Think Bitcoin™ Issue #3

Bitcoin and politics; Bitcoin in Africa; We're still early; Regulatory update; Intro to Proof of Work

Hey friends, welcome back to Think Bitcoin™. As always, if you’re brand new or relatively new to Bitcoin and looking for some education on the basics, feel free to scroll down to the “For the new and new-ish” section and work your way up.

In this issue:

Content Round-up: 3 articles, 1 podcast, 1 short film

Headlines/News: Infrastructure bill / blockchain bill / Kashkari trashes crypto / Former SEC Chair Clayton joins Fireblocks / Quintenz steps down / SEC Chair Gensler again seems to target DeFi / global crypto adoption

For the new and new-ish: An intro to Proof of Work

As always, if you find this newsletter interesting or useful, please share it with others who might find it interesting or useful!

Content Round-Up

1. “The Bitcoin Revolution in Africa: Explained,” a short 16-minute film, based on the article, “Check Your Financial Privilege,” by Alex Gladstein. Too often when we think of Bitcoin, we think primarily of wealthy Silicon Valley bros, computer nerds, or investment firms. We think of wealth-seeking individuals looking to get rich with an exciting new asset.

And this is because we live with and under the financial privilege of a comparatively stable currency in the U.S. dollar and are not ruled by an unelected authoritarian regime. We fail to appreciate the percentage of the world living with extremely unstable, hyper-inflating currencies and under authoritarianism. For people in these situations, Bitcoin serves a much more fundamental, much more important purpose. It allows people to save their money in an undebaseable unit of account and to transfer value without exploitative government intervention (and also without government surveillance).

The film (and the article) examine Bitcoin adoption and use in Nigeria, Sudan, and Ethiopia, respectively.

2. “Why Bitcoin’s Network Effect Can’t Be Neutral,” an article by the pseudonymous Medium account, The Progressive Case For Bitcoin. The author makes the case that, though the Bitcoin network itself is inherently (and crucially) neutral, we should be doing more work to diversify Bitcoin’s network effects, meaning the folks who join the network, adopt Bitcoin, and onboard others. Bitcoin can function as an equalizing economic force, as it is open to all, devoid of discrimination, and free of gatekeepers. But for it to truly benefit those who have heretofore been marginalized or oppressed by legacy/traditional financial systems, these folks need to be onboarded early to benefit from the “first mover advantage.”

Some of the statistics in the article are contradicted by other surveys and sources of data, some of which show more significant and more encouraging adoption by both women and by historically marginalized populations. However, I think the main thrust of the piece is important. This is one of the few opportunities in economic history in which normal people get to front-run Wall Street and institutional money. Normally the best opportunities are reserved for the latter. So it’s important to make sure we’re spreading the word, amplifying diverse voices in the space, and bringing everybody to the table. And this starts with Bitcoin education.

3. “The Bitcoin Adoption Curve,” an episode of The Investor’s Podcast with Preston Pysh interviewing Croesus. Croesus is a pseudonymous Bitcoin thinker and writer, perhaps most famous for his article “Why The Yuppie Elite Dismiss Bitcoin.” In this podcast episode, Croesus discusses why many of his Ivy League MBA-type friends struggled initially to engage with Bitcoin and why many have since come around.

He also discusses how early we still are in terms of the arc of Bitcoin adoption. There are a lot of folks who look at Bitcoin now and think they’ve missed the proverbial boat, but Croesus explains why this is untrue by examining the classic tech adoption curve that network-effect technologies like the internet and social media have traveled in the past.

Lastly, he discusses the properties that make Bitcoin a revolutionary, epoch-defining technology and discusses the total addressable market of Bitcoin.

4. “50 Years After Going Off Gold, the Dollar Must Go for Crypto,” an article by Niall Ferguson in Bloomberg. Marking the 50th anniversary of President Nixon “temporarily” closing the gold conversion window, Ferguson argues that the U.S. should embrace crypto.

5. “The rich get richer the poor get Bitcoin,” an article by Bradley Rettler, a philosophy professor at the University of Wyoming. This one’s an old classic.

(Bonus) 6. “Inside Afghanistan’s cryptocurrency underground as the country plunges into turmoil,” an article by MacKenzie Sigalos, one of the few mainstream finance journalists who has engaged with the crypto space in good faith. She breaks down crypto in Afghanistan, its promise, and its current limitations.

Headlines/News

The infrastructure bill moves to the House; House reps reintroduce a blockchain bill

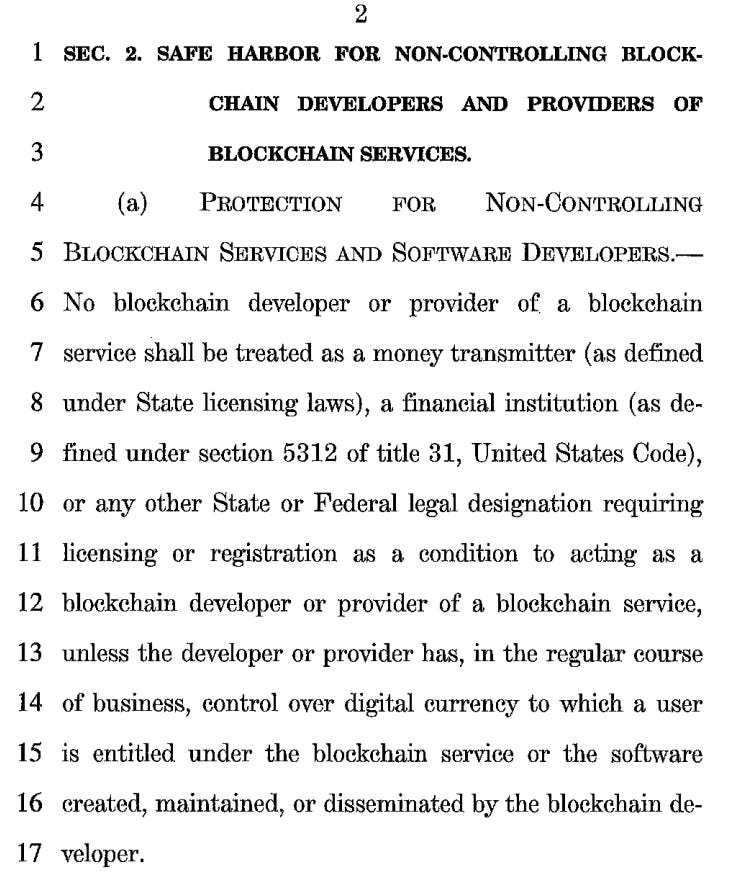

The infrastructure bill has moved to the House of Representatives, which will be back in session tomorrow, August 23. Meanwhile, Representative Tom Emmer reintroduced the bipartisan Blockchain Regulatory Certainty Act with Darren Soto. This bill would ensure that developers and blockchain service providers do not get classified as money transmitters, financial institutions, or “any other legal designation requiring licensing or registration as a condition to acting as a blockchain developer or provider of a blockchain service” unless the developer or provider exercises control over digital currency to which a user is entitled. See the language below:

Just like the infrastructure bill debates, a lot of the wrangling in Congress is over definitions, which crypto actors fall under which definitions, and what reporting/licensing requirements are triggered by each definition. Getting this right requires understanding the role each actor in the crypto space plays, which is why it’s so important that the crypto community spends focused energy on educating lawmakers.

Neel Kashkari excoriates crypto

Neel Kashkari, president of the Federal Reserve Bank of Minneapolis, made an appearance at the Pacific NorthWest Economic Region Annual Summit in Montana, and used the opportunity to say some pretty hostile things about bitcoin and crypto. Here are some of the juicier quotes from the appearance:

“So far what I’ve seen is … 95% fraud, hype, noise and confusion.”

This is obviously incorrect and sloppily hyperbolic.

“There are thousands of these garbage coins that have been created. Some of them are complete fraud Ponzi schemes. They dupe people into investing money and then the founders rip them off.”

This is not untrue. There are tons of scam coins and bad projects in crypto. But that doesn’t mean there aren’t also transformative projects. It’s a new, rapidly growing space. Like the internet in the 90s and early 2000s, there are good projects, and there are lots of crappy ones.

It’s also why we focus almost 100% of our energy here on Bitcoin. Bitcoin isn’t comparable to the good or bad projects in the internet boom. It’s comparable to the internet itself, upon and with which these projects, good or bad, were built.

“I always ask people what problem are you trying to solve and no one can articulate what the actual problem is.”

This just seems lazy. There is no shortage of intelligent, deeply-researched articulations of bitcoin’s use case(s).

On inflation: “I don’t see any evidence that the U.S. government or the United States of America is on a path to Venezuela.”

This from the man who once said there is literally “no limit” to how much money the Fed can pump into the economy. He’s missing the point, here. Few are arguing that the U.S. is on the brink of Venezuela-style hyperinflation, but is the increase in the money supply concerning? Yes. Is it clear that it will slow down in the next decade (or anytime in the foreseeable future)? No. The economy is clearly hooked on easy monetary policy and, since Americans now use the stock market as a savings account, I doubt the Fed will let the market suffer for any meaningful period of time. So what does this mean? Almost certainly more money printing.

It goes without saying here that Kashkari is also completely ignoring the 1.2 billion people who currently live under double- or triple-digit inflation. Or perhaps he’s just willfully ignorant with respect to economic conditions outside the U.S.

“I’ve not seen any use case other than funding illicit activities like drugs and prostitution.”

Again, tell this to all those living under inflationary currencies and authoritarian regimes. Tell this to political dissidents like Navalny in Russia. With respect to crime, Kashkari would do well to read “An Analysis of Bitcoin’s Use in Illicit Finance,” an independent research paper by Michael Morrell, former acting CIA Director.

Morrell admitted that when he began his research, he assumed the common, broad generalizations about bitcoin’s use in illicit activities were true. However, the results of his research led him to the conclusion that “the broad generalizations about the use of Bitcoin in illicit finance are significantly overstated.” Morrell noted that illicit activity comprised less than 1% of all cryptocurrency transactions form 2017 to 2020. He further noted that much more illicit activity is conducted using traditional finance.

“I have not seen any use case that is legitimate so far that bitcoin solves.”

I think it’s obvious that Kashkari is not a Think Bitcoin™ subscriber. Any readers with connections to Mr. Kashkari are hereby invited to share it with him.

SEC Chair Gensler again says DeFi can and should be regulated

In a Wall Street Journal interview on August 19, SEC Chair Gensler again noted that DeFi was not immune to regulation and oversight. We’ve been following Gensler’s attitude toward crypto since the inception of this newsletter, and it continues to be clear that he’s focused on DeFi and regulating what he views to be a sea of unregistered securities therein. Every week he’s talking about it.

Global crypto adoption growing exponentially

Chainalysis published a preview of its “Geography of Cryptocurrency” report on August 18. Worldwide crypto adoption has grown 880% this year. The top seven countries for adoption are Vietnam, India, Pakistan, Ukraine, Kenya, Nigeria, and Venezuela. The U.S. is number eight.

Jay Clayton joins Fireblocks board

Former SEC Chair Jay Clayton has joined the board of advisors of Fireblocks, a company valued at $2 billion that provides custody solutions for digital assets. Clayton is certainly not the first former top government official to move into the crypto space, but this is certainly notable. It signifies a maturing industry and an industry into which talent and expertise continue to migrate. Recall in May when John Dalby, the CFO of Ray Dalio’s Bridgewater Associates, left the firm to take a job with the New York Digital Investment Group (NYDIG). Recall also that former CFTC Chair Chris Giancarlo is now an advisor to BlockFi. And speaking of the CFTC…

Brian Quintenz stepping down as CFTC commissioner

Brian Quintenz announced that he’s stepping down from the CFTC on August 31. He noted he intends to announce a role in the private sector soon and that he plans to keep crypto “relevant” to his career. It seems obvious he is going to announce a role in crypto. He tweeted this earlier in the week, which was interesting:

Quintenz has been vocal in the past about cryptocurrencies being commodities and falling under the CFTC’s domain, as opposed to that of the SEC. It appears he’s thinking hard about DeFi and the concept of “investor protection,” and doing so in a radically different, more open, more thoughtful way than SEC Chair Gary Gensler. It’ll be interesting to see where Quintenz ends up.

For the new and new-ish

Last week we talked about some of the problems that emerge when you remove the middleman from the system. We discussed the double-spend problem, in particular. We noted that centralized intermediaries take care of these problems in our current system, and any alternative system would have to take care of them in a different way.

We continued to discuss what a distributed ledger looks like (everybody in a network has a copy of the ledger instead of only one centralized entity). We ended by acknowledging that this seemed kind of messy and unscalable because, in order for us to trust the other members of the network, we would have to know them pretty well and give them permission to join the network. In other words, we wouldn’t let just anyone join the network and have a copy of the ledger.

And this is where we got stuck. It seems impossible to create a scalable, decentralized network that can credibly maintain a shared ledger because we keep running into problems with trust and permission. Bitcoin solves this with computer science, cryptography, and math in a process called Proof of Work.

Don’t worry. I’m not going to get too granular on the details of the process because I’m not a computer science expert, nor am I particularly adept at math. I’m a word guy, not a numbers guy. So my goal is to just speak generally about the process. There are plenty of videos, articles, and books about Proof of Work (“PoW”) if you really want to get into the weeds, and I’ll direct you to some of these videos in subsequent issues when we go a little further with PoW.

PoW works like this: We have our network. Each member of our network has a copy of the ledger. This ledger is a blockchain. It’s a “chain” because we add new blocks to it, and each new block has to connect to the previous block. Each block contains transactions that have been announced on the network.

Any time anyone wants to make a transaction, they announce it to the network. But instead of each member simply recording the announced transactions into his or her respective copy of the ledger, members compete to see who gets to write the announced transactions into the ledger. In other words, members compete to see who gets to append the next block of transactions to the existing chain.

The winner gets to write the transactions into the next block and, if those transactions are valid (meaning, no double-spends, etc.), the winner gets rewarded with the right to mint a specific, programmed amount of new bitcoin, which he or she keeps. If the transactions are not valid, the block is rejected and the winner gets nothing. Everybody’s copy of the chain, which is the ledger, is updated when the winner’s block is validated.

So how do members compete? What is the competition? This is a whole tech-intensive can of worms known as “mining,” which is a concept you may have heard before. In the Bitcoin context, mining is obviously not picks and shovels in the ground. It involves the expenditure of energy to power computers. Miners use computers to run the list of announced transactions, along with some other info that we’ll explain next week (collectively, the input) through what’s called a hash function to get an output. Bitcoin uses a military-grade hash function called sha256. If the output is the first to fall within a certain programmed range, that miner wins and gets to write the transactions into the next block, provided the rest of the network validates the correctness of those transactions. If the output does not fall within the range, the miner’s computers keep trying. Eventually, a miner wins and gets to write the transactions in the next block and receive the reward for doing so, provided of course the block is validated.

We’ll dive into this process in more detail next week, but this is the very broad, bare-bones overview of PoW and mining. There is a ton of technical detail to each step I’ve radically and ruthlessly condensed here. We’ll go into some of those details next week, but we’ll still only be scratching the surface.

What I want to highlight, though, is that you don’t need to be a computer scientist or become a scholar of bitcoin mining to be in Bitcoin. It’s more important to know how the incentives in mining work and how PoW secures the network than it is to know all the technical details of how the sha256 function works. I want to disabuse you of any notion that you need to understand all the technical details of this process to be a part of the Bitcoin network and the Bitcoin community. I certainly don’t understand every single detail of the process, myself. But it’s good to have a general understanding to build upon, and I assure you it’s not more complex or recondite than our traditional financial system.

Bonus/Miscellaneous

1. Apparently Britney Spears has been using bitcoin since 2014.

2. Much ink has been spilled over the economic effects of Nixon taking the world off gold in 1971. Less ink has been spilled over the effects this has had on the food industry and, downstream, the influence it’s had on our collective diets. Saifedean Ammous, author of the canonical book, The Bitcoin Standard, wrote about this in his follow-up book, The Fiat Standard. Inspired by the latter, this young woman composed a rap about fiat’s effect on food.

Thanks for reading, this week! I’d love if you could share it with anyone you think might be interested. Maybe you have friends who are crypto-curious, maybe you have family members who ask you about Bitcoin, maybe you have coworkers who are into FI/RE and personal finance. Share this widely and freely. The goal of this newsletter is to spread knowledge, education, and interest in Bitcoin to as many people as possible, and it runs on word of mouth!

Have a great week,

Logan

DISCLAIMER: I am not investment advisor and this is not investment advice. This is not, nor is it intended to be, a recommendation to buy or sell any security or digital asset. This newsletter exists for educational and informational purposes. Do your own research before making any investment decisions.

Copyright © The Why of FI.