Think Bitcoin™ Issue #22

Wealth Inequality and Bitcoin

Hey friends, welcome back to Think Bitcoin™. As always, if you have any questions or comments, feel free to reach out!

In this issue:

An essay about wealth inequality, what current discussions about it miss, and how Bitcoin addresses it.

As always, if you find this newsletter interesting or useful, please share it with others who might find it interesting or useful, too!

Wealth Inequality and Bitcoin

Last week I was directed to a video “critiquing Bitcoin” by a personal finance Instagram account with thousands of followers. I was, of course, intrigued, as I think it is not merely healthy, but also essential, that we engage with good-faith, substantive criticism. After all, if the technology many of us believe to be transformative does not stand up to rigorous scrutiny, then it’s not all that transformative.

Unfortunately, the video was a morass of mischaracterizations, incomplete data, misleading assertions, and, most frustratingly, ideological objections masquerading as scrupulous criticism (to borrow a Nic Carter formulation):

I want to focus on a specific “criticism” that was raised, and it relates to wealth inequality. The TLDR of the video’s wealth inequality critique is that a bunch of very wealthy people have lots of bitcoin, these wealthy people are white guys who are “rich assholes,” and that, consequently, Bitcoin is just the same as fiat (in the sense that “rich assholes” have the most).

There are those who view this as a devastating (damning, even) assessment of Bitcoin. Proponents of Bitcoin insist that it somehow addresses wealth inequality, but look! There are rich people we don’t like who have a bunch and, therefore, Bitcoin fails to address wealth inequality. So the argument goes.

This argument is flawed for many reasons.

Before we discuss those flaws, however, I think it’s important to have a more nuanced discussion about what we mean when we talk about wealth inequality and the implications of different solutions.

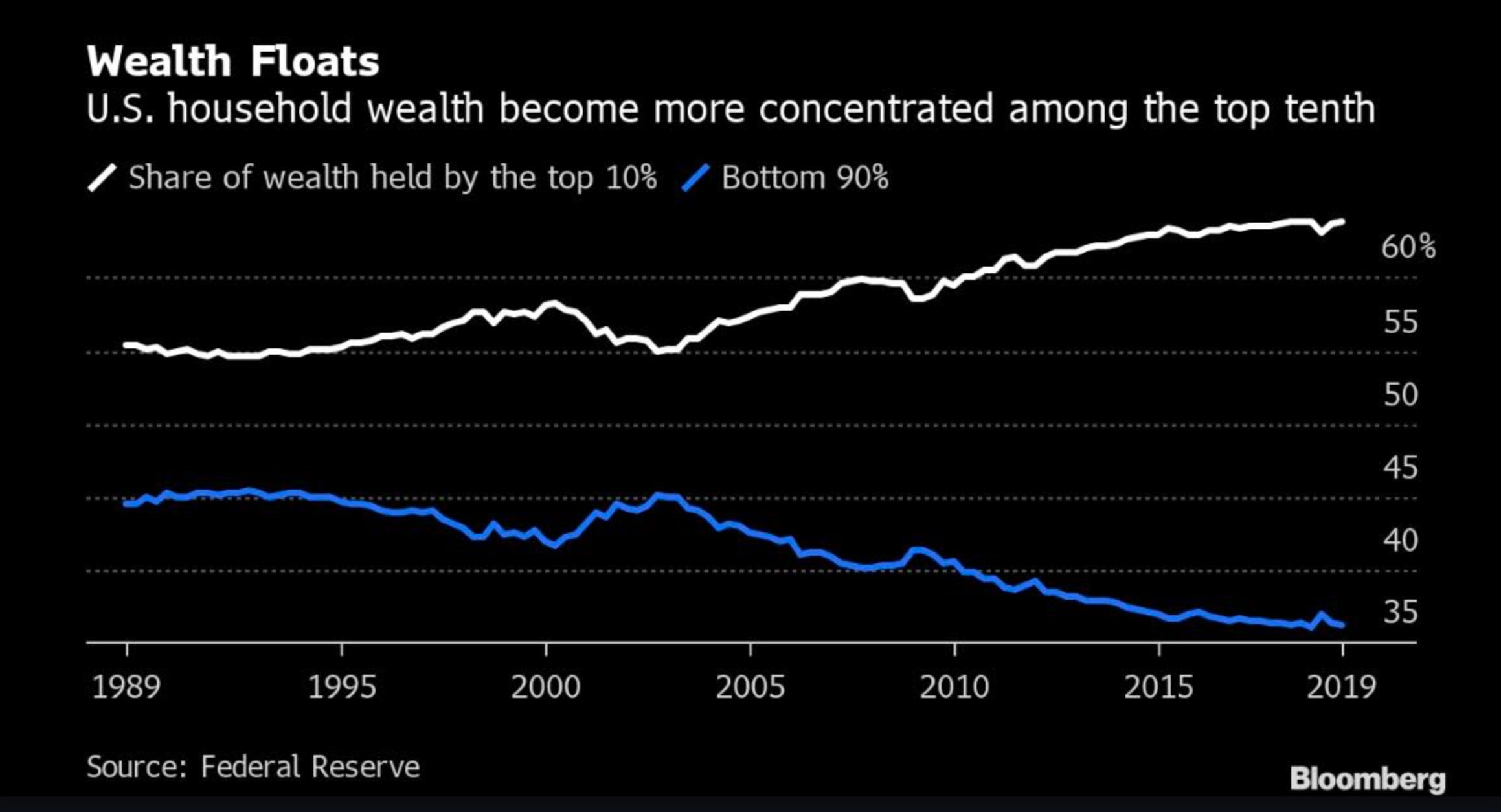

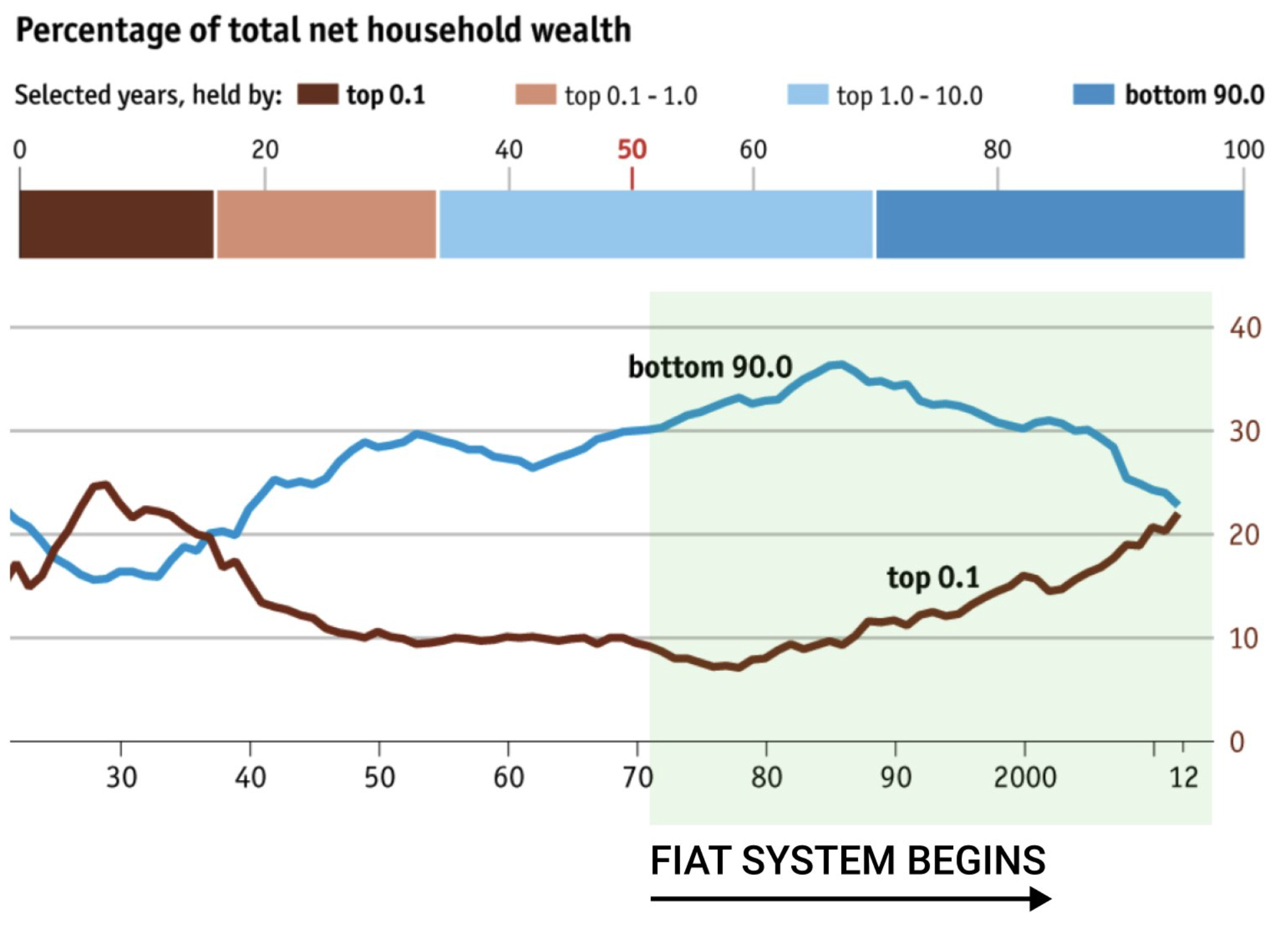

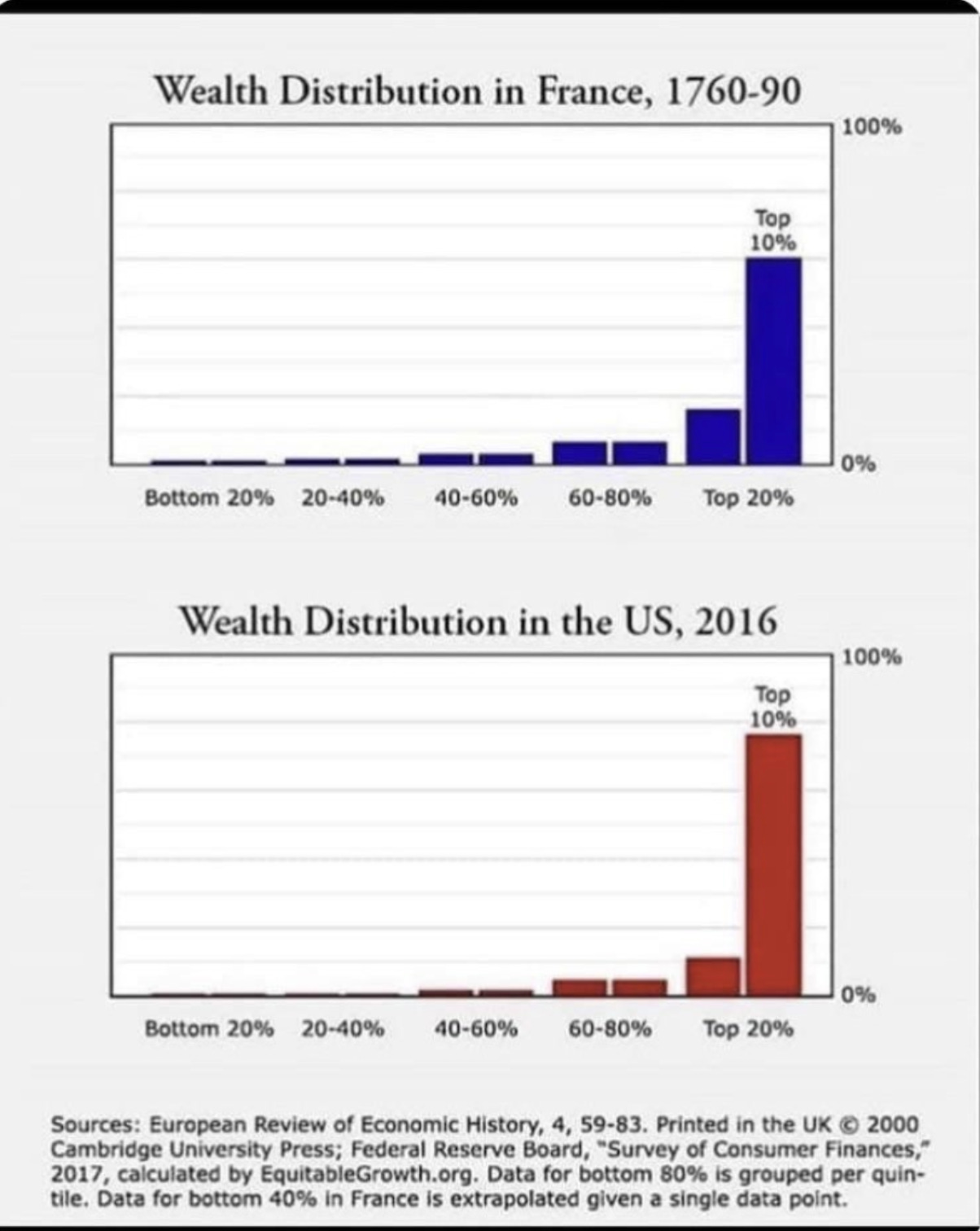

Wealth inequality is obviously a major societal problem. We’ve all seen the plethora of charts out there that show just how truly outrageous the gap is becoming. A profound disparity between the wealth of the few and the wealth of the many is problematic for myriad reasons and is often an ominous harbinger of dark downstream effects. Historically, for example, large wealth gaps have frequently preceded populist revolutions.

The obvious central question is how to address this problem, and I believe a better solution begins with properly locating the cause of the problem.

The political Left would argue, essentially, that much wealth is built and grown on existing capital, as opposed to being earned through labor. Once one accumulates enough capital, one exerts influence over the rules of the monetary network, which means one reaps more benefits from those rules, which leads to more capital, which one invests in various ways to create even more capital, which creates more influence, and around and around we go. The connection of this wealth to labor becomes increasingly attenuated and, most importantly, the more capital you amass the more opportunities to create capital you have. Capital is taxed more favorably than labor, so the goal of any enterprising person is to shift as much of his/her/their income as possible from W-2 (i.e. labor) to capital gains (i.e. capital). This dynamic is especially exacerbated by inflation, which depletes the purchasing power of held cash, disproportionately harming wage-earning savers while disproportionately benefiting asset-holding investors. Therefore, if we want to address wealth inequality, we should redistribute the capital that has been amassed and hoarded, punish over-accumulation, curtail generational transfer, and impede the well-worn path from labor to capital income.

The political Right would argue that the market determines winners and losers, that opportunity is (roughly) evenly distributed (while work-ethic is not), and that the world is ultimately meritocratic. They would argue that no one wants a “hand-out” and that anyone can attain great wealth by simply working hard and exercising some entrepreneurial ingenuity. To the extent we want to address disparities in wealth, we should lower taxes, especially on the wealthy capital-owners, who can then be more empowered to share their wealth with employees, who can then use that increased wealth to acquire assets themselves.

I have of course simplified the arguments of the two sides a bit and am acutely aware of the more granular nuances within each.

But my larger point is that neither effectively addresses the problem. In fact, both may actually exacerbate the problem (and even create new ones). And neither side successfully locates or addresses the cause of the problem. Both attempt to alter the results of the game without addressing the structure of the game itself.

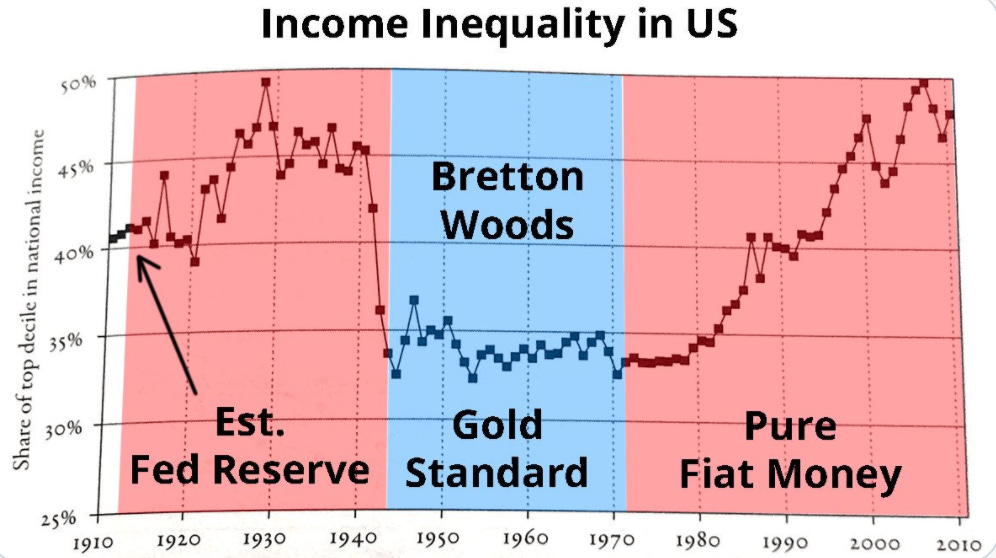

And the structure of the game itself, the game of fiat money, is built on a rotten foundation, namely manipulable, unsound money. When a system is manipulable, people will fight and compete to manipulate it in ways most advantageous to them. A scaffolding of bad incentives, including things like discrimination, exploitation, and other exclusionary practices, is erected atop the rotten foundation. Those with the most money, power, and resources are able to exert the most influence over the network, and it creates a cycle. In the Bitcoin world we often summarize this by saying those closest to the money printer benefit the most, which is to say the Cantillon Effect prevails.

So how is Bitcoin different? When you’re wealthy in the fiat system, you get to wield more influence. You get to build the gates and decide who gets kept out. In the Bitcoin network, wealth plays no part in how much influence you can exert on the monetary rules. The king and the pauper are treated alike by the protocol. The color of your skin, the religion you practice, your gender identity, your credit score, your zip code, etc. - none of this matters in the eyes of the Bitcoin network.

So when critics point out that the Winklevoss twins own a bunch of bitcoin so therefore it’s the same as fiat, they miss the point entirely. In the fiat system, wealth equals power and influence over the monetary network. In Bitcoin, it does not.

If the idea is that wealth inequality is only solved if everyone is given the same amount of wealth, or if we create a system that ensures an equal distribution of wealth, then sure, Bitcoin does not address wealth inequality. But I don’t think that’s what most of us mean when we talk about addressing wealth inequality. Historical attempts to redistribute wealth equally to everyone have been disastrous, deadly, and self-defeating (see, e.g., the Robespierre after the French Revolution, the former USSR, and Castro’s Cuba). Why? Because the monetary network, in each of the aforementioned cases remained manipulable. It was only the identity and party affiliation of the manipulators that changed. Moreover, manipulating to total equality requires a level of centralized power that, first, must be seized, and, once seized, is subsequently never relinquished voluntarily.

But a monetary network whose rules can’t be manipulated by anyone, wealthy or not, a network that is equally accessible to all and requires no permission to join, creates a much more equitable distribution of opportunity, which is what I think most of us mean when talk about addressing wealth inequality. Bitcoin disentangles the state, which responds to wealth and power, and the monetary network.

Of course, there are a number of advantages that certain folks have when it comes to Bitcoin. Those with lots of fiat capital are able to buy more bitcoin. This means the wealthy, should they all decide to opt-in to Bitcoin, could buy and hold significant amounts of it (remember, though, there are only 21 million). This seems to unfairly reflect the disparities of the fiat system. However, Bitcoin adoption is still in its extremely early stages, meaning a first-mover advantage can still be secured by early adopters. This is why it is absolutely imperative, as Nicole Dobrow has written, to spread Bitcoin knowledge and exposure to people and communities who have been historically left out or malevolently boxed out of the current fiat system. But there are no accredited investor rules, no investment minimums, and no credit-checks required to opt-in to Bitcoin. It is the best-performing asset of the last 12 years and there are no gatekeepers.

Content Round-Up

“Bitcoin’s Connection to Religion, Metaphors, Belief Systems, and Being a Force For Good,” an episode of the Digital Money Advisor podcast with Dr. Mark Stephany. This was the best piece of content I consumed this week. It’s just a really thought-provoking, wide-ranging conversation that I think effectively illustrates the intellectual depth and diversity in the Bitcoin community. A lot of newer folks who come into the Bitcoin world want to talk about price. The longer you stay, the deeper you go and the more you realize that Bitcoin isn’t about price. It’s about changing the world. Which is also why I love being in this space. That’s where Mark is focused, and that’s why this episode is so good.

As always, thanks for reading! If you enjoyed it or found it useful, share this newsletter widely and freely!

“Civilization is in a race between education and catastrophe. Let us learn the truth and spread it as far and wide as our circumstances allow. For the truth is the greatest weapon we have.” -H.G. Wells

See you next week,

Logan

SUPPORT

Send bitcoin to my Strike

SOCIAL

DISCLAIMER: I am not investment advisor and this is not investment advice. This is not, nor is it intended to be, a recommendation to buy or sell any security or digital asset. Nothing in this newsletter should be interpreted as a solicitation, a recommendation, or advice to buy or sell any security or digital asset. Nothing in this newsletter should be considered legal advice of any kind. This newsletter exists for educational and informational purposes only. Do your own research before making any investment decisions.

© Copyright The Why of FI.