Think Bitcoin™ Issue #2

Bitcoin fixes savings; regulatory battles; removing trust from the system

Friends, welcome to the second issue of Think Bitcoin™! As always, for those who are brand new or relatively new to Bitcoin and looking for some education on the basics, feel free to scroll down to the “For the new and new-ish” section and work your way up.

Content Round-Up:

1. “Bitcoin is the Great Definancialization,” an article by Parker Lewis. This is an older classic (from December of 2020), but it’s one of the top five pieces of content I would give to anybody in the personal finance or FI/RE communities who is encountering Bitcoin for the first time.

It is unquestioned dogma in the personal finance and FI/RE communities (and elsewhere, too) that one must make his or her money “grow,” and do so perpetually, in order to outpace inflation and the continuous loss of purchasing power it inflicts upon ordinary savings. That we should receive paychecks and promptly invest them in the stock market, to the greatest extent possible, is personal finance orthodoxy. An actual examination of the system that engenders this orthodoxy is rarely undertaken. In a lot of ways I think the personal finance community is so (understandably) fixated on surviving the game in which we find ourselves that it fails to question the game itself.

In this article, Parker Lewis dives deeply into why, exactly, we all feel like we need to make our money “grow” and how Bitcoin fixes the broken monetary policy that makes us feel this way.

2. Jeff Booth episode on the Blue Collar Bitcoin Podcast. Booth, author of The Price of Tomorrow: Why Deflation is the Key to an Abundant Future, walks through the macroeconomic case for Bitcoin. In my opinion, nobody does this better or more effectively than he consistently does.

3. “Bitcoin’s Energy Usage Isn’t a Problem. Here’s Why.” This is a characteristically thorough, meticulously outlined article by Lyn Alden. A common critical narrative of Bitcoin is that it uses an unsustainable amount of energy. This narrative is based on a plethora of misunderstandings about how Bitcoin actually functions and is usually promulgated by those who have not done much meaningful work to understand how Bitcoin uses energy. Alden breaks it all down here.

4. “The Lightning Network is Going to Change How You Think About Bitcoin,” an article by Jeff Wilser. One of the common criticisms of bitcoin, and one you’ve probably heard or harbored yourself, is that bitcoin just can’t be used to buy a cup of coffee and is therefore no more than a digital piece of gold you hold and never use. The implication of such a criticism is that bitcoin could never be a global currency. The crux of the criticism is about scalability. The argument is that Bitcoin cannot accommodate the amount of transactions that, for example, Visa can accommodate. And this is true. BUT, the Lightning Network, a layer-2 technology (layer-2 meaning built on top of layer-1, the Bitcoin chain), is addressing precisely this issue and has been making exciting progress.

5. “Why Progressives Should Love Bitcoin: An Open Letter to Senator Elizabeth Warren,” an article by Samantha Messing. Too often Bitcoin is lazily characterized as a strictly or transparently right- or libertarian-leaning technology, politically speaking. Personally, I tend to think Bitcoin transcends the two-party system of politics in the U.S. I do think it has far-reaching political implications. I just don’t think the current two-party framework in the U.S. is equipped to parse it along party lines. More importantly, I think Bitcoin reveals the systemic limitations of our current political machinery and offers a powerful alternative vision.

With respect to claims that it is intrinsically right-leaning, it is true that Bitcoin removes power from the state, which leads some to categorize it as right of center. It also promotes free, unmanipulated markets, which some associate with business-friendly Republican principles. But Bitcoin is also a technology incapable of discrimination and openly accessible to all. It is unable to be controlled by any one party, and its monetary policy isn’t rigged by an unelected few in Washington D.C. There are no gatekeepers in Bitcoin. It can bank the unbanked. In many ways, it accomplishes the putative goals of progressives better and more effectively than government intervention. To modify Senator Warren’s own presidential campaign slogan, Bitcoin is big structural change. And this is not talked about frequently enough, in my opinion. This is why I’m highlighting this particular article, which concludes with this quote:

“Bitcoin offers equal access which will inevitably foster more equal outcomes. Bitcoin will make the world a better place. What’s more progressive than that?”

(Bonus) 6. Petrodollars – This is a 33-minute documentary film, made by Richard James and narrated by prominent Bitcoin thinkers Nic Carter and Alex Gladstein, with additional narration by Guy Swann. The film is about the petrodollar system, which is something that almost never gets talked about in the personal finance and FI/RE spaces. The petrodollar system is essentially a set of agreements between the United States and Saudi Arabia (as well as other oil-producing countries in the Middle East) in which the Saudis agreed to price oil transactions in dollars and buy U.S. debt with those dollars. In exchange, we promised to protect them and sell them arms. They get rich and stay protected, and the U.S. dollar remains the global reserve currency. This has been a central organizing force of the global economy since the 1970s, when Nixon ended the gold conversion window.

But at what cost? This is the question posed by the film. The petrodollar system has been catastrophic for the working, manufacturing class in America, catastrophic for the environment (it’s based on oil, obviously), and catastrophic for third-world economies. It has also played a part in multiple wars and military interventions.

This short film is also great for folks looking to get some background on economic history, particularly how the United States moved from the gold standard to the Bretton Woods agreement, and then from Nixon’s abrupt end of dollar-to-gold conversion to the petrodollar system, which is unwinding today.

The film looks ahead to what might replace the petrodollar as the organizing force of the global economy.

I highly recommend reading the source material for the film, which is an article by Alex Gladstein called “The Hidden Costs of the Petrodollar.”

Headlines/News:

Updates on the infrastructure bill

Last week we followed the infrastructure bill in the United States Senate which, as originally written, included a last-minute provision seeking to change the definition of “broker” in the tax code to encompass just about every actor in the crypto space, including those who perform no broker-like activities (like miners, software developers, stakers, node operators, etc.). Pursuant to the language of the provision, these parties would be treated as brokers and be subject to the tax reporting requirements of brokers. For most of theses parties, it is logistically impossible to comply with these requirements. Since it would render much activity illegal, the ultimate effect of enforcing such a provision would seem to be the eventual offshoring of the crypto industry and, with it, jobs, innovation, potential tax revenue, and economic growth.

The crypto community responded with vigor and got some small changes into the final text of the bill. Then a bipartisan group of lawmakers went back and forth on different amendments to this language, each excluding different parties from the proposed new definition of “broker.” Because of some intricacies of Senate procedure, these amendments did not actually get presented for votes on the floor. Instead, a bipartisan group of Senators agreed to an amendment, which was also supported by the Treasury Department, and presented it to their colleagues for unanimous consent. Unanimous consent just means asking that something be accepted unanimously. If one person objects, the unanimous consent fails.

Senator Toomey gave a speech on the floor about the proposed amendment, highlighting the importance of regulating the crypto industry in a smart, nuanced way that does not stifle innovation or subject parties to rules with which they cannot possibly comply. He said the original provision, with its overbroad definition of “broker,” was akin to regulating a firm performing broker services in stocks and bonds by requiring both the firm itself and the electric company providing electricity to the firm’s building to report on transactions. This would obviously be ridiculous, he noted, as the electric company does not perform any broker-like activities.

He presented the amendment to the floor for unanimous consent. Senator Shelby, an 87-year-old from Alabama, asked that a vote on his own unrelated amendment about increasing funding for defense be considered, as well. Senator Toomey allowed it, which prompted Senator Sanders to object. This killed the unanimous consent motion.

What happened next was fascinating to watch. Senator Cruz stood up and presented a new amendment for unanimous consent. His amendment consisted of striking the entire crypto provision from the infrastructure bill. His reasoning, which he expounded upon in a floor speech, was that almost no one in the Senate actually understands anything about cryptocurrency. And, as such, why would the Senate hastily regulate something that they don’t understand and risk doing unnecessary harm to a nascent industry? Why not have some hearings, do some research, and learn from folks in the space? Here’s part of his speech:

“[the current bill] would force every single participant in the cryptocurrency structure to operate as a financial institution, which would mean they would have to provide consumer information to the IRS, even if they don’t have access to that information. This overly broad definition of the word ‘broker’ will block rapid innovation in cryptocurrencies, and it will endanger the privacy of many Americans in cryptocurrencies. This is wrong.

So I applaud my colleagues for trying to find an incremental approach. Unfortunately, because the senator from Vermont objected, that incremental approach hasn’t been adopted. So let’s exercise a brief, shining moment of common sense. And let’s recognize if we gathered all 100 senators in this chamber and asked them to stand up and articulate two sentences defining what in the hell a cryptocurrency is that you would not get greater than five who could answer that question.

Given that reality, the barest exercise of prudence would say we shouldn’t regulate something we don’t yet understand. We should actually take the time to try to understand it. We should hold some hearings, we should consider the consequences. We shouldn’t destroy people’s lives and livelihoods out of complete ignorance.”

Senator Cruz then offered his amendment for unanimous consent. Senator Shelby from Alabama stood up again and asked that his unrelated amendment to increase defense spending be considered, as well. Senator Cruz told Senator Shelby that though he agreed with increasing defense spending, adding this to the amendment he was proposing would result in an objection from Democrats. So Senator Cruz did not modify his amendment to appease Senator Shelby. Senator Shelby then objected, tanking Senator Cruz’s amendment.

Senator Shelby, acknowledging that he blocked something he, in fact, agreed with, tweeted this immediately afterwards:

The result of all this is that the original language in the infrastructure bill regarding cryptocurrencies will stand. The bill now heads to the House of Representatives, where this provision will be debated some more. The Blockchain Caucus in the House, which is chaired by two Democrats and two Republicans, has already circulated a letter outlining the ramifications of the current language and its desire to fix it.

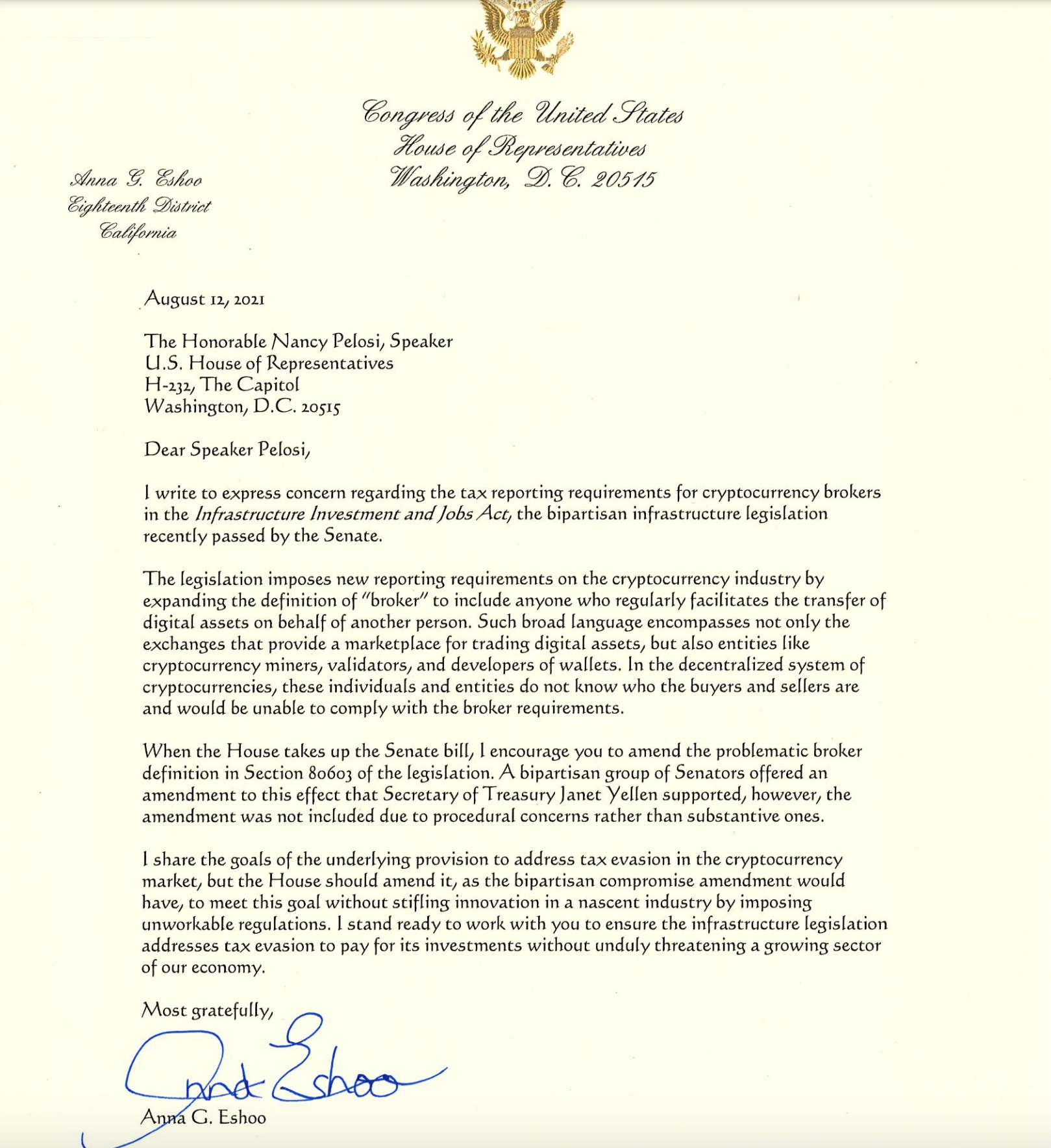

Representative Anna Eshoo, a Democrat from California, penned her own letter to Speaker Pelosi:

Representatives Ro Khanna and Eric Swalwell have also expressed concerns over the existing language. Representative Soto has suggested that even if the House fails to amend the language passed by the Senate, standalone legislation would be a contingency option to fix it.

On Friday afternoon, a Bloomberg report citing an unnamed Treasury Department official, reported that the Department would not go after actors in the crypto space who are not clearly “brokers.” Apparently, the Department is set to issue some guidance to this end next week. Per the Bloomberg report, they are planning to exempt parties they don’t consider to be brokers on a case-by-case, basis. This is obviously not optimal for a couple of reasons. For starters it requires us to trust the Treasury Department’s word, which is difficult to do given how antagonistic they’ve historically been to crypto, both explicitly and behind the scenes. The “case-by-case” basis is also troubling and not nearly as clear and broad an exemption for non-broker actors as the one sought by the crypto community and its Congressional allies in the infrastructure bill.

The larger takeaways of this battle are as follows:

1. Very few people in Congress, especially in the Senate, understand, even at an elementary level, what cryptocurrency is. Nevertheless, Congress has demonstrated a willingness to regulate without knowledge. Thus, if the crypto community wants to avoid overbroad, draconian regulation, we need to launch and sustain an extensive education campaign in the halls of power. This is already underway, and I believe this past week’s proceedings have accelerated the process. But it must continue. Special shoutout to both Coin Center and the Blockchain Association, who have been instrumental in the process thus far. Please check them out.

2. The crypto lobby has arrived and is a force to be reckoned with. There are an estimated 10-50 million crypto users in the U.S. alone, a number that is growing rapidly. One study has estimated that 46 million Americans own bitcoin. Globally, there are over 220 million crypto users, and this number doubled in the last four months alone. The crypto community in the U.S. made well over 50,000 calls to senators about the language in the infrastructure bill. This is a growing political constituency, and one to which folks from various (and even wholly divergent) political backgrounds are migrating. This is powerful and un-ignorable.

3. There seems to be a collective acknowledgment and realization that crypto is not going away. In his floor speech, Senator Cruz forcefully noted that the crypto industry is not tied to American soil, meaning it is not tied to any particular country or jurisdiction. It can move and will move if it needs to do so. This acknowledgment carries an implication that everyone in the Bitcoin space already understands: one country can’t shut it down. Highlighting this reality is the fact that China recently banned Bitcoin mining, and the mining just moved elsewhere. The network continued to function uninterrupted. The wider and more thoroughly this is understood, the more I expect governments to think strategically about positioning for Bitcoin adoption, as opposed to scrambling to curtail it.

Gensler tells Elizabeth Warren the SEC needs “plenary” power to regulate crypto

In other regulatory news, SEC Chair Gary Gensler responded to an open letter penned by Senator Elizabeth Warren last month. In her letter, Senator Warren asked Gensler about the authority the SEC has over crypto and inquired whether Congress should act in some way to assist. She released Gensler’s response this week, which was notable for a couple of reasons.

First, he said: “I believe we have a crypto market now where many tokens may be unregistered securities, without required disclosures or market oversight…To the extent that there are securities on these trading platforms, under our laws they have to register with the Commission unless they meet an exemption. If a lending platform is offering securities, it also falls into SEC jurisdiction.”

This isn’t surprising. Gensler made it clear in his speech last week at the Aspen Security Forum that he has his sights on DeFi and believes many cryptocurrencies are, in fact, unregistered securities. For the background on the legal definition of a security and why it’s important in this context, see last week’s newsletter. This is another clear, explicit statement from Gensler that he’s eying the non-bitcoin cryptos. Like I said last week, he’s certainly not the only voice in the SEC, but he is the most important voice. It’s also worth noting again that the CFTC thinks crypto is their turf – not the SEC’s.

Second, and more notably, Gensler asked Congress for additional authority to regulate crypto. Troublingly, he said “regulators would benefit from additional plenary authority to write rules for and attach guardrails to crypto trading and lending.” This word “plenary” is a bit worrisome. Per Wex, the legal dictionary hosted by Cornell Law School, “plenary” power is “power that is wide-ranging, broadly construed, and often limitless for all practical purposes.” For example, Congress exercises plenary power over a few different areas. However, members of Congress are elected and (in theory) accountable to voters. Gensler is not elected and not accountable to voters. So the idea that Gensler and the SEC would be, for all intents and purposes, legislating crypto, is not optimal. Congress is not allowed to delegate its legislative power to an executive agency like the SEC, but they can and do give agencies the power to make rules, provided they give the agency an “intelligible principle” upon which to base those rules. This delegation of regulatory power is almost never struck down.

The point is that, in this author’s opinion, optimal regulation of the crypto space involves robust education, a learning process for lawmakers, productive conversations with stakeholders, and meaningful interfacing with advocacy groups and industry groups. Doing none of these things and, instead, handing all the authority over to the SEC, no commissioner of which is democratically elected, is not a good outcome. So look for some pushback from the crypto space and its allies in Congress if Gensler’s request gains any traction.

Gensler and Warren are both, ostensibly, fixated on what they conceive of as “investor protection.” Gensler has been clear that this is the primary mandate of the SEC. And yes, there is no shortage of scams and shady behavior in the crypto space. Yes, some people lose money. But it’s worth pointing out, if at least for the sake of argument, that investors have been “protected” out of most of the best-performing assets of the past 20 years. Private companies stay private longer, enriching their early investors, all of whom meet the requirements to invest in these promising companies, requirements which essentially boil down to being rich. And then when these companies go public, these already-rich investors make massive gains. Think of some of the biggest companies now: Facebook, Uber, Coinbase, Netflix, etc. Normal retail investors were shut out of any opportunity to invest in these companies early, putatively on the grounds that they’re not sophisticated enough to take such risks with their money. So the majority of the gains from investing in these companies are locked in by wealthy early investors before the companies go public.

Why is this worth bringing up? Well, because we do a lot of things in the name of “investor protection” that sometimes just serve to shut retail investors out of the most promising investments. Meanwhile, most normal folks keep whatever savings they can muster in U.S. dollars, which themselves are losing purchasing power at an alarming rate, largely as a result of inflating the money supply which, again, is something sold as necessary to hold the economy together and protect normal people. Any attempt to “protect” investors out of being able to invest in Bitcoin, the best-performing asset of the last decade, would seem similarly to harm the very people it would purport to “protect.” The chart below from casebitcoin.com, which is accurate as of Saturday, August 14, is worth thinking about.

This is not to argue against regulation of any kind, nor is it to suggest that there are no counterarguments to what I’ve just articulated. It’s just to say we should take a step back and really think about how we regulate this new and growing space to make sure we do it in a way that is nuanced, intelligent, and fair.

Lastly (and I just can’t help myself here), let’s also note that Gary Gensler is worth well over $100 million. He spent 18 years working at Goldman Sachs before accepting multiple political appointments, including Chair of the CFTC under Obama. He then spent some time in academia before being nominated by Biden to chair the SEC. So this is a career “insider,” shall we say. This is not, on-its-face, a bad thing. But, fundamentally, I would argue the raison d’etre of Bitcoin (and crypto, generally) is the total disruption of the system crafted, protected, and perpetuated by such insiders, all of whom benefit disproportionately and immensely from this system.

Coinbase Earnings

Coinbase reported its second quarter earnings last Tuesday, and they were, to put it mildly, impressive. They reported $2.23 billion in revenue, obliterating expectations. Their net profit for the quarter was $1.6 billion.

For the new and new-ish:

Last week we began with a little bit of Bitcoin history. We talked about Satoshi Nakamoto, the Bitcoin whitepaper, and what Satoshi was thinking about at the time of invention. We then explored Bitcoin’s fundamental idea, which is removing centralized, trusted financial intermediaries. If you’re new and you missed Issue #1, take a couple of minutes and skim through the “for the new and new-ish” section in that issue to get up to speed.

Now we’re going to talk about trust. How is it possible to have a system for transactions that does not have a trusted centralized intermediary making sure nothing goes wrong? In other words, sure, decentralization sounds great, and we can all probably agree that banks have done (and still do) a lot of shady, rent-seeking stuff, but isn’t centralization still the best option? Otherwise, how could we trust that ledgers aren’t being manipulated, that fraud isn’t constantly being orchestrated, or that bad actors aren’t taking advantage? A centralized financial intermediary seems to appropriately assuage these concerns.

These concerns all come down to trust. Our financial system is based on trust, from the very top to the very bottom.

We trust centralized intermediaries to manage ledgers, among other things. And they do do this. Before we dive into how Bitcoin obviates trust altogether, let’s talk about some specific ledger-related problems that centralized intermediaries prevent, because if we’re going to get rid of them, we’re going to have to solve these problems in some other way.

The first one is pretty classic. It’s called the double-spend problem. Imagine I deposit $100 into my bank. I then want to pay you that $100 for something. I send you that $100 using some type of electronic payment method. My bank registers this transaction in my ledger, subtracting $100 from my account. Your bank also registers this transaction in your ledger and adds $100 to your account. Now, imagine I try to pay someone else that same $100 I just paid you. What prevents me from being able to do this? My bank, which has been keeping the ledger, says no, that’s $100 you don’t have. In other words, it prevents me from spending the same $100 more than once. This is the double-spend problem, which we trust banks to solve as part of their management of ledgers.

The next one is the problem of mistaken identity. Every electronic payment app (and the online bank account to which they are linked) requires an identity verification step of some kind. Typically you log in with a username and a password to verify that it is, in fact, you who wants to make a transaction. If a malicious third party obtains your username and password, that’s a breach, and now this third party is able to access your accounts. In this situation, we contact the centralized intermediary, provide extensive additional proof of identity, and ask that it delete any unauthorized transactions from our ledger. If we remove the trusted intermediary we have to find a different way to solve this problem of identity.

So, quick recap: We know the whole system is based on trust. We trust centralized intermediaries like banks, and they keep the ledgers. You and I don’t walk around with our own ledgers, manually tallying every transaction we make. This wouldn’t work on a large scale, anyway. So we delegate this to banks, and this delegation has allowed significant scaling of transaction power. Banks seem to adequately solve the double-spend problem and, most of the time, the identity problem, too. However, this massive amount of trust we have in these centralized intermediaries has significant drawbacks, some of which we have discussed (and some of which we will eventually discuss).

So we decide to remove these centralized intermediaries, these middlemen, and start something new.

The first thing we do when we remove the middlemen is decentralize the ledgers. We have no banks holding and managing them now. We instead decentralize possession of the ledger by giving everyone a copy. Now you, me, and our friends each have a copy of the big ledger of transactions between us. Our group has become a network. We talk to each other, consult with each other, and keep each other up-to-date on all the transactions going on between us. Any time one of us wants to transact, we let the whole group (the whole network) know, so that everyone can update his or her copy of the ledger accordingly. If I want to send $5 to you, I tell our group that I want to do so and everyone makes this entry in their respective copies of the ledger.

If you hear folks talking about “distributed ledgers” or “distributed ledger technology,” this is what they’re talking about. They’re referring to a ledger being shared among members of a network, as opposed to being held by one centralized party.

Okay, so we’ve successfully decentralized power and distributed the ledger amongst our network. But remember the double-spend problem? We still have to solve that problem, and we no longer have a bank to do it for us. What we have now is a network of users, each with a copy of the ledger, each updating the ledger accordingly when a transaction occurs. So how do we make sure no member of the network double-spends?

We use consensus. In other words, the members of the network have to agree that each transaction is valid and doesn’t include a double-spend. For example, if I want to send you $100, I announce to the network that I want to send you $100. Everyone in the network checks his or her copy of the ledger to make sure I have the $100 I want to send to you. If I do, each member of the network validates the transaction and adds it to his or her copy of the shared ledger. So far so good. If I try to spend $100 I don’t have, the network rejects the transaction. This is how double-spends gets policed.

But consensus can get muddied in a variety of ways. It seems like it works great if the network consists solely of friends we can trust, friends we know won’t try to cheat. How might one cheat this consensus mechanism? Well, imagine there are five of us in the network. Imagine you, me, and another friend decide that I’m going to send $100 to you, but we agree not to record this transactions in our copies of the ledger. Now three of the five ledgers in the network say that I continue to have $100, even though I just sent it to you. The majority of the ledgers say I didn’t spend it. This is a problem. Now imagine that a new friend joins the network and asks for a copy of the ledger. He’s going to get three that did not record the transaction of $100 from me to you and two that did. Which one will he accept as correct? In this way, by teaming up with a majority of the people in the network, I was able to create $100 for myself that I didn’t have. This is referred to as a “double-spend attack.”

So it seems like this distributed ledger idea only works if every member of the network trusts each other not to perform an attack like this. This also implies that the network requires permission to join, because the only way we know if we can trust other folks in the network is if we control who joins and only allow people we trust in as new members. In light of these limitations, our effort to remove the middlemen seems to have stalled. It seems like we’ve just replaced centralized trust and permission with decentralized trust and permission, which almost feels messier. And how could we possibly scale a transaction network across the world if we have to trust every member who joins and grant him/her permission to join?

The solution to these problems is one of Bitcoin’s most elegant features. It’s called Proof of Work. You’ve probably heard this phrase somewhere if you’ve spent any time dabbling in the Bitcoin world. You may even have heard of an alternative consensus mechanism called Proof of Stake.

Proof of Work is absolutely essential to Bitcoin, but it is admittedly difficult to understand. It involves a little computer science, some cryptography, and some math, which, if you’re anything like me, are intimidating subjects. So we’re going to begin walking through Proof of Work next week, and we’re going to do it very slowly and methodically. The weekly segments might even be a little shorter just so that they’re more easily and conveniently reviewable.

Bonus/Miscellaneous:

My favorite tweet of the week (and how I feel about the personal finance and FI/RE communities):

Thanks for reading, this week! As always, I know we covered a lot, but hopefully you found it useful. Obviously this newsletter takes me quite a bit of time to research and write. I’d love and appreciate it if you could share it with anyone you think might be interested. Maybe you have friends who are crypto-curious, maybe you have family members who ask you about Bitcoin, maybe you have coworkers who are into FI/RE. The goal of this newsletter is to spread knowledge, education, and interest in Bitcoin to as many people as possible. So please share this freely and widely!

Let’s never stop learning.

See you next week,

Logan

DISCLAIMER: I am not investment advisor and this is not investment advice. This is not, nor is it intended to be, a recommendation to buy or sell any security or digital asset. This newsletter exists for educational and informational purposes. Do your own research before making any investment decisions.

Copyright The Why of FI.