Think Bitcoin™ Issue #4

Bitcoin is anti-war; competing with fiat; validating transactions; everything gets cheaper

Hey friends, welcome back to Think Bitcoin™. As always, if you’re brand new or relatively new to Bitcoin and looking for some education on the basics, feel free to scroll down to the “For the new and new-ish” section and work your way up.

In this issue:

Content Round-up: 4 articles, 1 podcast

Headlines/News: Updates on the infrastructure bill / Rep. Soto introduces multiple bills / Majority of surveyed executives think crypto will compete with fiat very soon / Jack Dorsey and Square want to build a decentralized Bitcoin exchange

For the new and new-ish: How transactions get validated, minting new coins, Bitcoin’s supply cap

As always, if you find this newsletter interesting or useful, please share it with others who might find it interesting or useful!

Content Round-Up

1. “Finding Financial Freedom in Afghanistan,” an article by Alex Gladstein. This is another riveting piece from Gladstein, who is a human rights journalist and activist. As I’ve said repeatedly in previous issues, I consistently want to foreground Bitcoin’s promise for human rights, financial access, and financial inclusion. Additionally, I always want to highlight adoption and usage outside of western democracies, because too often our gaze is fixed solely on American or European investors and what they think of Bitcoin. It’s important to remember that Bitcoin’s promise is not confined to being merely an inflation-hedge asset in the well-diversified portfolios of western investment firms and individuals.

In this piece, Gladstein follows Roya Mahboob, Afghanistan’s first female tech CEO, who shares how Bitcoin is being used in Afghanistan and why it’s important. Mahboob first learned about Bitcoin in 2013 and began paying her employees with it. It was an upgrade to the hawala system and gave her employees, most of whom were women, the ability to hold their own money without the risk of it being taken by the men in their lives.

The article chronicles Mahboob and Bitcoin from 2013 through the current day in Afghanistan. Living through the fall of Kabul, with the consequent cratering of the currency, the freezing of bank accounts, the halting of remittances, and the suspension of aid, Mahboob wishes she could have educated more people about Bitcoin, which would have allowed more people to preserve their wealth and flee with it.

2. “Bitcoin is the War on War,” an article by Robert Breedlove. Breedlove is one of the most intellectually rigorous thinkers/philosophers in the Bitcoin space. His writing is always extremely thought-provoking.

In this piece, he argues that modern nation-states use war to determine who owns what. In other words, war is the “consensus mechanism for property distributions.” Fiat currency, printable and debaseable as it is, allows governments to fund wars indefinitely. Bitcoin is a multi-front attack on this paradigm. One significant motivation for state violence and coercion stems from the “violability” of property. In other words, the gold, the oil, etc. remains after violence is wrought upon other nation-states. As “inviolable” property, Bitcoin diminishes this motivation.

Additionally, Bitcoin would impose a financial discipline upon nation-states. Unlike fiat currency, you can’t simply print more bitcoin to finance protracted violence.

3. “OnlyFans Shows How the Banking System is Politicized,” an article by Nic Carter. Carter is a founding partner at Castle Island Ventures, a venture capital firm focused on public blockchains. He has written extensively and tirelessly about Bitcoin mining and the energy debate surrounding mining.

In this piece, he discusses how banks, being centralized providers of financial lifeblood to market participants, can deprive entire industries of this lifeblood and, in so doing, effectively ban or curtail their growth. In other words, banks, though ostensibly private firms, often function as extensions of the state (bank charters are difficult to get, after all) and, historically, governments have been able to act through banks without actually having to pass laws.

Perfectly legal businesses are essentially deprived of the ability to operate not by legislation, which must pass constitutional muster, but, at the urging of the state, by private banks who aren’t burdened with the same constitutional constraints.

Carter notes that this is, at the end of the day, a form of censorship, and cautions both political parties on celebrating censorship of disfavored industries or ideological opposition, as the pendulum inevitably reverses course, and unintended consequences inevitably ensue. In his words, “censorship, once normalized, always strays from its initial confines.”

The moral of the story is that our financial infrastructure should be neutral. The implication, of course, is that Bitcoin helps fix this, being an inherently neutral technology that de-monopolizes the power of centralized financial intermediaries.

4. “Here’s Why Bitcoin Will Rejuvenate Your Hope In Life,” an article by Josef Tetek. This article really resonated with me this week. Given all that’s happening in the world, it is easy to feel discouraged, to feel that we’re living on the precipice of a great disorder, and to feel as though the future may hold more darkness than promise. Tetek provides valuable perspective.

He first discusses the horrors of living through much of the 20th century in Czechoslovakia. Next, he enumerates some of the exponential gains in human progress made in the past 100 years which, despite the aforementioned horrors of the 20th century, offer some hope for continued progress in the future. We’ve obviously made major advances on issues like hunger, global poverty, access to water and sanitation, etc.

“The last great problem” to tackle, however, is the problem of fiat money. Tetek discusses how fiat money is essentially a form of central planning and, as the 20th century has taught us, central planning has deeply negative and oppressive downstream effects, many of which he discusses.

Until Bitcoin, Tetek asserts, there wasn’t much hope to “fix the money,” which would, in turn, help fix many of the remaining problems in the world.

“Today, we have an option to opt out of monetary central planning no matter where we live. We can literally take money into our own hands, while relying on no one and preserving our privacy.

And that is a reason to be optimistic.”

5. Aarika Rhodes on the Swan Bitcoin Podcast. Aarika Rhodes is an elementary school science teacher running against Brad Sherman for California’s 30th Congressional District in 2022. She talks about the importance of financial literacy in schools, how Bitcoin forces you to learn about money and why cutting out exploitative financial intermediaries is important. She’s joined by Alex Gladstein, and they’re hosted by Brady Swenson (@CitizenBitcoin). Together they discuss the discriminatory machinery of the current, legacy financial system, in terms of both racial discrimination and favorable treatment for the already-wealthy.

In the last 30 minutes of the episode, Gladstein discusses the importance of Bitcoin in (and as) politics.

“We need to understand that Bitcoin is the thing that’s going to change the system. Some policy is not going to change the system. Replacing this person with that person is not going to change the system. But Bitcoin becoming a bigger part of our lives and our social contract - that’s what’s going to change the system.”

-Alex Gladstein

Headlines/News

Infrastructure bill update

If you’re just joining us this week, the quick background here is: Congress is trying to pass a massive infrastructure bill. The bill is thousands of pages long and has all sorts of stuff in it. At the last minute, a provision was inserted that would expand the definition of “broker” in the tax code to include pretty much everyone operating in the crypto space, many of whom do not perform anything remotely resembling a broker-like function. Being deemed a “broker” subjects one to certain tax reporting requirements. Many in the crypto space who would be deemed “brokers” under the new law do not have the information with which to comply with these requirements because they don’t perform broker-like functions. The end result would be software developers, miners, validators, etc. potentially operating illegally under the letter of the law, though the proposed changes would not ultimately be implemented until 2023. There was a lot of debate in the Senate, and an amendment to fix the language relating to crypto in the bill was eventually offered for unanimous consent. The consent failed when Senator Richard Shelby objected to it on unrelated grounds. So now the bill is in the House of Representatives.

This week, the House Rules Committee established a process that won’t allow any amendments to the bill. Instead, the bill is set for a floor vote on September 27. It should be noted that these rules were established despite vigorous calls from both Republican and Democratic lawmakers to fix the language in the bill relating to cryptocurrency.

Thus, the path forward for crypto advocates is likely through another legislative vehicle. Representative Anna Eshoo, a Democrat from California, released a statement on Tuesday, saying: “I continue to explore all options to improve the flawed cryptocurrency language in the Senate’s bipartisan infrastructure bill, including through the budget reconciliation process or standalone legislation.”

On Thursday, Republican Senator Pat Toomey, said “rather than trying to ignore or suppress cryptocurrency and related technologies, regulators and legislators alike need to recognize that open, public networks are here to stay. Our laws and regulations must adapt to these developments.” He is soliciting legislative proposals that protect investors while still promoting and cultivating the growth of the space.

This week, Treasury Department officials sought to assure the crypto community that they do not intend to target those who would be unable to comply with the law. Obviously, these assurances were (and should be) taken with a metric ton of salt, given the Treasury Department’s not-so-veiled distaste for cryptocurrencies and its behind-the-scenes lobbying during the debate in the Senate.

Representative Darren Soto introduces two bipartisan crypto bills

This week, Representative Soto, a Democrat from Florida, introduced the Virtual Currency Consumer Protection Act of 2021 and the U.S. Virtual Currency Market and Regulatory Competitiveness Act of 2021. Both bills are co-sponsored by Representatives Ro Khanna (a progressive Democrat), Ted Budd (a Republican), and Warren Davidson (a Republican). Additionally, Republican Representative Tom Emmer also co-sponsored the U.S. Virtual Currency Market and Regulatory Competitiveness Act of 2021.

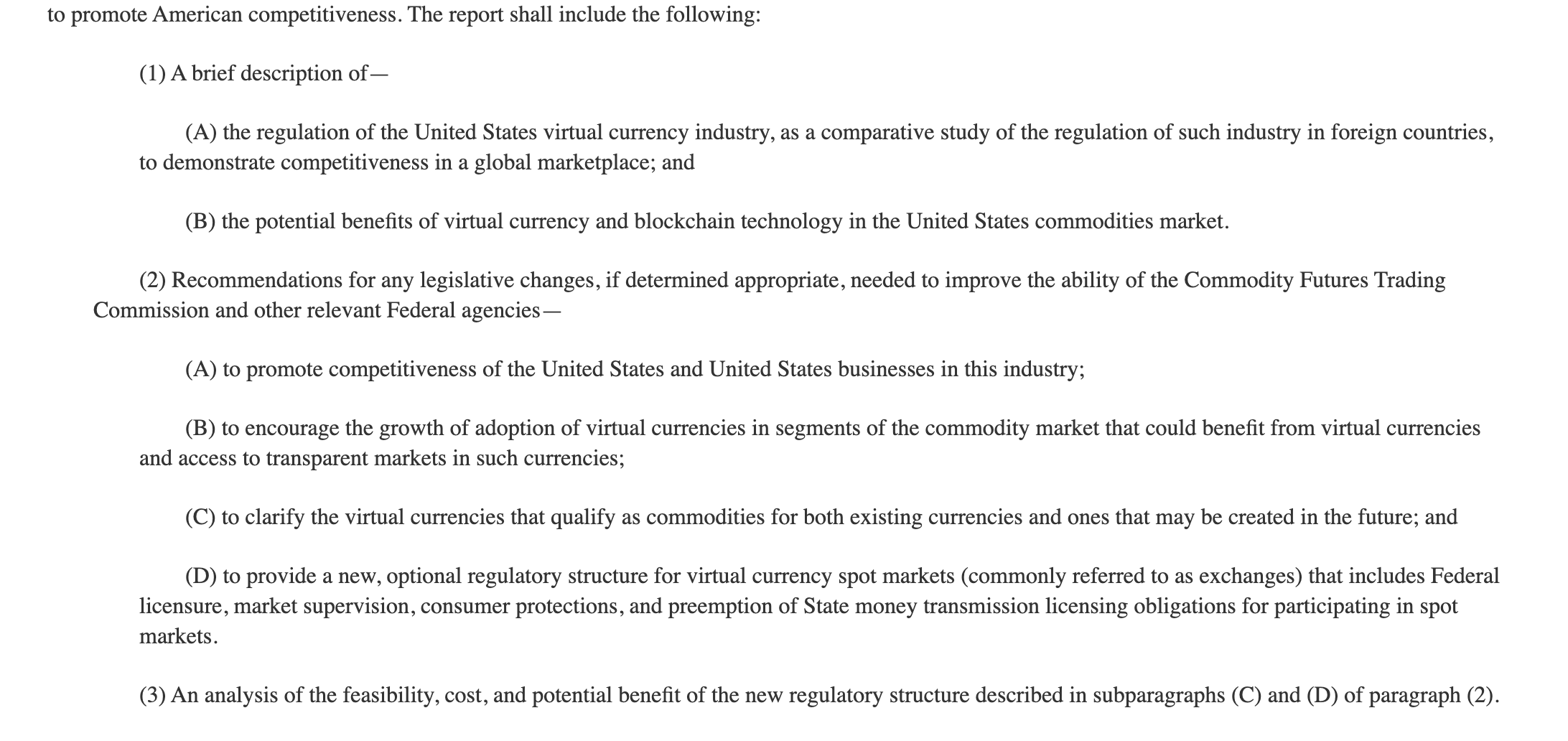

What do these bills do? The Virtual Currency Consumer Protection Act of 2021 directs the Commodity Futures Trading Commission (the CFTC) to produce a report describing how price manipulation could happen in digital asset markets and make recommendations for regulatory changes to improve the CFTC’s ability to prevent manipulation.

The U.S. Virtual Currency Market and Regulatory Competitiveness Act of 2021 directs the CFTC to produce a report comparatively studying the regulation of virtual currency in other countries and, per Representative Soto’s website, '“make recommendations for regulatory changes to promote competitiveness in the U.S. by providing regulatory clarity and examining alternatives for current burdensome regulations that may inhibit innovation.”

Take a look at the some of the text of this bill below. Notice it asks the CFTC to recommend legislative changes “to promote competitiveness of the United States and United States businesses in this industry” and “to encourage the growth of adoption of virtual currencies.” This tone is important. This is about promoting innovation in the United States, cultivating the growth of the industry, and being a global leader in the space. This is a stark departure from some of the rhetoric we’ve seen out of the Treasury Department and certain (though not all) Democratic members of the Senate.

As I’ve said before, concerns about the U.S. attempting to “ban” cryptocurrency dissipate more and more every day. The battle is about the manner of regulation - not whether the industry should be “banned” or summarily outlawed which, as we’ve noted before and as members of Congress seem increasingly to understand, would be ineffective and counterproductive. It’s heartening to see lawmakers from both sides of the political aisle encouraging intelligent regulation that allows the space to grow and develop here in the U.S.

Do I think this means we’re in for smooth sailing on the regulatory front? No, it does not. Frankly, I think the battles are just beginning, and there are plenty of unelected officials (Treasury Department, SEC, CFTC, etc.), many of whom harbor contempt for crypto, who continue to try to stake out their own respective purviews of authority with respect to the space. But do I think the bipartisan efforts we’ve seen in Congress over the past few weeks bode well? I’m cautiously optimistic. And is it necessary to go through these battles for the continued growth and adoption of crypto? Yes.

Perhaps more importantly, in terms of societal organization and governance, I think the growth of crypto is and will continue to present the Treasury Department and the executive branch, generally, with some uncomfortable questions (for them, at least) regarding the coupling/decoupling of money from the state. Remember that the government and its fourth, shadow branch, the central bank, wield massive, monopolistic power over fiat money. That power, as with all state power, is not going to be eagerly relinquished or reduced.

Deloitte survey reveals most executives view crypto as strong alternative to fiat

On Monday, Deloitte released its 2021 Global Blockchain Survey. They surveyed 1,280 senior executives and practitioners from all over the world (a third of whom are U.S.-based), and a whopping 76% said they think digital assets will be a "strong alternative to or replacement for" fiat in the next five to 10 years. That’s more than three quarters of respondents.

Another 78% said that digital assets will be important to their industry in the coming 24 months.

One major takeaway here is that the majority of institutions are no longer looking at Bitcoin (or crypto, generally) as tulip mania or some passing market fad. This has been obvious for some time, but the survey results do some work nailing these sentiments to time horizons. 76% of respondents said they think digital assets will be a “strong alternative to or replacement for” fiat in the next five to 10 years.

Five to 10 years is not a long runway, and I think this speaks to more than just the rapid pace of technological innovation in the space. It speaks additionally to the equally rapid pace of fiat currency debasement, which has been dramatically accelerated by the COVID-19 pandemic and the unprecedented expansion of the money supply undertaken to hold up the global economy. Fiat currency is debasing itself just as quickly as new monetary technology is advancing upon it. Institutions are clearly seeing this and starting to wake up to its ramifications.

It’s also worth reminding ourselves that the era of pure fiat currency has only been in existence for about 50 years. It is not a law of the universe that this era persist for the next 50.

Jack Dorsey wants to build a decentralized Bitcoin exchange

On Friday, Jack Dorsey announced that “TBD”, the division of Square working on an open developer platform, wants to create a decentralized exchange for Bitcoin. Specifically, they want to make it easier for folks to move straight into holding their own Bitcoin, as opposed to setting up an account with a centralized exchange (e.g. Coinbase), exchanging fiat for crypto, keeping the crypto on the exchange, or eventually sending it off the exchange to a self-custodied wallet. Square wants to remove some of these steps and, most importantly, remove the need for the centralized exchange.

For the new and new-ish

Last week we introduced Proof of Work (“PoW”) at a high, general level (and I highly encourage you to revisit last week’s issue before continuing here). PoW is the process by which network members compete to be able to write announced transactions (aka the next block) into the ledger (aka the blockchain). Remember, each block in the chain contains transactions that have been announced and validated.

This week, we’re going to do a high-level overview of the validation process, talk a bit about how new bitcoins get minted, and then conclude by talking about Bitcoin’s 21,000,000 supply cap.

So, as we discussed last week, bitcoin miners use specialized computers to attempt to “win” the right to record new transactions into the shared ledger. But we noted that these transactions must be validated before being formally appended to the blockchain as the next block. What does validation mean and entail?

Let’s recall how mining works, first. The process of bitcoin mining is expensive and energy-intensive. Miners, through their computers, use energy to continuously run the list of proposed transactions, along with some other info, through something called a hash function, to get an output. The goal is to get an output that falls within a range pre-determined by the network. The first miner to find an output that falls within this range wins. The process of “finding” an output is random. You just keep running the inputs through the hash function and hope you get an output within the range. The more computing power you have and use, the higher your chances of arriving at that number first.

Personally, I visualize this process as taking information I want to publish to the ledger (the announced transactions) and bundling it together in a suitcase. I then take my suitcase and slide it on the conveyor belt through a machine like the ones you see in airport security. When the suitcase comes out the other side, it’s been converted into a number. If that number falls within a certain range, I win. The “machine” in this analogy is the sha256 hash function we introduced last week. The inputs are the transaction info. The output is a number. The inputs go in looking one way and come out as a number.

So far so good. That’s the hard part. Once a miner wins, the transactions that the miner sent through the sha256 hash function have to get validated to make sure they’re not violating the rules of the protocol, there were no double-spends, etc. Think of this as akin to when airport security agents open your suitcase up and look through it to make sure nothing illegal made it through the machine.

Who validates the transactions? Every member of the network who operates what’s called a node, which is just a computer running the Bitcoin software. Nodes communicate with other nodes on the network, keep the ledger up-to-date, and enforce the rules of Bitcoin. Unlike the mining process, which requires energy and is difficult, validating is easy. Anyone can run a full node from his or her home, and there are nodes running all over the world at any given time. No exorbitantly expensive equipment is required. The Bitcoin software on a node makes sure everything looks right in a proposed new block. If so, the block gets appended to the chain. If not, the block is rejected.

Important to note here are the incentives. Because mining requires real-world energy, which costs money (electricity costs money), it is not in the financial interest of a miner to present a block containing false transactions. Doing so will result in the block being rejected, thereby wasting the energy costs spent by the miner. It also means the miner will not get the reward for adding a valid new block, which is a reward of new bitcoins, as well as transaction fees. So the incentives are such that it is very much in the financial interests of miners to be honest.

With respect to new bitcoins, you may have heard that Bitcoin has a maximum supply of 21,000,000, meaning that there can only ever be 21,000,000 bitcoins. How does this work if new bitcoins are created with every new block? The amount of new bitcoins minted with each block is cut in half every four years. Each such event is referred to as a “halving,” and Bitcoin follows a “halving” schedule.

When Bitcoin first began, a successful miner received 50 new bitcoins for a new block. In 2012, this reward was reduced to 25. In 2016, it was reduced to 12.5, and in 2020 it was reduced to 6.25 new bitcoins per block. In this way, the supply of new bitcoins slows and diminishes until the last bitcoin gets mined in approximately 2140. Unlike fiat currency, Bitcoin’s supply cannot be inflated, expanded, or accelerated in contravention of the halving schedule.

Bonus/Miscellaneous

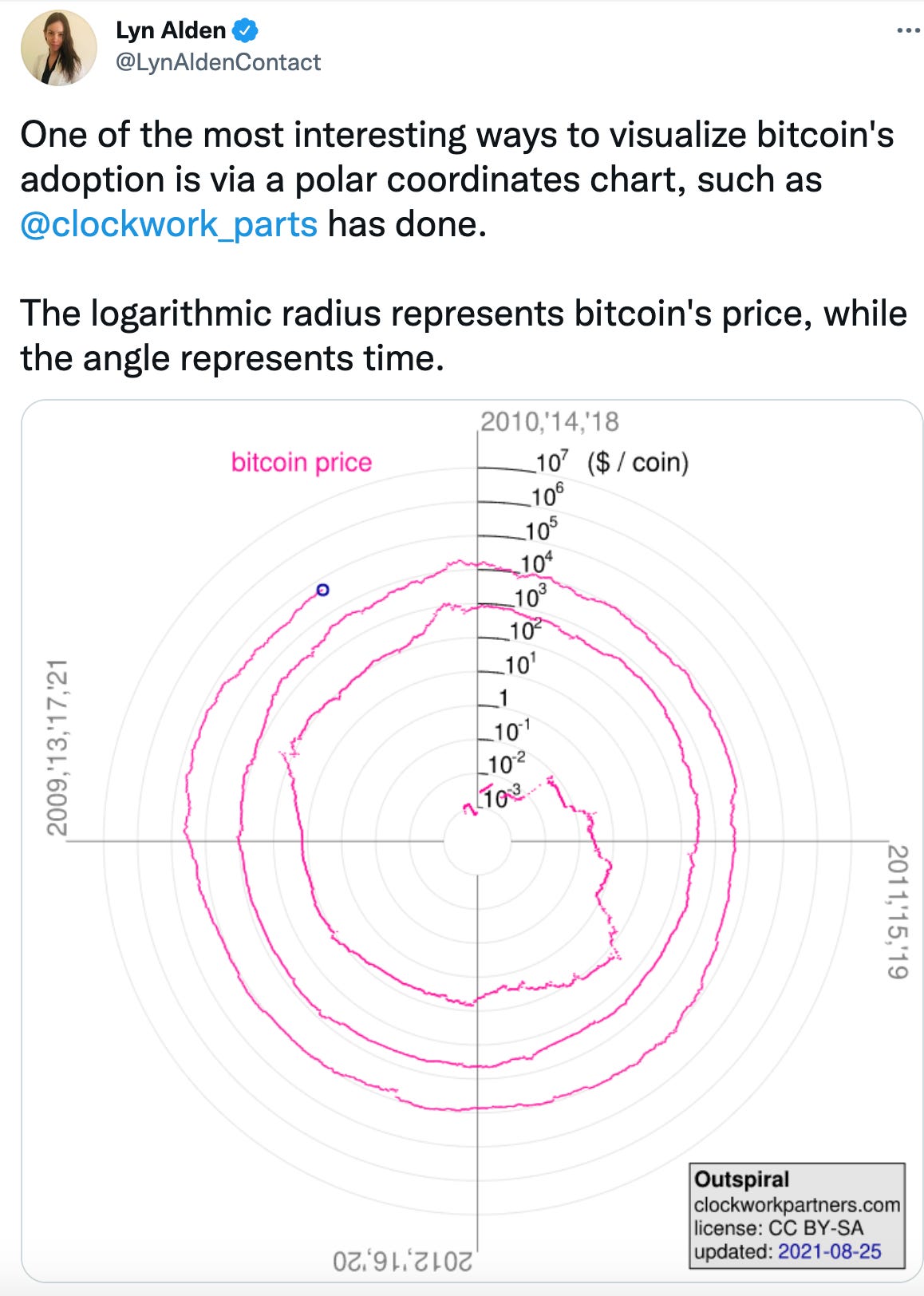

If you follow me on Instagram (@TheWhyOfFI), you know I talk a lot about how things are obviously getting more expensive, but only in dollar terms. In other words, we measure price with a unit of account that loses value and is debased over time through inflation. But what happens when we measure things with a different, better unit of account?

Lyn Alden tweeted these fascinating charts showing (1) Bitcoin’s adoption and monetization over time, (2) how other commodities have gotten cheaper in Bitcoin terms, and (3) how the S&P itself has gotten cheaper in Bitcoin terms:

Credit to Clockwork Partners (@clockwork_parts) for the charts.

This visual representation of Bitcoin’s adoption and the way in which everything gets cheaper in Bitcoin terms made me think of these relevant charts created and tweeted by Ecoinometrics (@ecoinometrics):

The takeaway is that if your unit of account is Bitcoin, the world is getting less expensive. If you like these charts, check out the Ecoinometrics Substack.

As always, thanks for reading this week! If you enjoyed it or found it useful, share this newsletter widely and freely!

See you next week,

Logan

“Civilization is in a race between education and catastrophe. Let us learn the truth and spread it as far and wide as our circumstances allow. For the truth is the greatest weapon we have.” -H.G. Wells

SOCIAL

DISCLAIMER: I am not investment advisor and this is not investment advice. This is not, nor is it intended to be, a recommendation to buy or sell any security or digital asset. This newsletter exists for educational and informational purposes. Do your own research before making any investment decisions.

© Copyright The Why of FI.