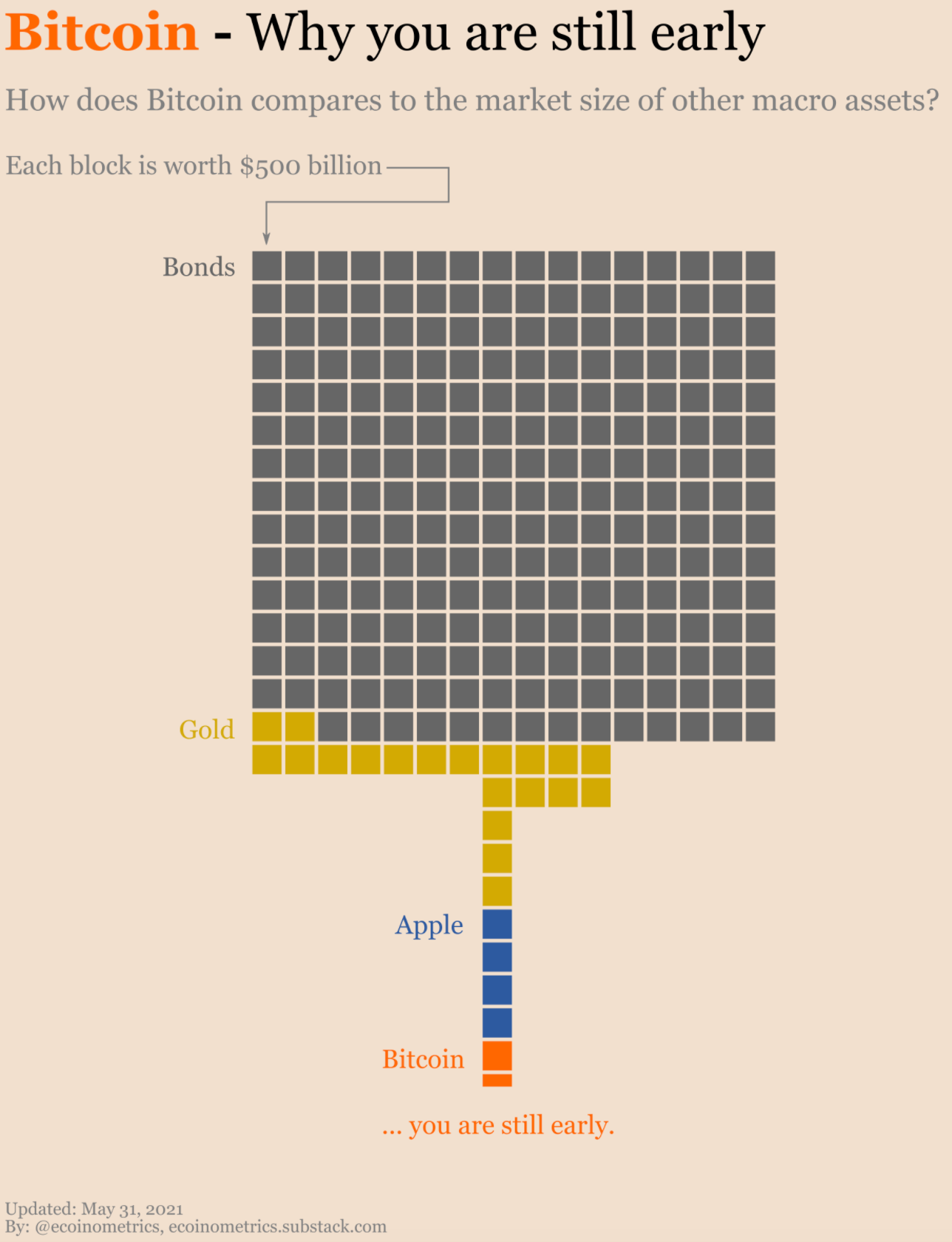

This is a pretty short piece, but it very thoughtfully addresses the commonly-held belief of many new Bitcoiners that they are late to the game. I get comments and messages all the time from folks who think the current price point of Bitcoin means they’ve missed the boat, which impels them to look to other, inferior coins, a number of which are outright scams, just because these coins are cheaper. It’s important to remember that while many other coins are akin to casino bets, Bitcoin is the ultimate long-term asset. Bhatia explains why we are actually early.

Here’s a great visual to accompany this piece from the good folks at Ecoinometrics:

4. “Ukraine is the Latest Country to Legalize Bitcoin as the Cryptocurrency Slowly Goes Global,” an article by MacKenzie Sigalos. Read alongside “Inside Ukraine’s Bitcoin Bill,” an article by Nik Hoffman. Both pieces discuss the Bitcoin law passed in Ukraine last week. MacKenzie Sigalos, as I’ve said before, is one of the very few mainstream financial journalists who engages with the Bitcoin community in good faith, does her research, and provides thoughtful commentary.

5. “El Salvador’s Bitcoin Adoption to Cut Western Union Revenue, Increase Population Wealth,” an article by Namcios. In this piece, Namcios explains how remittance payments can now be made directly, person-to-person, using Bitcoin, obviating the need for exploitative middlemen like Western Union. Cross-border remittance inflows constitute approximately 25% of El Salvador’s GDP. Middlemen like Western Union take large cuts of these inflows. Additionally, remittance recipients have to retrieve these inflows at central, physical locations. This process can often be dangerous as folks have to travel to get to these locations, which naturally tend to be places around which gangs congregate, well aware of why folks are there. Bitcoin fixes this.

Headlines/News

As I mentioned at the outset, there has been an absolute ton of news this past week.

Flash crash on Tuesday

On Tuesday of last week, the day El Salvador officially adopted Bitcoin as legal tender, Bitcoin dropped approximately 10% pretty quickly, before recovering moderately. Most other crypto tokens dropped precipitously, as well. While many crytpo skeptics speculated that this was the market deciding El Salvador had made a mistake, on-chain metrics seem to reveal that, as per usual, this drop was the result of folks getting a little over-leveraged long (meaning they’re betting on the price increasing). This is often the case with sharp drops. Crypto investors are able to use significant leverage on various platforms, which can result in significant and swift liquidations when the price moves downward, causing a quick and cascading spiral of forced selling.

Here, it seems there was some profit-taking in a “buy the rumor, sell the news” situation, meaning some folks took profits at the end of the run-up to El Salvador’s adoption by selling, knowing the price would likely be high in anticipation of that adoption, which caused those who levered up to bet that the El Salvador adoption would lead to a sustained price spike to get liquidated.

This isn’t the only view on what caused the flash crash, but it’s the most common one I’m seeing from the analysts and on-chain experts I follow.

These liquidations can act as a sort of “cleansing” of the debt and leverage out of the market which, ultimately, is a healthy dynamic. We could and should compare to the fiat currency world in which debt and leverage are never allowed to reset or clear and instead just expand indefinitely, building more and more fragility into the system. Crypto, unlike the fiat capital markets, is a free market, though. So if you get caught over-leveraged long, you’ll likely get liquidated, and no one will come to bail you (or the market) out.

For folks interested in on-chain metrics, I’d recommend following Will Clemente and Willy Woo.

El Salvador officially adopts Bitcoin as legal tender and promptly buys the dip

I’m continuing to follow the rollout of Bitcoin as legal tender in El Salvador. There were some technical difficulties with the state-backed Chivo wallet on Tuesday, as well as with servers in El Salvador, which appeared to get overwhelmed. This caused some temporary issues for people, but my understanding is many of these issues have since been resolved.

I saw a lot of folks on Twitter (and received some direct messages from some) who were critical of some of these technical difficulties, suggesting the imperfect rollout was indicative of incompetence and simply more evidence that this whole experiment would fail. I would invite those folks to recall the inauspicious large-scale rollouts of a number of major government programs in putatively competent western powers. In the U.S., consider the very bumpy rollout of Obamacare (through the healthcare.gov site), or even the distribution of stimulus checks, just to name a few. The point is, some of the most sophisticated western governments struggle just as much, if not more, when attempting to integrate the entire populace to something on a large scale. So, all things considered and in this broader context, the rollout in El Salvador went fairly well. Was it perfect? Of course not. But expecting perfection with something of this magnitude is, in my opinion, absurd.

In a remarkable move, during Tuesday’s flash crash, El Salvador’s President Bukele actually bought the dip on behalf of El Salvador, as a nation, and tweeted about it to the International Monetary Fund (the IMF). The IMF has given El Salvador the cold shoulder since the latter announced it would adopt Bitcoin as legal tender.

The fact that a nation state bought the dip, openly and defiantly, is truly remarkable.

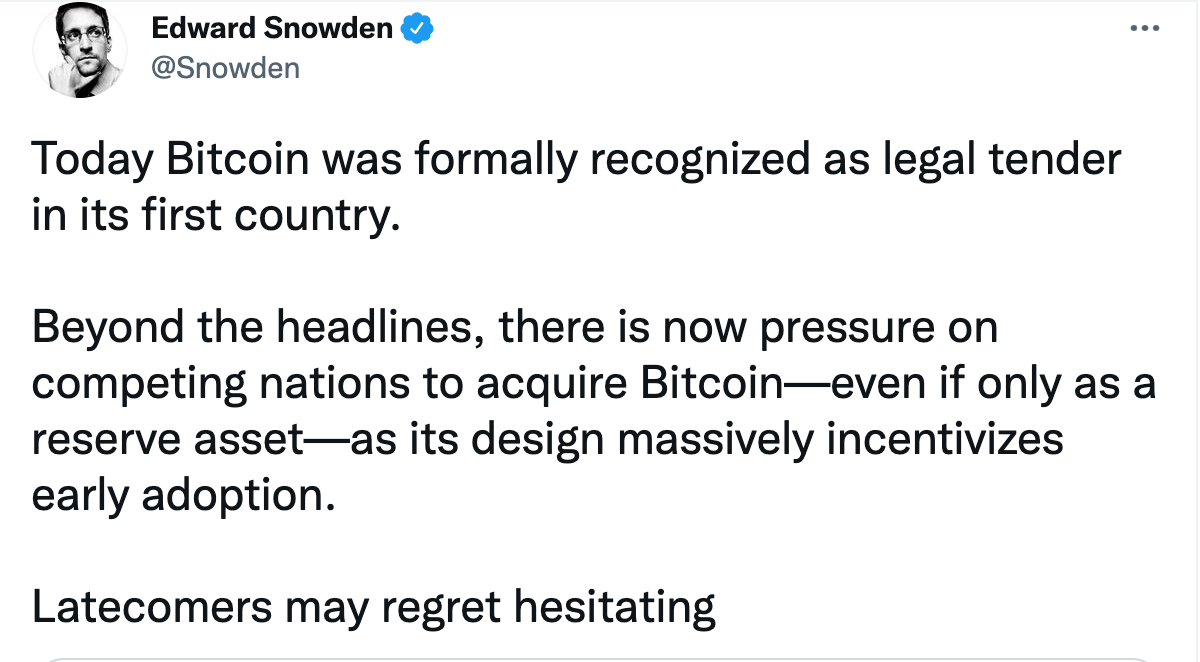

For me, the most important takeaway is the game theory this potentially sets up for other nations, which Edward Snowden encapsulated perfectly:

Key point: “…as its design massively incentivizes early adoption.” Other nations are watching El Salvador closely, and many large western nations who have enjoyed massive economic privilege (“exorbitant” privilege, as de Gaulle once said of the U.S.) and the geopolitical power that comes with that privilege, are clearly hoping El Salvador’s gambit fails. But the game theory is now set up. With one country already adopting it and putting it on the national balance sheet, every other country now has to make a decision. If El Salvador’s experience works, more countries will surely go the same route. There are countries already moving in that direction, as we speak. In this scenario, being the last country to acquire bitcoin means acquiring less and at dramatically higher prices. The advantage goes to the early movers.

Coinbase and the SEC lock horns

On Wednesday, Coinbase disclosed that it had received a Wells notice from the SEC. A Wells notice is a formal letter from the SEC stating the agency’s intent to bring an enforcement action against the recipient. The notice sent to Coinbase relates to their forthcoming “Lend” product, which would allow users to lend select crypto assets for yield. The product was set to launch with USDC, a stablecoin redeemable on a 1:1 basis with U.S. dollars and backed by dollar-denominated assets. The SEC has conveyed to Coinbase that if they launch this product the SEC will bring an enforcement action against them.

Coinbase reported that they’ve been “proactively engaging with the SEC about Lend for nearly six months.” They have answered all of the SEC’s questions both in writing and in person. According to Paul Grewal, Coinbase’s Chief Legal Officer, the SEC didn’t offer much of a response, besides just asserting that the Lend product is a security. The SEC eventually opened a formal investigation and asked for more documents and responses. They also asked for someone from Coinbase to give sworn testimony about Lend. Again, Coinbase complied. At no point has the SEC offered an explanation as to why they think Lend is a security. They appear to believe the reasons are self-evident and clear in the law. Some would argue that the law is, in fact, clear. Others, as we’ll see, argue that it’s not clear at all.

The SEC has also made requests of Coinbase that are wholly unrelated to the issue of whether Lend is a security or not. When Coinbase initially announced Lend they began a waitlist for the product. In a somewhat Orwellian move, the SEC asked Coinbase for the names and contact information of every person on the Lend waitlist, despite this having nothing to do with whether Lend is a security. Coinbase did not comply with this request.

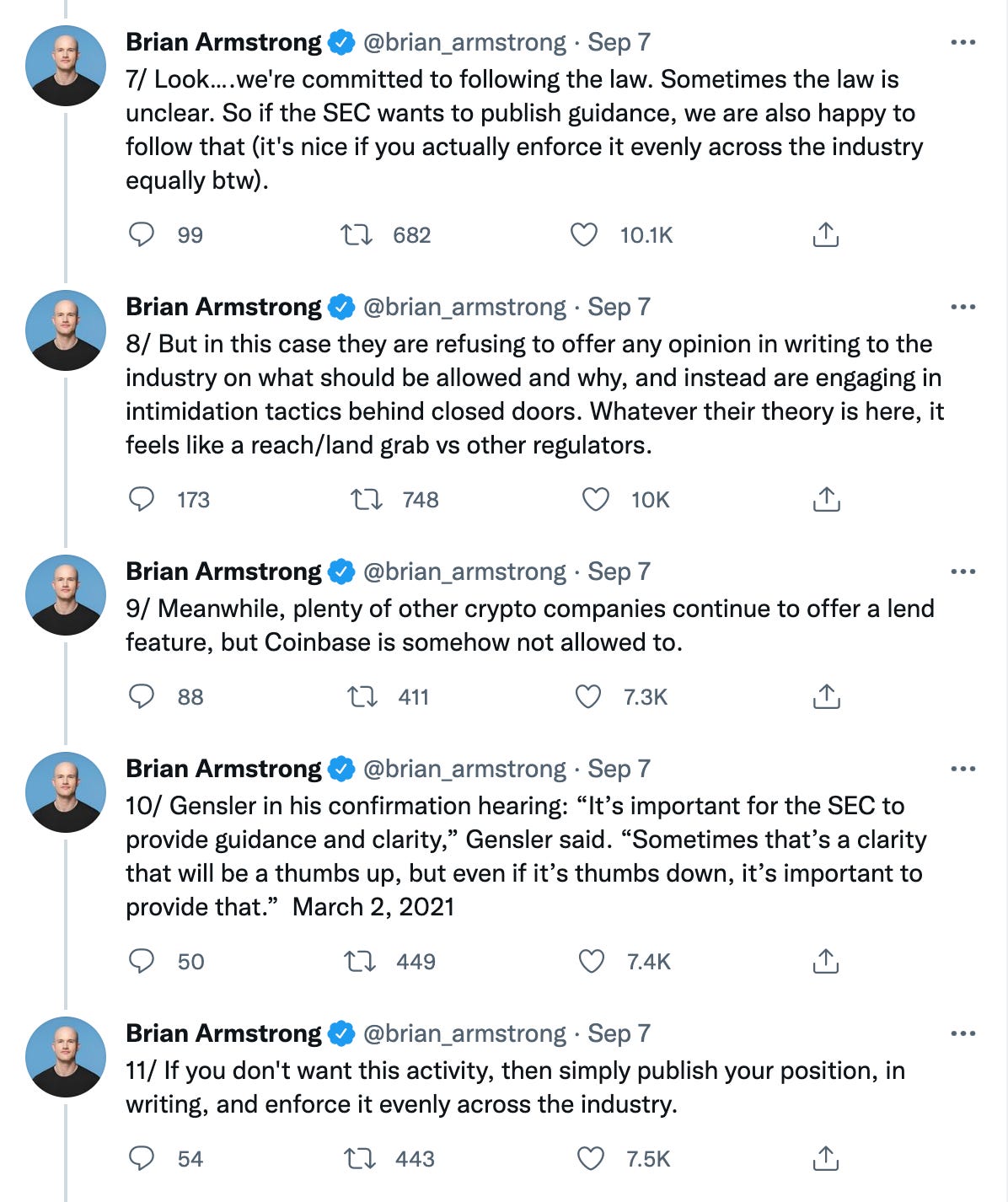

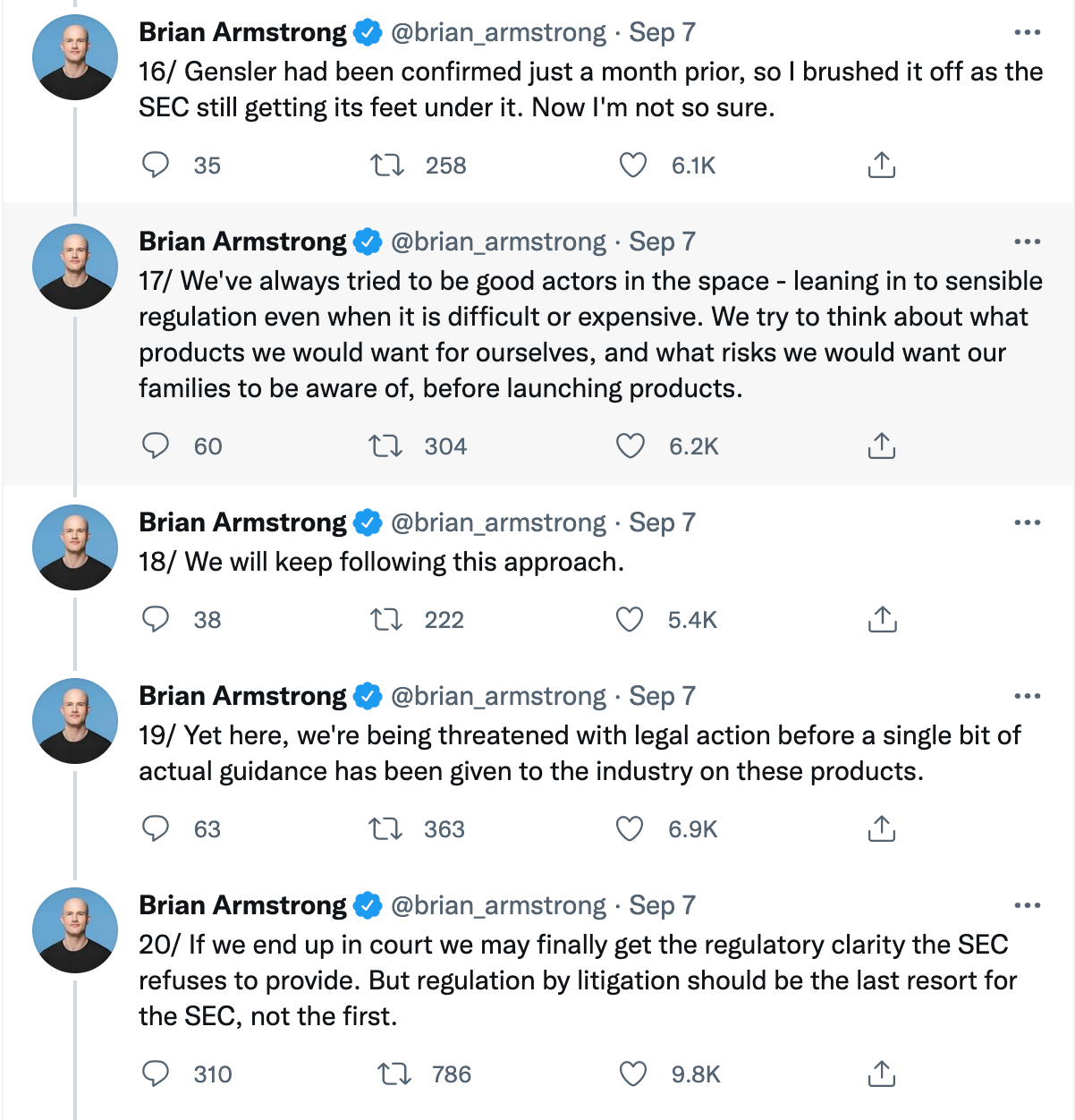

Brian Armstrong, Coinbase’s CEO summed things up in a Twitter thread:

There’s so much to unpack here. First, I think the company’s decision to share its experience publicly and, in doing so, openly describe the SEC’s “sketchy” behavior, is remarkable in its own right. Coinbase, unlike many in the space, has always sought to be compliant, to be a good actor, and to engage with regulators and lawmakers in good faith. They have tried to play by the rules, presumably assuming this would endear the company (and also the crypto community, as a whole) to regulators and foster a collaborative relationship that could result in win-wins for users and the government, alike. Unlike many other tech companies (like, to name just one example, Uber), Coinbase has heretofore decided to refrain from taking the ask-for-forgiveness-not-permission approach to regulation.

This confrontation with the SEC, however, seems like it may mark a turning point in Coinbase’s approach. The SEC, much like the U.S. Treasury Department, does not seem to be very interested in engaging with the crypto industry in any meaningful way. This brings me to my second observation, which relates to Armstrong’s “if we end up in court we may finally get the regulatory clarity the SEC refuses to provide” comment. This very much appears to be Coinbase openly pondering whether it might be worth it to go to court and have a judge interpret the law, as opposed to allowing the SEC to use the threat of litigation as a way to regulate without having to explain themselves. Coinbase certainly has enough money to go this route, if they choose. But going to war with the SEC here has its own risks.

The issue of whether the Lend product is actually a security is a hotly debated topic. We’ve discussed the Howey Test in a previous issue, which is the 1946 Supreme Court case defining what constitutes an “investment contract” under the Securities Act. This was important because an investment contract is a security, per the Securities Act and, subject to certain exemptions, securities have to be registered with the SEC.

Coinbase’s Lend product is clearly not a stock or a note. Grewal argues that it’s not an “investment contract,” either, and expressed his frustration that the SEC has not explained why, exactly, it believes Lend is a security. As Preston Byrne, a partner at Anderson Kill, has written with respect to BlockFi, products like Lend may seem merely like what you do with your deposits at your bank, but case law has carved out an exception for bank deposits and CDs, vehicles that are federally insured against default and not commonly known or treated like securities. It’s worth noting, however, that there are also cases in which CDs have been deemed securities (see, e.g., the Gary Plastics case).

Crypto law Twitter, including Byrne, chimed in with some thoughts on Lend, specifically. I don’t want to get too granular on this point because (a) I’m no longer a securities lawyer and (b) it can, as evidenced by the preceding paragraph, get a bit heady, but the ramifications are far-reaching and worth discussing. The 90-year-old securities laws and the 80-year-old cases we primarily rely on to define securities are, clear as they may be in many cases, in my opinion, not equipped to effectively and holistically address the crypto space. As currently written and as potentially applied to crypto, these laws and cases threaten to over-protect investors, which isn’t really protection at all, and stymie the growth of a societally significant new industry.

With respect to the debate over whether Lend is a security, Byrne tweeted the following:

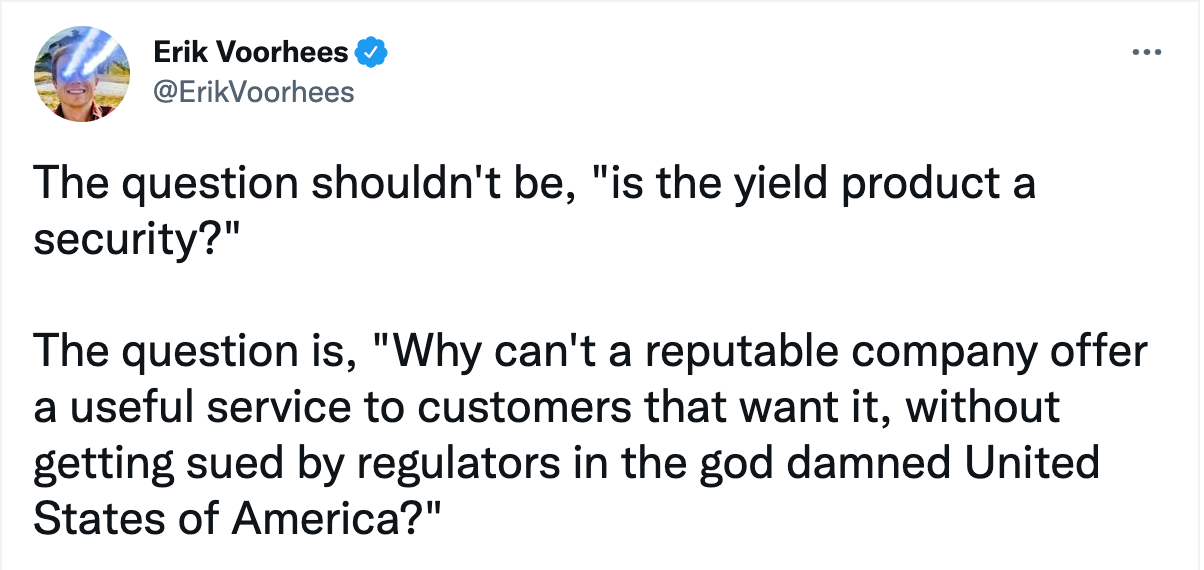

Erik Voorhees, founder of ShapeShift, summed up the non-legal perspective of many in the crypto community:

Though many of us may feel this way, we do need to grapple with and navigate the current securities law regime, and Coinbase’s situation is challenging the adequacy of that regime and its appropriateness for the space, while also revealing its many shortcomings.

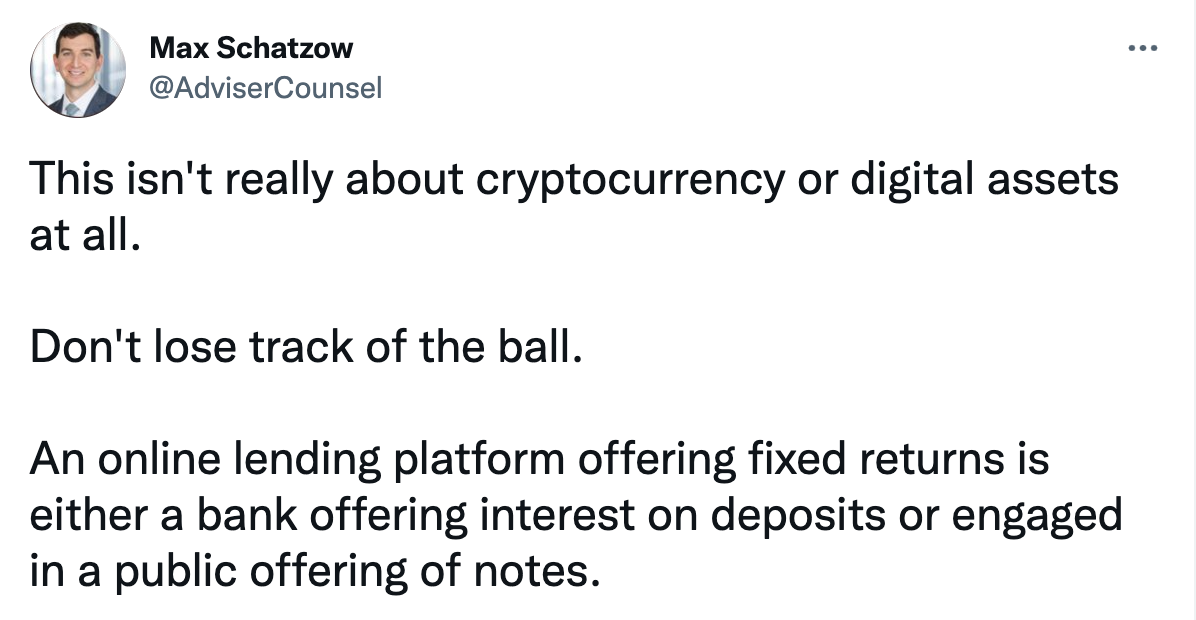

On this issue of whether Coinbase is performing a bank’s function and whether Lend actually renders Coinbase a bank, Max Schatzow added:

Obviously, one of the prevailing and ever-growing elephants in the crypto room right now is the issue of which cryptocurrencies and derivative products, if any, are securities. Further, and stemming from this question, is our definition of securities still adequate? If certain cryptocurrencies or derivative products are securities, and they’re unregistered, what does this mean for the industry?

It’s worth pointing out that Bitcoin is decidedly not a security under the Howey Test. But projects like Ethereum, which had a pre-mine distribution, is relatively centralized, has investors, etc… how is the SEC likely to view this? Particularly in light of what Gensler said last week (which we noted in last week’s issue) about the idea of some crypto tokens being “utility tokens,” namely that he thought this argument was hogwash.

I’m certainly not here to proclaim that Ethereum or any other crypto token is or is not a security, definitively. I think there are crypto tokens that obviously fit the definition of a security under Howey. I also think Bitcoin very obviously does not. But there’s clearly a fair amount of gray area, both in tokens themselves and in derivative products. If the SEC approaches the space with the now-rather-blunt instrument of Howey, the consequences for the industry, its place in America, and the economic growth it can foster could be severe.

Congress can certainly step in and just pass a new law that establishes a better definition of “security” or perhaps establishes more nuanced, thoughtful exemptions from registration with the SEC.

Former CFTC Chariman Chris Giancarlo has also chimed in. On CoinDesk TV he said, “It’s important for this new innovation that we don’t apply 90-year-old statutes, which is effectively what we have.” He additionally noted that “Ultimately, it will be the courts that will have to determine jurisdiction and apply the security laws to these asset classes, and I’m optimistic that Congress steps in.”

Pivoting back to the SEC’s Wells notice to Coinbase, if the SEC is really as open to talking with the crypto industry as they purport to be (Gensler has famously invited crypto operators to “come in” and talk to the SEC), why are they sending out Wells notices, asking for names of potential customers, and refusing to elucidate their position?

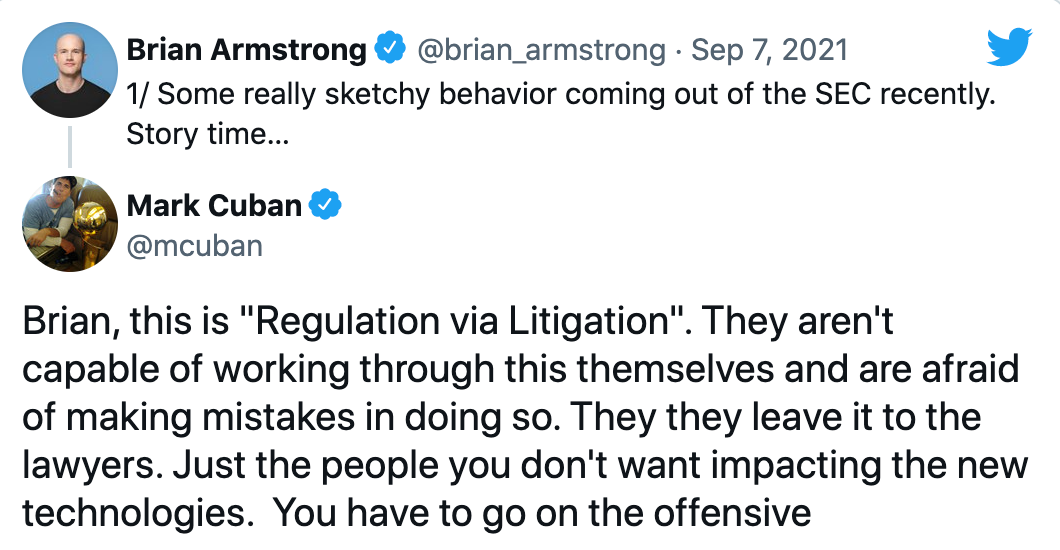

Mark Cuban, no stranger to tangling with the SEC, encouraged Brian Armstrong to go “on the offensive:”

Needless to say, the impending collision of Coinbase and the SEC, as a microcosm of the growing tension between traditional finance and the crypto economy, is likely to have far-reaching consequences, and it will be fascinating to follow.

Strategically, Coinbase does have the war chest, the personnel, and the clout to take on the SEC. Arguably, if Coinbase does not do so, the SEC could bring a similar enforcement action against a smaller player, obtain a settlement, and then use that as legal precedent for future enforcement actions. Jerry Brito of Coin Center made this point:

SEC reportedly investigating other DeFi projects beyond just Uniswap

Last week news broke that the SEC was investigating Uniswap Labs, the developer behind the Uniswap protocol, the largest decentralized exchange on Ethereum. A decentralized exchange is a platform on and through which users can conduct a host of financial transactions without the governance or direction of centralized intermediaries like banks or investment firms.

This week it’s being reported that the SEC is looking at other as-yet-unnamed DeFi platforms. More signs that Gensler and the SEC are looking to at least attempt to bring DeFi within some kind of regulatory parameter and clip the wings of the crypto space as a whole.

SEC sues Rivetz

The SEC obviously had a busy week. They charged Rivetz Corp., a now-defunct blockchain hardware firm, for selling unregistered securities in the form of their “RvT” token via an initial coin offering (an “ICO”) in 2017.

I think this is notable for the language and angle of the SEC complaint. In their complaint, the SEC states that the “offer and sale of RvT tokens was not registered with the SEC, and investors did not receive the disclosures required by the federal securities laws.” Remember, many now-popular crypto tokens were sold in ICOs in 2017 (e.g., Polkadot, Filecoin, Tezos, etc.). Gensler has stated before that he will not conduct a token-by-token analysis of crypto tokens, which suggests he’s looking to apply a broad, uniform framework (like a strict interpretation of the Howey test) to the space as a whole. Whether this action against Rivetz is a one-off against a shady firm who did shady things or an indication of Gensler’s position on ICOs and a harbinger of things to come, remains to be seen, but it is abundantly clear that he is fixated on what he views as unregistered securities.

It is, again, worth regularly repeating that Bitcoin never had an ICO, never distributed any coins to “investors,” and never had any investors. Gensler is obviously hyper-focused on crypto, but he has acknowledged Bitcoin’s near-immaculate inception (organic, decentralized, no investors, etc.) and seems to be of the camp that though many crypto tokens seem to meet the definition of a security under Howey (at least in his opinion), Bitcoin does not.

Quintenz joins a16z

A couple weeks ago, Brian Quintenz, then a commissioner of the CFTC, announced he was stepping down. I speculated that it was only a matter of time before he joined a crypto company in some capacity, as he’s been an outspoken advocate for the industry. Sure enough, this week he announced he was joining Andreesen Horowitz, a venture capital firm with a massive footprint in the crypto space.

From a16z’s announcement of the hire:

“As part of our larger effort to make sure we have a world-class support system in place when it comes to policy and regulatory matters, I’m thrilled to announce that Brian Quintenz, a former Commissioner of the Commodity Futures Trading Commission, is joining as an advisory partner on the crypto team. The CFTC plays a critical role as a federal regulator with jurisdiction over digital currencies, utility tokens, and other non-security commodities, and Brian has long stood out as an innovative thinker in the crypto and DeFi space. He understands both how crypto technology works and how the CFTC thinks about the issue. His ability to translate between the two will be central to the success of a16z Crypto’s policy program and our portfolio companies.”

Bonus/Miscellaneous

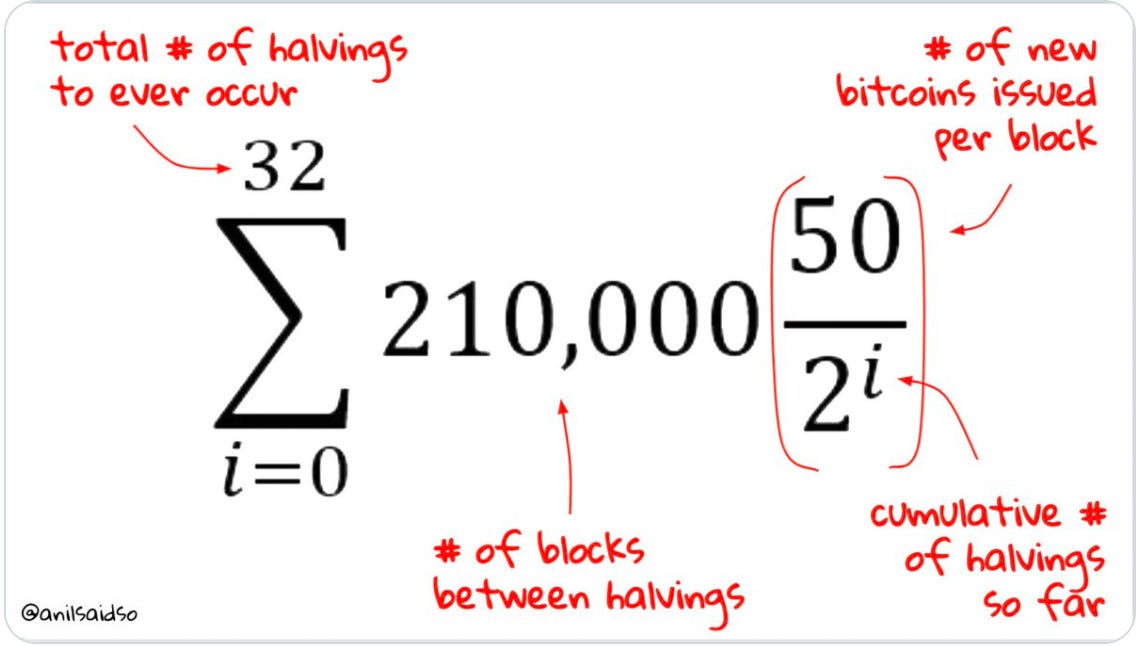

Unlike fiat currency, Bitcoin’s monetary policy does not rely on the judgments of a handful of unelected humans in a room who can and do choose to manipulate, inflate, and debase the money. Bitcoin’s monetary policy is governed by math. The formula is elegant, simple, and un-manipulable. It looks like this:

As always, thanks for reading! If you enjoyed it or found it useful, share this newsletter widely and freely!

“Civilization is in a race between education and catastrophe. Let us learn the truth and spread it as far and wide as our circumstances allow. For the truth is the greatest weapon we have.” -H.G. Wells

See you next week,

Logan

SOCIAL

DISCLAIMER: I am not investment advisor and this is not investment advice. This is not, nor is it intended to be, a recommendation to buy or sell any security or digital asset. This newsletter exists for educational and informational purposes. Do your own research before making any investment decisions.

© Copyright The Why of FI.