Think Bitcoin™ Issue #14

Why inflation won't go away; a monetary escape hatch for the U.S.; building generational wealth with bitcoin; Bitcoin as a cathedral

Hey friends, welcome back to Think Bitcoin™. As always, if you have any questions or comments, feel free to reach out!

In this issue:

Headlines/Insights: Inflation is very much here, but its primary cause is not the supply chain; the Fed’s options for handling it; the implications of those options; how Bitcoin fits in; how the U.S. could attempt to avoid the harsh consequences of its current monetary trajectory

Content Round-Up: 3 articles, 1 podcast, 1 Twitter thread (and a bonus documentary)

As always, if you find this newsletter interesting or useful, please share it with others who might find it interesting or useful, too!

Headlines and Insights

Inflation and the Escape Hatch

Last week the consumer price index numbers came in for October at 6.2% year-over-year, which is the largest print in 30 years. The numbers exceeded consensus estimates and came on the heels of September’s hot 5.4% year-over-year increase.

So what does all this mean, especially for Bitcoin? How should we be thinking about it, where does the Fed go from here, and is there any escape hatch available?

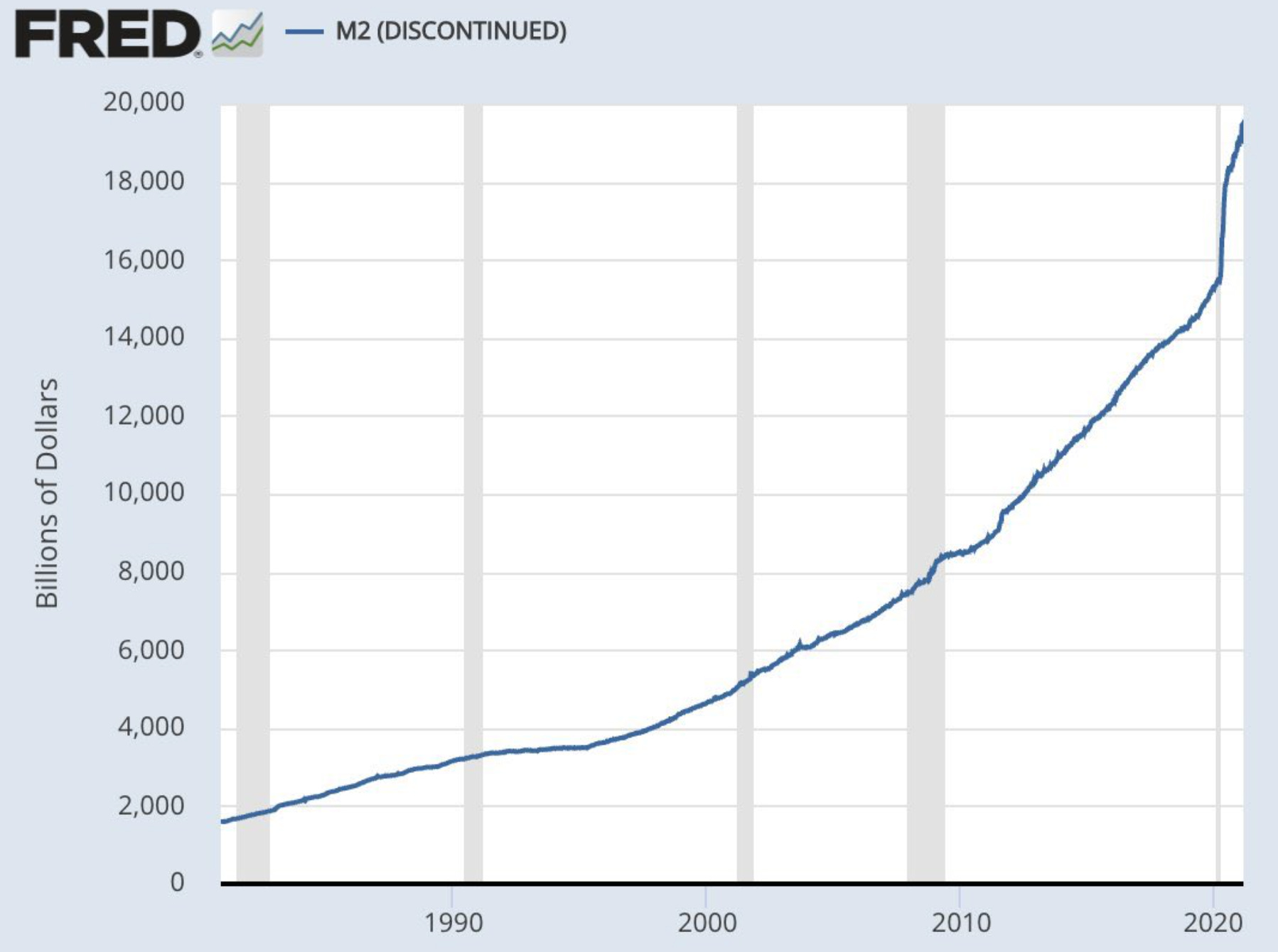

With respect to causality, we hear a lot about difficulties and bottlenecks in the supply chain. Certainly, there are a lot of contributing factors resulting in inflation of this magnitude showing up in consumer prices. However, anyone telling you inflation is strictly a supply chain issue is wrong. Bitcoiners continue to be unsurprised by these inflation prints because they are the predictable result of expanding the money supply as dramatically as we’ve done over the past 18 months (visible in this chart of M2 money supply):

As Milton Friedman said, “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.”

And as the Austrian economist Ludwig von Mises said, “The most important thing to remember is that inflation is not an act of God, that inflation is not a catastrophe of the elements or a disease that comes like the plague. Inflation is a policy.” The policy of the U.S. since 1971, but especially in the last decade or so, has been to expand the money supply, which has debased the currency and, now, is finally showing up in consumer prices.

Though supply chains don’t help, this is not an issue of supply chains. Other countries who did not expand their respective money supplies to the extent that we did are not seeing the CPI upticks we’re seeing:

That being said, it’s also not true that inflation is only present when it manifests in rising prices of consumer goods. Too often we think of inflation as a phenomenon that exclusively affects our grocery bills, the price of gas, and other consumable goods. But these price increases are the results of inflation, which is to say the expansion of the money supply.

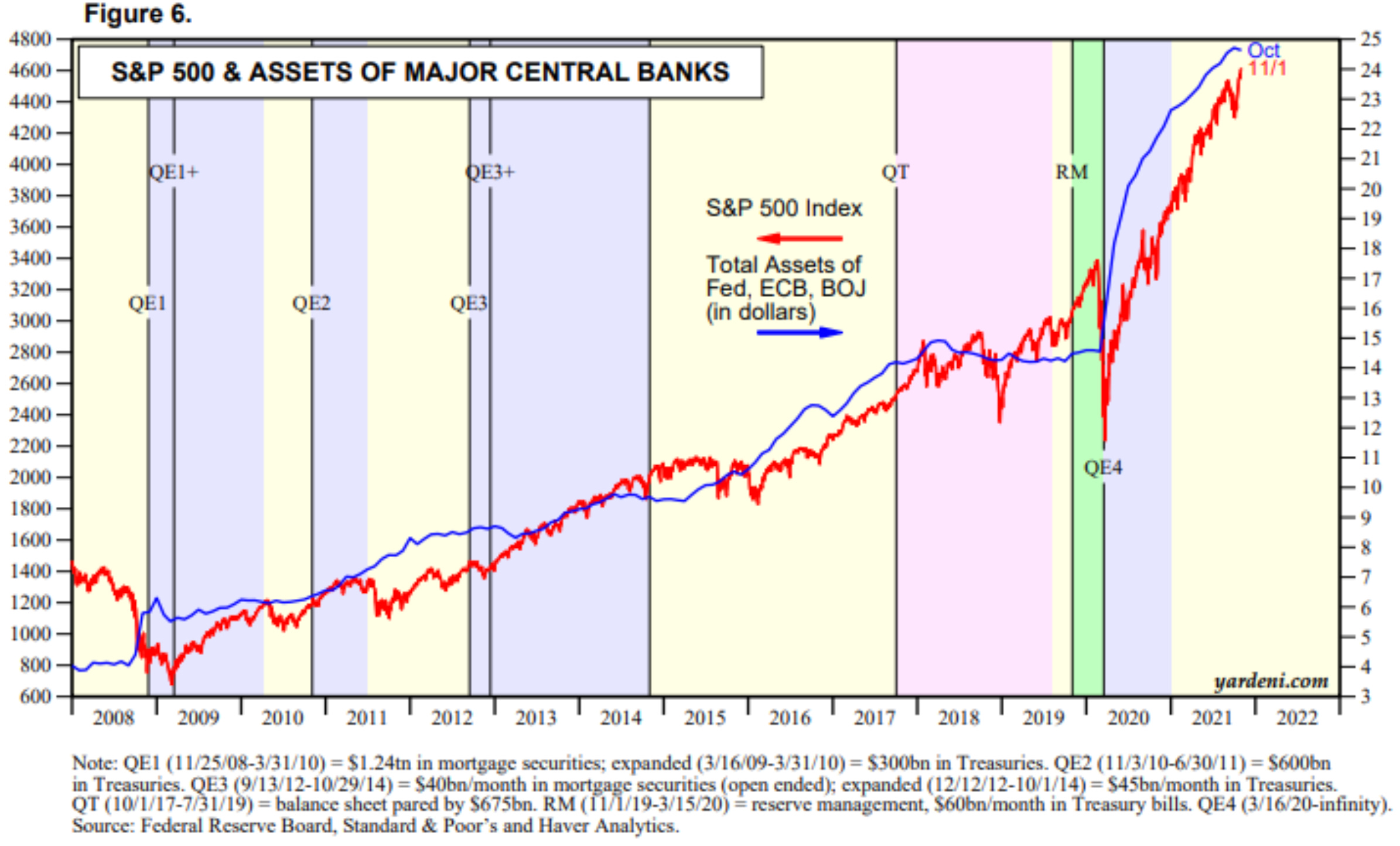

Prior to these increasingly alarming CPI prints, inflation was visible in the price of assets (and still is). We expanded the money supply at an unprecedented rate and have continued to keep interest rates artificially low. Because of the Cantillon Effect, the new flood of liquidity went first to financial institutions, corporations, and the wealthy who, collectively, own the overwhelming majority of the assets in this country. And they kept buying them. The glut of liquidity, therefore, ultimately ends up in assets, which inflates their respective prices. This is why the stock market has been moving in lock step with central bank balance sheets, the expansion of which is the result of quantitative easing.

Now we’re seeing the inflation show up in a big way in the price of consumer goods, which especially harms the middle and lower classes, savers, and those who are more dependent on cash wages and have fewer assets.

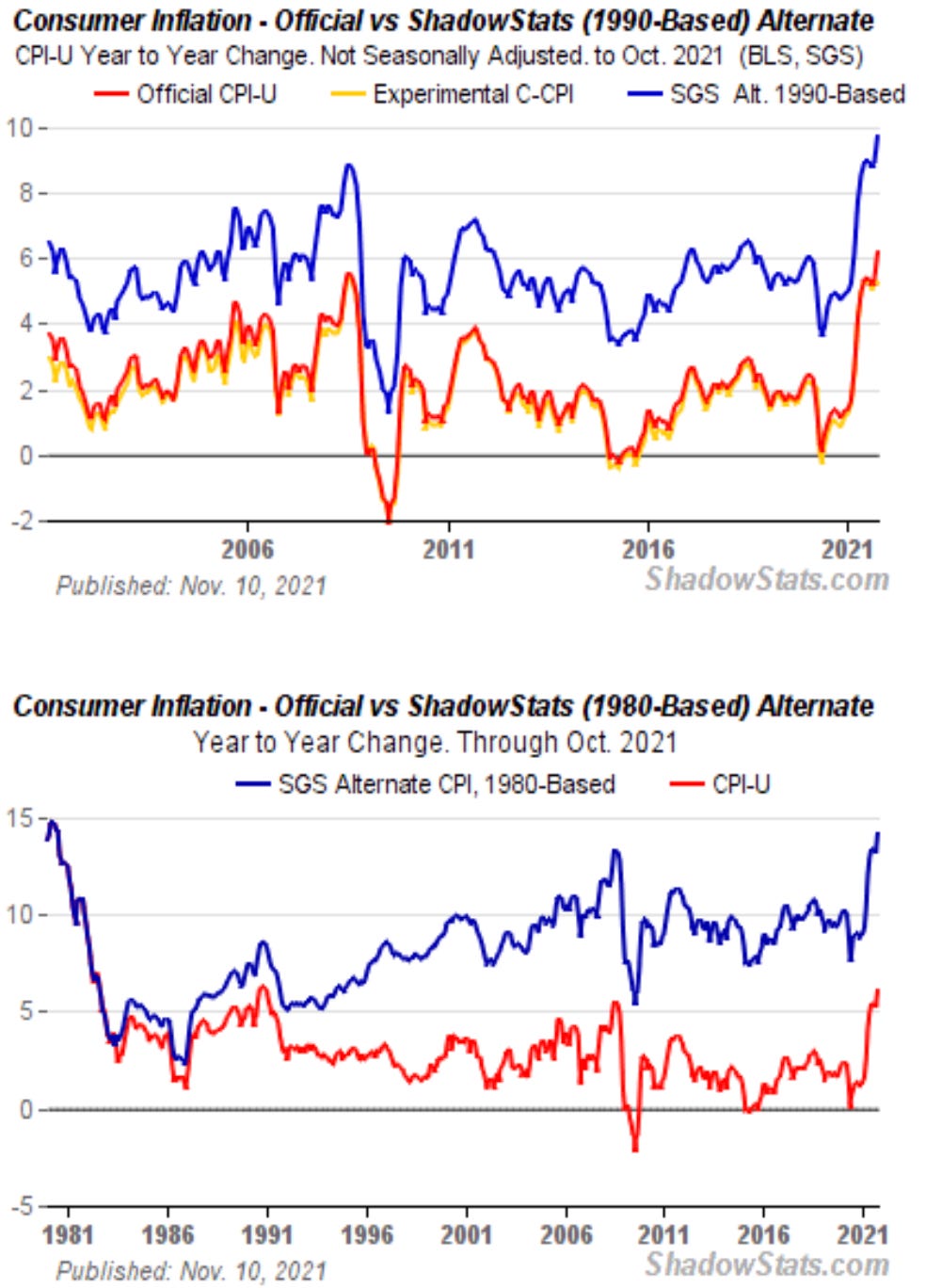

There’s an argument to be made that CPI is even worse than what the numbers currently show. Many forget that CPI, as a metric, has been altered on numerous occasions and involves hotly debated modifiers like hedonic adjustments. It seeks to track the price changes in a specific basket of goods, weighted a specific way, and controversially adjusted for the quality of those goods. ShadowStats.com tracks CPI under the pre-1990 formulation of the metric and the pre-1980 formulation of the metric, as well.

(Chart courtesy of ShadowStats.com.)

We often use the 1970s as our framework for thinking about inflation. You can see from the chart above that, measured with the formulation of CPI that was used in the late 1970s and early 1980s, CPI is currently about 14%.

The question is how does the Fed respond? And what would the consequences be? Where and how does Bitcoin fit in?

In the near-term, the Fed only has a couple of options. The first option is ultimately raising rates. This is, after all, what former Fed Chair Paul Volcker famously did in the 1980s to get inflation under control. In 1981, the Fed Funds rate hit 19%. So why can’t we just do that now? Seems like it worked in the past, right?

Well, the macroeconomic environment is considerably different now than it was in the 1980s. For starters, in the 1980s the national debt was well under $5 trillion and debt to GDP was under 50%. In stark contrast, the national debt is currently pushing $30 trillion, and debt to GDP is, as I write, about 126%. So what happens if the Fed raises rates in this environment?

The first problem with doing so is it would make our debt more expensive to service, which, given the amount of debt we’re currently in and expect to incur in the future, is a major issue. The second problem is that GDP forecasts are being cut, and raising rates into a slowing economy risks a recession, especially when coupled with rising commodity prices. The third problem is that significantly (and quickly) raising rates is likely to torpedo the stock market. Time and time again since the Great Financial Crisis of 2008, we’ve seen the Fed step in and backstop markets. This phenomenon is known as the Fed put, which simply means the market relies on the Fed to both prop it up and catch its fall. With a record amount of household wealth in the stock market right now, it seems unlikely that the Fed would knowingly kneecap the market unless it deemed the alternative option to be meaningfully worse.

So what is the Fed’s second option? The Fed could let inflation run and try to get the debt to GDP ratio under control. This would essentially be eroding the value of our debt, i.e. inflating the debt away. The stock market would likely continue its parabolic trajectory in nominal terms. This approach has obvious problems of its own, however. Most pressing would be the harm it would inflict upon everyone already on thin margins. Buying groceries and other necessities would continue to become significantly more expensive, as wage growth would continue to lag far behind inflation. This would create a lot of political problems (remember, Jimmy Carter was the last one-term Democratic president). Additionally, it would mean deeply negative real yields on government bonds, likely causing a sell-off, which would lead yields to then rise (yields move inversely to price), which would be a problem for the Fed since it means the cost to service the debt is higher. If this scenario unfolds and the Fed has to step in and buy all the bonds to keep rates pinned at an acceptable level, that means we’re back in quantitative easing land again.

A more fundamental question may be what is the Fed actually hoping to accomplish. Luke Gromen has described the Fed as “trying to ride two horses with one ass,” meaning they’re simultaneously trying to inflate the debt away (by QE, zero interest rates, letting inflation run hot, etc.) and trying to convince everyone they’re not trying to inflate the debt away (by tapering, potentially raising rates, expressing concern about inflation, etc.).

The Fed is obviously between the proverbial rock and a hard place. Significantly raise rates (meaning something more sincere than a mere 25 bps) and risk a host of negative consequences including potentially making the U.S. government insolvent, or leave rates at zero and watch inflation wreak havoc, both financial and sociopolitical.

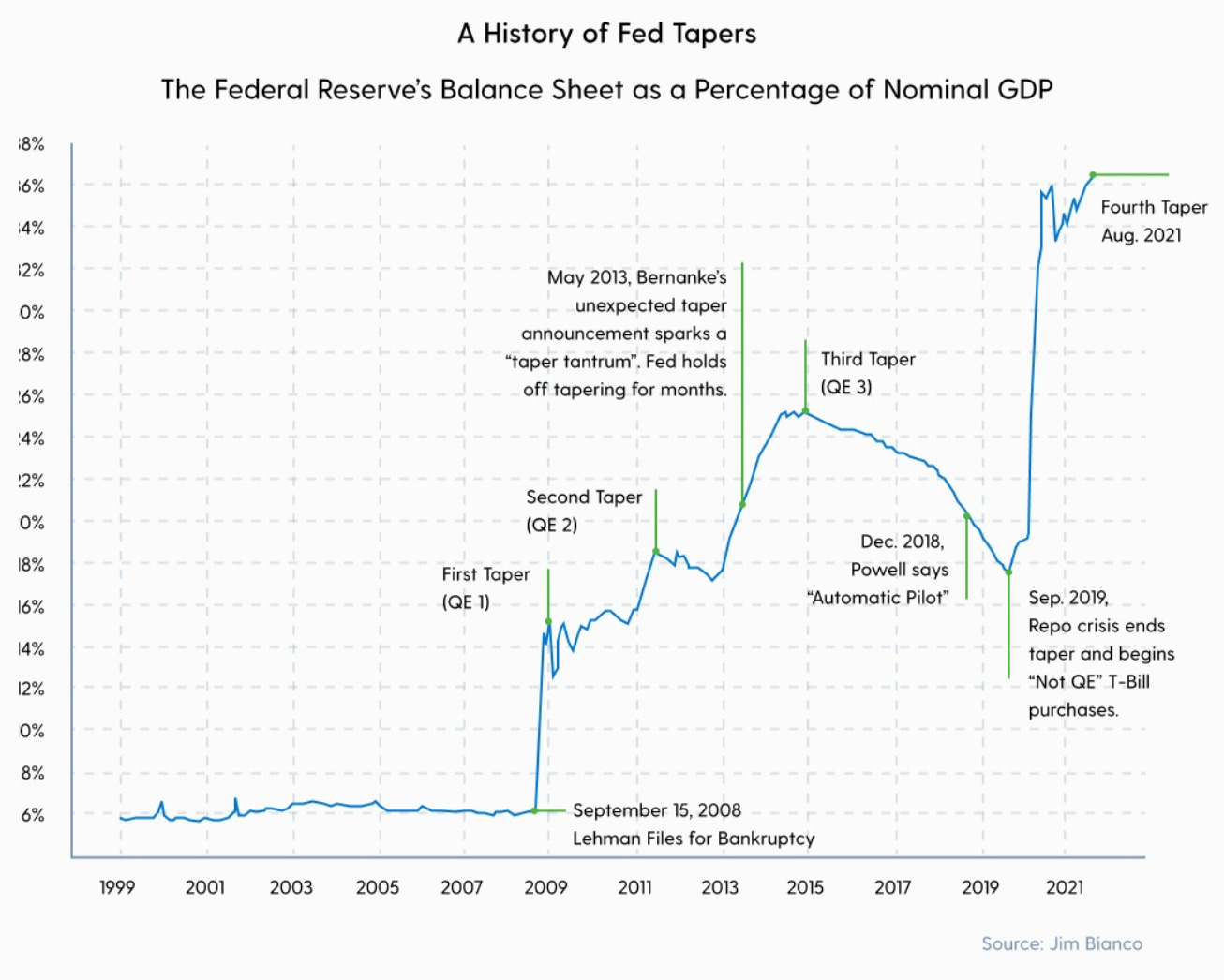

It’s worth noting that over the last 12 years the Fed has tried to taper and tighten multiple times and, in every case, they have eventually resumed quantitative easing.

(Chart credit: Jim Bianco at Bianco Research)

This chart lends credence to the idea that the Fed could attempt a tightening, if perhaps only for performative, credibility-bolstering motives. But, alas, if said tightening is too aggressive for the market’s taste, or if the Fed tightens into growing economic weakness, the consequences may (and likely will) require them to step back in as support. In other words, we may get some temporary tightening, but the long-term trajectory seems more likely to involve (require, in fact) continued support from the Fed in the form of quantitative easing and stimulus.

The last option the Fed has is closing its eyes and hoping (praying, perhaps) inflation is entirely supply-chain related and, therefore, transitory.

How this current Fed responds is also likely contingent upon who comprises its Board of Governors. Chair Powell’s current term as Chair expires in February. There’s a lot of speculation that President Biden may nominate Lael Brainard to take his place. Brainard is widely considered to be more dovish than Powell, which could mean rate hikes are undertaken more cautiously, at a slower pace, or perhaps not at all. President Biden also has three additional seats to fill on the seven-member board, as two members are retiring and a vacancy needs to be filled. If these seats are filled with folks who subscribe to modern monetary theory (commonly referred to as “MMT” and basically the idea that debt does not matter to a country who issues its own currency), we might see increasingly aggressive QE, monetization of the debt, and expansion of the money supply, which is to say more monetary inflation.

So what does this all mean for Bitcoin, long-term? If we grant that the Fed is on a stair-step trajectory of increasingly difficult decisions with increasingly severe consequences; if we further grant that no politician will get elected to implement the degree of austerity and financial responsibility required to right the ship; and, lastly, if we grant that the temptation to print money, when one has the power to do so, has never been resisted, it becomes harder and harder to see how we solve this problem within the confines of the paradigm that created it.

As Mises said, “There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

We know that “voluntary abandonment” of our current debt-driven system is a nonstarter, for reasons outlined above. So it would appear, if Mises is correct, we are heading for a painful end, though the exact timing is uncertain. The music might not stop for decades. But it will stop. We shouldn’t forget that fiat currency, as the global norm, is, from the perspective of human history, an extremely young and fragile phenomenon. It has been our reality for a mere 50 years. There is no promise, no immutable law of nature that dictates it must remain our reality for the next 50. Greater empires than the United States can trace their demise to the moment they began to clip coins and debase their currencies.

What if there’s an escape hatch from this grim future, though? What if there’s a window of opportunity for extrication before Mises’ predicted catastrophe? To make a nautical analogy, imagine our current system (the fiat system) is a ship sailing toward its own undoing. Imagine, now, that there is another ship, sailing in the exact opposite direction, away from the painful undoing and toward a restoration. There is a brief moment in time when these ships are side by side, when folks on the one may advantageously abandon it for the other. Bitcoin is this other ship.

The window of time in which to change ships advantageously will be confronted by nearly every nation, and it’s an increasingly small window because there’s game theory involved. The advantage for each successive nation that boards this ship is incrementally smaller, because early movers benefit from a lower price.

The U.S., whether its senescent ruling class knows it or not, is confronting a decision to defend the dollar at (quite literally) any and all cost or be an early mover to a new system built upon sound money. Making the latter choice preserves a global leadership role.

Countries like Laos and El Salvador are already mining bitcoin and using proceeds to fund needed public works. What if, instead of expanding the money supply and debasing the currency (which harms everyone in the long run) to fund collectively desired public programs, the U.S. started mining and holding bitcoin and using the position of financial strength this would afford to fund desired programs without inflating away the purchasing power of its citizens?

The window of opportunity exists. But it won’t exist forever.

Content Round-Up

1. “Why I Left My Legacy News Job For Bitcoin,” an article by Natalie Brunell. Brunell tells the story of her upbringing, her parents (who came to America from Communist Poland), and how she realized Bitcoin was a solution to many of the problems she observed and experienced, both as a tireless reporter and a daughter of immigrants pursuing the American Dream. She writes of the cruel vicissitudes of the boom-and-bust modern economy and its harsh effect on everyday people.

She articulates what I believe most of us intuitively understand, which is that something fundamental is broken. Politicians from both sides continue to debate what that “something” is, but it never gets fixed. Brunell argues this is because it is the money itself that is broken. This realization is what led her, and what leads many others, to discover Bitcoin.

As she writes, “until you realize our current money is broken, you will be blind to see how Bitcoin fixes it and the myriad of issues money touches.”

I can’t recommend this piece enough. Brunell has been a wonderful new voice in the Bitcoin space over the last year, and has a great podcast called Coin Stories, which is also very much worth checking out.

2. “Cathedrals,” an article by Meltem Demirors. I found this piece really thought-provoking. It’s about the importance of building something that outlasts you and the spiritual significance of devoting oneself to such a project. Demirors reminds us that most of those who worked on or financed great cathedrals knew they would likely not live to see the work’s completion and, thus, that the motivation for such an undertaking was the motivation to build something that would outlast them, something that transcended temporally-bound profit motives and aspired to more enduring satisfaction and meaning.

Cathedrals were meant to be places where people go to feel closer to something that’s larger than themselves. The difference between cathedrals and the skyscrapers of modern cities (the “cathedrals of capitalism,” as Demirors calls them) is that while the former were meant to be places people go to feel closer to something that’s larger than themselves, the latter were meant to be places people go to trade their time for money.

Demirors discusses Bitcoin as a “cathedral for the digital age.” Here’s an excerpt I love:

“While some think of Bitcoin as an asset class, I believe it is so much more. Bitcoin’s design is perfection in so many different ways - technically, socially, politically, economically. While some reject Bitcoin’s more esoteric elements to focus on the hard investment case, I believe we should embrace it. Nothing is more powerful than a shared belief system - some may call it religion - but all movements in our world are based on belief, complete with its own language and terminology, its own symbolism, and its own cathedrals.”

If you’re interested in this idea of economic systems as belief systems, check out last week’s issue of the newsletter, in which I write about exactly that:

3. “The End of Super Imperialism,” an article by Alex Gladstein. If you spend any time in the Bitcoin space you know that Gladstein’s writings are must-reads. He has spiritedly and industriously covered the global socioeconomic and geopolitical effects of dollar hegemony, as well as how Bitcoin advances human rights.

This new article is about the history of the current system of dollar hegemony. It’s long, but it’s well worth the time. You will learn a lot, I promise. I certainly did.

4. Twitter Thread: This thread is from Morgan Harper, a Democrat running for Senate in Ohio. She was formerly an advisor and lawyer at the Consumer Financial Protection Bureau, an agency dedicated to protecting consumers from exploitative financial intermediaries and whose very existence was originally proposed and urged by Senator Elizabeth Warren, a noted crypto critic. Harper, who has begun to learn about Bitcoin, notes its benefits, its inclusive promise, and its potential to challenge and disempower monopolies and gatekeepers.

5. “Bitcoin Is the Best Asset w/ Michael Saylor,” an episode of the Pomp Podcast. Anthony Pompliano sits down with Michael Saylor, and they cover everything. It’s a treasure trove of insight.

Bonus/Miscellaneous

“Bitcoin is Generational Wealth” is a 15-minute film by Matt Hornick and Tomer Strolight. This film explores the pitfalls of corrupted money and envisions what a future of sound money, i.e. a future on a Bitcoin standard, could look like. There is hope, the film argues, when money actually stores and grows your wealth, as opposed to degrading it. Check it out if you’re looking for some uplifting and visual Bitcoin content this week:

Lastly, I’m frequently asked about the cheapest place to buy Bitcoin. The answer is Strike. They charge fees so negligible as to be almost zero, and you can transfer from the app right into your own custodial wallet, whether a software wallet or a hardware wallet. You can also make payments directly from the app. If, say, you wanted to buy one of the great publications from Citadel 21, you can do so directly from Strike. Or if you want to buy some of the incredible merch from the Lightning Store, you can do so with Strike.

The only downside with Strike is there’s a $1000 limit for weekly deposits of fiat, meaning you can only deposit $1000 a week with which to buy Bitcoin in the app. So if you’re looking to make larger weekly buys, you have to look elsewhere. But if you’re looking to make smaller, regular buys with significantly lower fees than any other option, Strike is my recommendation. I have no affiliation or relationship with them. I just love their company and product.

If you sign up, you can use my referral code, which is QV2XMR.

As always, thanks for reading! If you enjoyed it or found it useful, share this newsletter widely and freely!

“Civilization is in a race between education and catastrophe. Let us learn the truth and spread it as far and wide as our circumstances allow. For the truth is the greatest weapon we have.” -H.G. Wells

See you next week,

Logan

SUPPORT

Send bitcoin to my Strike

SOCIAL

DISCLAIMER: I am not investment advisor and this is not investment advice. This is not, nor is it intended to be, a recommendation to buy or sell any security or digital asset. Nothing in this newsletter should be interpreted as a solicitation, a recommendation, or advice to buy or sell any security or digital asset. Nothing in this newsletter should be considered legal advice of any kind. This newsletter exists for educational and informational purposes only. Do your own research before making any investment decisions.

© Copyright The Why of FI.