Think Bitcoin™ Issue #35

The Bear Market Issue: How We Got Here, Where We're Going, and How to Survive and Thrive

Hey friends, welcome back to Think Bitcoin™ for issue #35. Happy Father’s Day to all the dads out there! And special welcome to the new subscribers. I’m glad you’re here. As always, if you have any questions or comments, feel free to reach out. You can also find me on Twitter (@TheWhyOfFI).

In this issue:

Long Reads: How to Approach, Survive, and Think About this Bear Market

Content Round-Up: 2 articles

FAQ: If Bitcoin is an “inflation hedge” then why is it going down right now?

As always, if you find this newsletter interesting or useful, please share it with others who might find it interesting or useful, too!

Long Reads

How to Approach (and Survive) a Bear Market

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of light, it was the season of darkness, it was the spring of hope, it was the winter of despair.”

-Charles Dickens, describing the volatility of crypto markets

Well, friends, we find ourselves in that oh-so-dreaded, yet also (in hindsight) inevitable, bear market.

It’s no secret that these markets are (at least historically) savagely cyclical. Throughout this current cycle, however, there have been some prominent, vocal skeptics of this cyclicality. Some posited that we may be entering a “supercycle,” or that, due to institutional involvement, drawdowns would become increasingly shallow. These overly sanguine takes have turned out to be profoundly incorrect. And the speed of the current downswing has certainly caught even some of the most grizzled Bitcoin veterans by surprise.

So what happened? How did we get here? And is this time different?

Put simply, we’ve run up against intractable macroeconomic headwinds and destabilizing geopolitical developments, the market effects of which have revealed vulnerable protocols and parties in the broader crypto world.

Inflation obviously remains a problem. The May CPI print came in at 8.6%, hotter than consensus expectations and not showing meaningful signs of moderating. Food was up 10.1% year-over-year, and energy was up 34.6% year-over-year. Fuel oil, specifically, was up a breathtaking (and painful) 106.7%.

The food and energy situation globally is pretty bleak:

A big part of this is obviously the Russian invasion of Ukraine. As I’ve written about before, Ukraine and Russia are both top-5 exporters of wheat. War does not make for good harvests. Russia is also a significant exporter of fertilizer, which is obviously pretty important for agriculture.

By now I think we’re all familiar and well-versed on just how dependent the world is on Russian energy and how much leverage that affords Putin, especially over Europe.

This is all contributing to a trend toward deglobalization, which is inflationary. And this is all happening on the heels of the largest expansion of the money supply in U.S. history, which is also highly inflationary.

Finally forced to acknowledge that inflation is not, in fact, transitory, the Fed is now on a mission to tame it and bring it back under control. So they’re raising rates aggressively and looking to shrink their balance sheet. Basically the only thing the Fed can do is try to destroy demand in order to reduce spending. They can’t produce more oil, harvest more wheat, produce more baby formula, etc. All they can do is create an environment designed for us to spend less. The more aggressively they pursue this end, the more likely a recession becomes.

Recently, White House Press Secretary Karine Jean-Pierre said “the economy is in a better place than it has been historically and so we feel that we’re in a good position to take on inflation.” Fed Chair Jerome Powell, for his part, echoed this sentiment last Wednesday when the Fed raised rates by 75 bps, saying that the economy was in a “strong position.”

These proclamations of economic strength are a bit curious, however, given that real GDP growth in Q1 was negative and the Atlanta Fed’s GDP Nowcast is estimating 0% real GDP growth in Q2. This is also the third bear market for U.S. markets in the last four years, a notable departure from historical frequency:

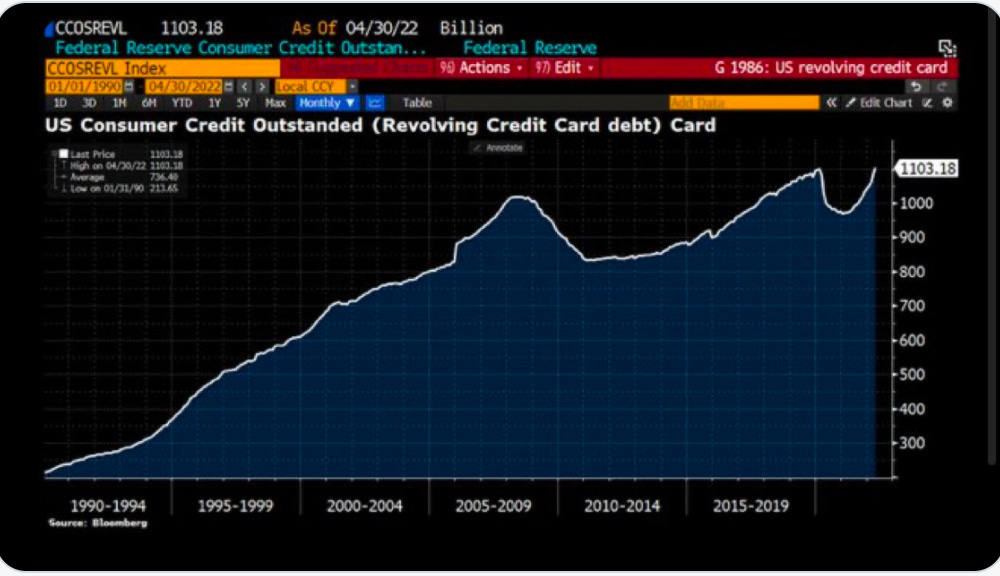

It’s also worth noting that consumer credit card debt is rising again:

And lastly worth noting that homeowners with variable-rate mortgages are going to find themselves in increasingly dire circumstances if the rate-hiking continues. 30-year fixed mortgage rates are also rising rapidly, pricing many people out of the market and reducing demand, which will obviously affect the historically inflated housing market.

Apparently this is the “strong” environment into which the Fed is going to keep hiking rates. But this is where we are.

In addition to having a macro outlook that does not inspire a lot of optimism and which is weighing heavily on asset prices, we also have shenanigans in the broader crypto market dragging the whole digital asset space down.

First, there was the Luna debacle, which I briefly touched on in the last issue. That poorly designed system led to the Luna Foundation Guard becoming forced sellers of all their Bitcoin reserves as a result of their algorithmic stablecoin losing its peg. If that sounds like gibberish to you and you’d like a more in-depth explanation, I’d recommend this piece by Nic Carter and Allen Farrington, this piece by Cory Klippsten and Sam Callahan, and also this piece by Namicos.

Then Celisus announced it was suspending withdrawals from its platform indefinitely, as rumors swirled about its solvency. For more information on this particular meltdown, see this in-depth piece from Dylan LeClair and Namicos. This has also led to questions being posed to similar platforms like, most prominently, BlockFi.

Three Arrows Capital, a crypto investment fund, got margin-called. Babel Finance, a crypto lender based out of Hong Kong, is suspending withdrawals because, according to a statement they issued, they’re “facing unusual liquidity pressures.” Mike Alfred has forcefully and cogently argued that HEX, another crypto, is a ticking time bomb. Which is all to say there is contagion, and it is spreading. I’m sure we’ll see more blow-ups before this cycle is over. As Warren Buffett said, “Only when the tide goes out do you discover who's been swimming naked.”

I do want to highlight the fact that many Bitcoiners were essentially shouting from the rooftops on Twitter and elsewhere for folks to abandon many of these projects well before their respective implosions. Cory Klippsten, Swan Bitcoin’s CEO, has been vociferously and relentlessly calling out Celsius for weeks and warning Celsius users of the platform’s impending struggles. Mike Alfred has been (and continues) beating the drum on HEX’s inevitable demise for weeks, as well.

The combination of macro headwinds and crypto market fireworks has driven digital asset prices down and will likely continue to drive them down for the foreseeable future.

But is this cycle different from previous cycles?

In some ways, yes. The speed at which the Fed is hiking rates right now is not an environment the digital asset space has seen before. So, in that sense, this cycle is different. But while previous cycles seemed to lose steam endogenously, it’s worth reflecting on the fact that the current bear market is mostly the result of exogenous, macroeconomic factors that are also weighing heavily on the stock market.

Sure, as discussed above, there have been some notable blow-ups within the crypto world (and there will likely be more), and they will put downward pressure on Bitcoin by association. But there’s no real, serious question about Bitcoin’s legitimacy or staying power anymore. It’s a macro asset now, and it’s affected by macro headwinds. And as long as investors and institutions are looking to de-risk ahead of a widely expected recession (and we may actually already be in a recession), assets perceived to be the farthest up the risk curve will be the first to get jettisoned.

Okay so when does the pain stop?

I think the beatings will likely continue until the Fed pumps the breaks on rate-hiking and quantitative tightening. What might cause them to feel comfortable doing that? Well, Powell has been emphatic recently about the Fed’s commitment to bringing down inflation, describing it to Congress as “unconditional” on Friday. In the FOMC statement on Wednesday, the committee said it “is strongly committed to returning inflation to its 2 percent objective.”

Given this posture, I think we’re likely in for a protracted period of pain and sideways chop. Either inflation moderates and the Fed can take its foot off the tightening pedal or the Fed is compelled to take increasingly aggressive measures to forcefully bring inflation down. The former means a shorter bear market period. The latter means a more prolonged bear market period.

There are credible arguments to be made for either scenario. What is clear, however, is that this is not going to be a March-2020-style, lighting-fast V-shaped recovery spurred by abrupt and colossal infusions of liquidity from central banks. The Fed is focused on taming inflation - not on propping up markets- so no infusions of liquidity are imminent. The explicit current objective is instead to actively withdraw liquidity.

The joke of it all is that the inflation the Fed is currently fighting is largely the result of the liquidity bazooka the Fed launched at the economy during the pandemic to save us from a recession. And now the Fed finds itself in the unenviable position of having to engineer a recession in order to save us from the inflation created by the measures it took to save us from prior recession. It will likely be forced to return to quantitative easing to save us from this new recession. In other words, the cures create new maladies.

It’s worth asking yourself if such a system is sustainable, worth saving, or beneficial to anyone other than wealthy asset-holders.

How to keep perspective and stay sane:

First, reacquaint yourself with this chart:

Second, realize that Bitcoin’s death has been declared hundreds (if not thousands) of times over the course of its existence. During the crash phase of each of the previous cycles, pundits and financial “experts” have danced on what they perceived and proclaimed to be Bitcoin’s grave. Bitcoinisdead.org has kept an extensive record of these obituaries. Here are just a few examples of the doom and gloom during the last cycle crash (with the price of Bitcoin at the time listed to the right of the date):

(screenshots from Bitcoinisdead.org)

Here’s a gem from Peter Mallouk in Forbes on December 7, 2018:

And from Jeff Schumacher on January 23, 2019.

The point is that people have been predicting Bitcoin’s demise for almost 13 years. As dark and pessimistic as sentiment seems to be currently, we have been here before.

Also remember that, despite this significant drawdown, Bitcoin remains by far the best-performing asset in any 3-year period over the last decade.

What should I be doing to thrive in this market?

1. Keep a LONG-term mindset. If you’re not prepared to hold Bitcoin for years, you’re going to be emotionally pulverized every bear market.

2. Build a deeper understanding of WHY Bitcoin exists and the purposes it's serving.

This means keep your eyes on the future we’re working to build! Use this time to re-devote yourself to learning. In a bull market, everything moves quickly, hype reaches a manic euphoria, FOMO is ubiquitous, noise drowns out signal, and it becomes exceedingly difficult to just sit down and sedulously learn.

In bull markets, mere sentiment masquerades as conviction. Bear markets are where real conviction gets built.

3. Focus on all of the positive use-cases and growing adoption of Bitcoin across the world.

4. Connect with other Bitcoiners! Reach out and connect with people who have been through a bear market or two (or three).

Content Round-Up

1. “Letter in Support of Responsible Crypto Policy.” This letter was written to the United States Congress by 21 human rights activists from 20 different countries. As I mentioned above, it’s important to foreground and keep top-of-mind the human rights case for Bitcoin. In this letter, human rights activists urge Congress to take an “open-minded, empathetic” approach to Bitcoin, which is increasingly serving as a vital monetary tool for so many:

“We can personally attest — as do the enclosed reports from top global media outlets — that when currency catastrophes struck Cuba, Afghanistan, and Venezuela, Bitcoin gave our compatriots refuge. When crackdowns on civil liberties befell Nigeria, Belarus, and Hong Kong, Bitcoin helped keep the fight against authoritarianism afloat. After Russia invaded Ukraine, these technologies (which the critics allege are “not built for purpose”) played a role in sustaining democratic resistance — especially in the first few days, when legacy financial systems faltered.”

2. “How Bitcoin Can Unlock the Energy of the Ocean for 1 Billion People,” an article by Level39. If you’re looking for some (dare I say) optimism about the climate and how Bitcoin can be leveraged to unlock innovative climate solutions, this is an utterly fascinating piece by the great Level39 about a technology called Ocean Thermal Energy Conversion (OTEC), and how Bitcoin can potentially make it feasible to implement on a global scale.

FAQ

If Bitcoin is an “inflation hedge” then why is it going down right now?

I’ve been seeing this question a lot lately, sometimes as a sincere inquiry, but more often as trolling. Here’s the deal. There are different types of inflation (as Lyn Alden has so thoroughly and eloquently explained here). It’s common for folks to talk about CPI, which is just consumer price inflation (which measures the change in prices of goods), as if it is the one and only all-encompassing measure of inflation.

The more traditional economic definition of inflation is actually the growth of the money supply. This is what central banks do. When they want to “rescue” an economy from a recession they tend to do this quite dramatically and on an enormous scale. But every time the money supply is inflated, it devalues the currency.

The idea of Bitcoin as an inflation hedge involves this latter definition of inflation and not merely CPI. As is apparent from the chart below, Bitcoin has served as a hedge against inflation of the monetary supply:

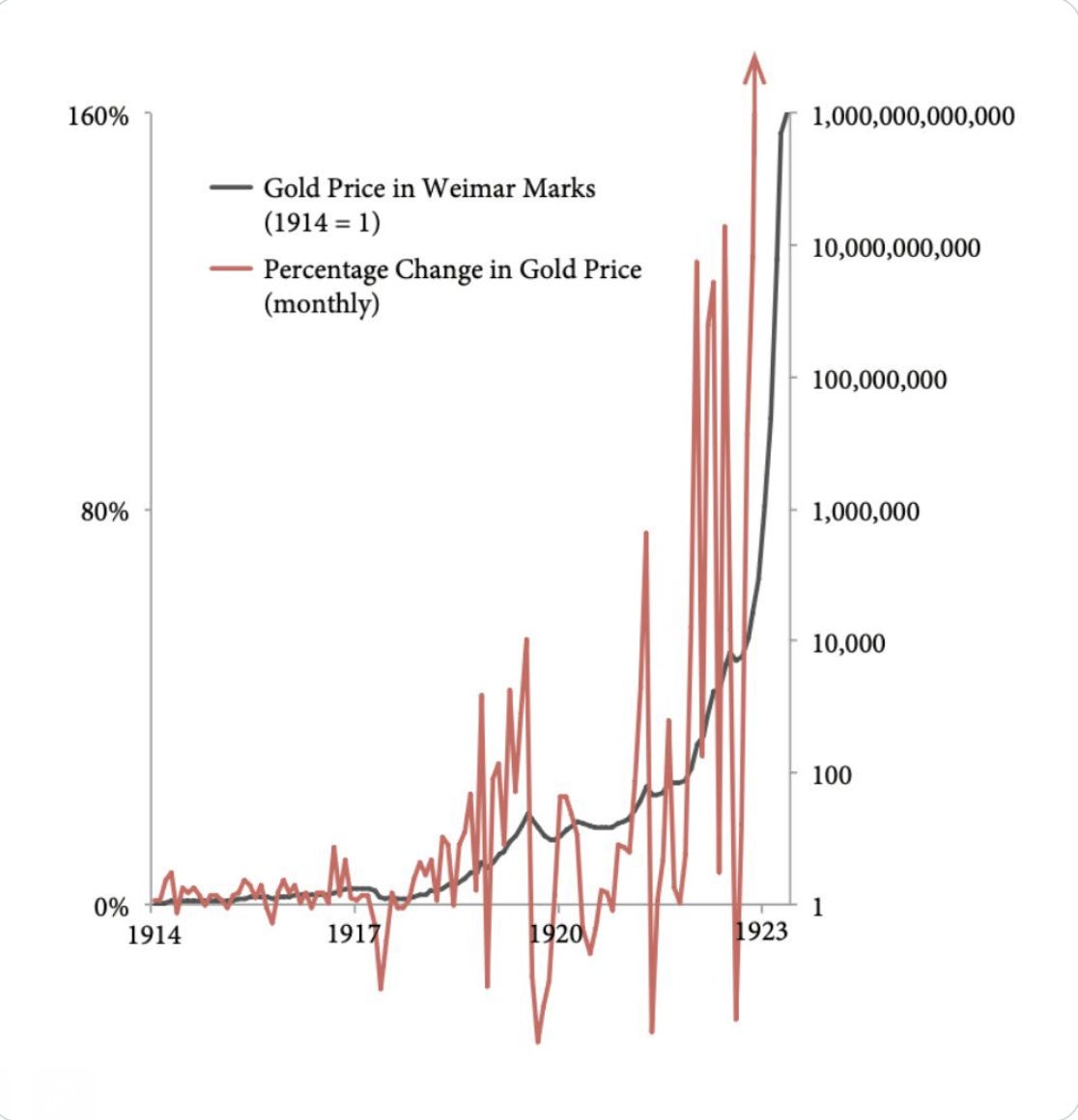

So if your view is that central banks will have to continue expanding the money supply in order to deal with a global debt to GDP that’s over 250% and to prop up increasingly fragile economies, Bitcoin will continue to rise, albeit in volatile way. See, for example, a chart of gold (a hard money) vs. the German mark (a constantly devalued money) in Weimar Germany:

It was not, as you can see, a straight line up for gold, which was clearly the superior money and superior store of value. It was instead a wild and turbulent ride up, with huge drawdowns and explosive upswings.

Now, I’m not arguing that the U.S. is going to hyperinflate. But it’s useful to see the interplay of a hard money and a money that’s being devalued rapidly.

Miscellaneous

Speaking of focusing on positive developments in the Bitcoin space, Jay-Z and Jack Dorsey teamed up to create The Bitcoin Academy, a free, educational program for residents of Marcy Houses in Brooklyn.

As always, thanks for reading! If you enjoyed it or found it useful, share this newsletter widely and freely!

“Civilization is in a race between education and catastrophe. Let us learn the truth and spread it as far and wide as our circumstances allow. For the truth is the greatest weapon we have.” -H.G. Wells

See you in two weeks,

Logan

SUPPORT

Send bitcoin to my Strike

SOCIAL

DISCLAIMER: I am not investment advisor and this is not investment advice. This is not, nor is it intended to be, a recommendation to buy or sell any security or digital asset. Nothing in this newsletter should be interpreted as a solicitation, a recommendation, or advice to buy or sell any security or digital asset. Nothing in this newsletter should be considered legal advice of any kind. This newsletter exists for educational and informational purposes only. Do your own research before making any investment decisions.

© Copyright Logan Bolinger