Think Bitcoin™ Issue #1

Bitcoin advances human rights; regulation is here; what is decentralization?

Hey friends! Welcome back to Think Bitcoin™. I’m going to start using a template for these weekly newsletters to keep them nice and consistent. They’ll be broken up into “Content Round-Up,” in which I’ll share the best content I’ve consumed over the course of the week; “Headlines/News,” in which I’ll keep you up-to-date on the most important news stories relating to Bitcoin and crypto, generally; “For the New and New-ish,” in which I’ll walk through fundamental Bitcoin concepts; and “Bonus/Miscellaneous,” in which I’ll share any extra stuff I come across that’s cool or useful or just fun.

So first off, if you’re new to Bitcoin, feel free to scroll on down to the “For the new and new-ish” section for the education portion of the newsletter if you want to hit that first.

Content Round-Up:

1. “A Billion Here, A Billion There: Crypto Remittances are Suddenly Real Money” -article on 1729. One thread I always want to follow and foreground in this newsletter is how Bitcoin advances human rights and financial access by removing exploitative, rent-seeking middlemen. This article dives into the broken system of remittances and how crypto is fixing it.

2. Coin Stories Podcast: “Preston Pysh: Bitcoin for a Broken System.” Pysh, like many folks in the personal finance and FI/RE communities, developed an early admiration for the investment strategies of Warren Buffett and sought to emulate them. In fact, Pysh has actually written books about Buffett and his style of long-term value investing. In light of this background, it initially seems odd that he’s now an avid supporter of and investor in Bitcoin, but his explanation of how he got from Warren Buffett to Bitcoin is pretty compelling, and I think a lot of folks in the personal finance and FI/RE spaces will find it interesting.

The first 10 minutes are about his biography and background. The next 20 minutes are about how he got into investing; what he does now; how he came to admire and study Buffett and value investing; and why some high net-worth individuals don’t understand Bitcoin. The remainder is all about Bitcoin.

If you want to hear more about his journey from value investing to Bitcoin, he did another interview on the Business Brew podcast, in which he explains to the host how he landed on Bitcoin and why it makes so much sense.

3. “Crypto and Black Economic Empowerment” - article by Cuy Sheffield. Here’s a snippet I love:

“Crypto enables the upside of venture capital-like returns that can generate life-changing wealth that are accessible to Black consumers without requiring accredited investor status, or access to venture capital networks that have been traditionally dominated by white men in Silicon Valley. These assets are able to be passively bought or earned without minimum investments where they are liquid on 24/7 markets.

Traditionally, the path to ownership of a digital network required starting a company or having the opportunity to join a startup on the ground floor. Freelancer and gig economy jobs were limited to hourly wages without an upside in the network for which they are helping to build.

Crypto enables consumers to join or build online communities and contribute to them while owning an asset that benefits from the growth of that community. This creates the potential for generational wealth transfer to young, tech savvy, online communities who are able to identify and capitalize on new trends.”

4. “Why a Government Ban on Bitcoin Would Backfire” - article by Peter St. Onge, Ph.D. Given our discussion of regulatory developments below, this article is particularly relevant to ponder this week.

5. “Bitcoin and the American Idea” - article by Alex Gladstein, human rights reporter and activist. This article is about how Bitcoin can reinvigorate the ideals upon which America was putatively founded and from which it has since dramatically strayed.

Headlines/News:

This week is all about regulation, friends. There is A LOT going on in this area. And it’s a very fluid situation. So depending on when you read this, the situation may have evolved or changed. It’s important to note and highlight from the outset that most people (but not all) in the crypto space understand regulation of some kind is necessary for both the growth of adoption and the continued construction of the ecosystem. The fear is not regulation, writ large. The fear is hasty, un-nuanced regulation, regulation made without meaningful engagement with or understanding of the space that consequently stifles innovation (and potentially sends it offshore).

The war of narratives is also well underway.

There’s so much going here so, for both ease and my own sanity, I’m going to break it up into five buckets:

Bucket 1: The infrastructure bill

Anyone following the news in the U.S. knows that Congress is debating an infrastructure bill, which is a major piece of the Biden administration’s legislative agenda. Normally this wouldn’t really concern the crypto space. However, it came to light last week that a last-minute provision was added to the bill, which would, if ultimately enacted, have a profoundly negative effect on the crypto industry in the U.S.

Here’s what the provision in question is about. The provision’s stated aim is to ensure that the folks involved with crypto are paying taxes, an aim with which no one really disagrees. The crypto industry itself has long called for clarity on this front. But the provision changes the definition of “broker” in the tax code to include essentially everybody conducting any kind of activity in the crypto space.

Why is this a problem? “Brokers” are subject to tax reporting requirements. They have to file 1099s and report information about customers. Most folks interacting with the crypto space are not brokers by any stretch of the imagination. Miners, folks running nodes to validate transactions, software developers, hardware wallet manufacturers, etc. are not brokers. Forcing them to comply with tax reporting rules designed for brokers is forcing them to do something logistically impossible. Many of these parties don’t have customer information (or even customers!).

The crypto community, which itself has some internal divisions, swiftly unified and responded to this last-minute provision vociferously. Crypto lawyers, crypto companies, crypto associations, and various other crypto stakeholders commenced a spirited campaign to lobby Congress, mobilize the support of crypto users, and communicate the potential negative effects of the provision, if enacted.

Luckily, there are some Senators who have spent some time learning about the space. Senators Wyden, Lummis, and Toomey authored a bipartisan amendment to this provision (which I’ll call the “WLT Amendment” for short). This amendment would explicitly exclude all of the parties within the crypto ecosystem who do not perform any broker-like function from the new definition of “broker.”

As a relevant aside, we should note the odd bedfellows and new alliances crypto is beginning to create in Congress.

Anyway, things were looking good mid-week with the WLT Amendment. Senator Portman, a leader in the infrastructure bill negotiations, verbally supported the WLT Amendment, which was a significant step. The crypto community made thousands of calls to senators urging them to support this amendment.

But then the plot thickened.

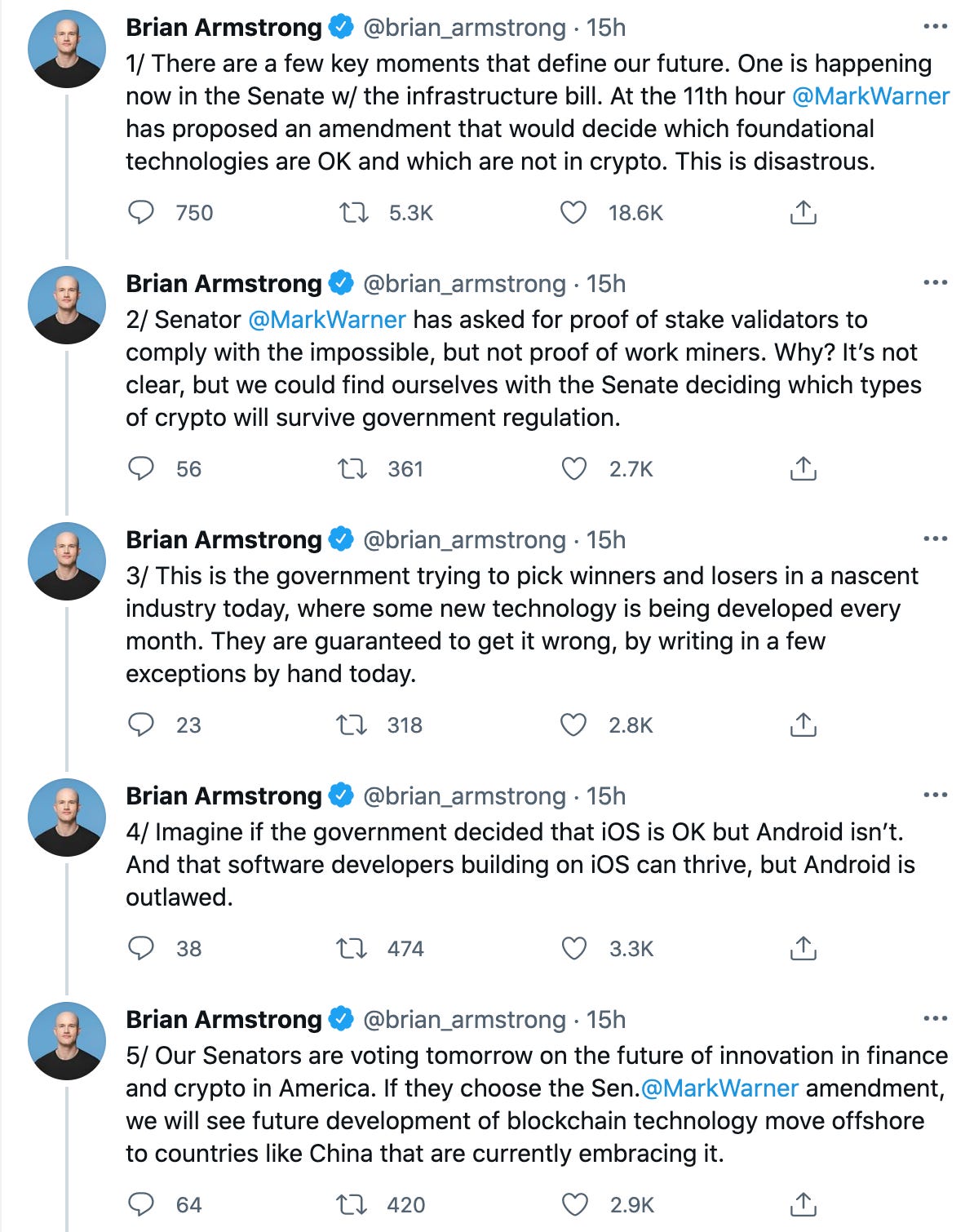

Suddenly, Senators Warner and Portman proposed a separate amendment, distinct from and competing with, the WLT Amendment (I’ll refer to the Warner/Portman amendment as the “Portman Amendment” for short). The Portman Amendment muddied the waters significantly, first by confusing validators and miners in the language itself, evincing an unsurprising and thorough lack of understanding of the space. The Portman Amendment also attempts to specifically exclude proof-of-work miners from the new definition of “broker,” while leaving proof-of-stake actors included.

We’ll get into proof-of-work vs. proof-of-stake in subsequent issues. For now, what you need to know is that Bitcoin uses proof-of-work to mine new blocks in its blockchain, while many other crypto protocols use proof-of-stake. So what it appeared Senator Portman was doing with his amendment was choosing winners and losers in the crypto space through legislation. This heavy-handed approach prompted another vociferous response, including from folks like Elon Musk and Brian Armstrong, the CEO of Coinbase. Armstrong aptly described this as comparable to Congress choosing the iPhone over the Android and not allowing any software development on the Android.

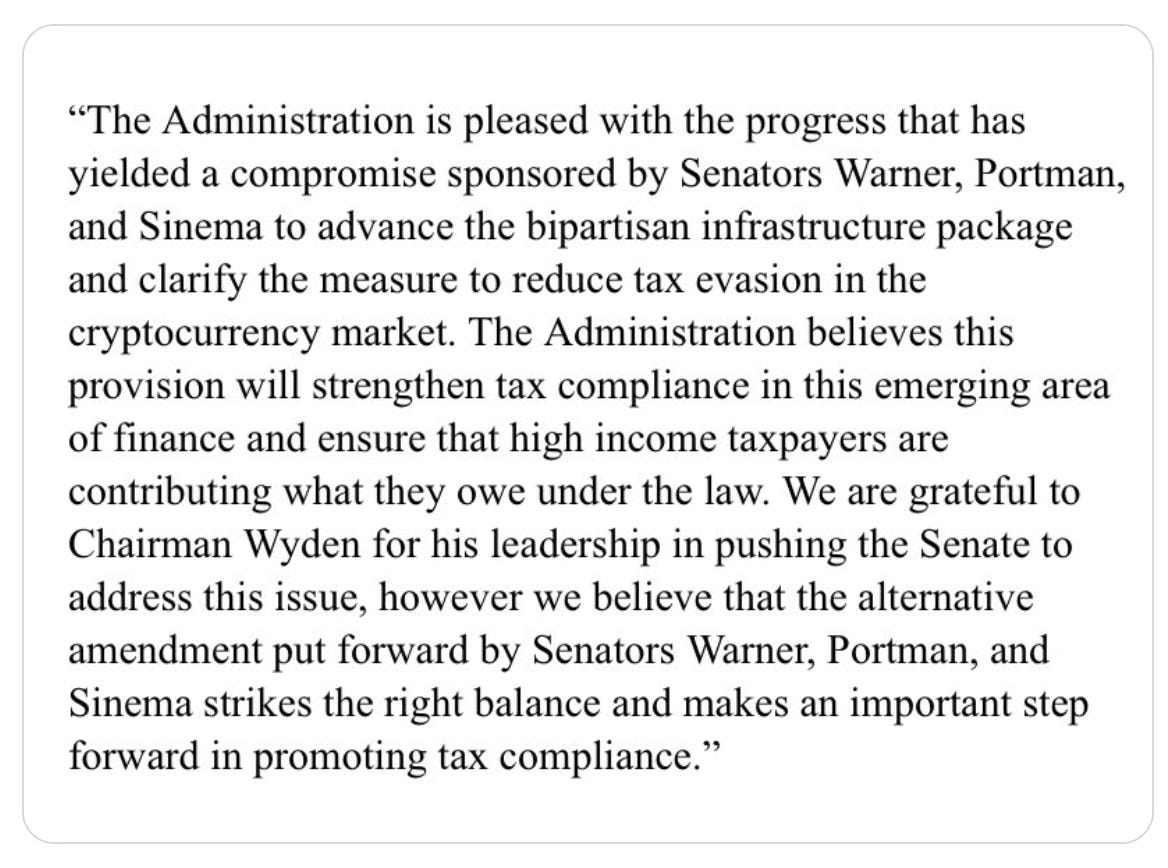

Multiple news outlets reported that Janet Yellen was lobbying senators behind the scenes to support the Portman Amendment, with support from the Biden administration. The Biden administration released this statement:

Like the Portman Amendment itself, this statement reveals an anemic understanding of how crypto works and misidentifies the issue being debated. It’s important to reiterate that the crypto space is not arguing for exemption from taxation, nor is the space arguing that actors who perform broker-like functions shouldn’t be subject to tax reporting requirements (entities like Coinbase, Gemini, etc.). In fact, these entities have actively lobbied for clarity on their reporting requirements and have expressed explicit, unequivocal willingness to comply with those requirements. The crypto space is simply arguing that the definition of “broker” should not be so broad as to encompass actors in the space who perform no function even remotely resembling a broker-type function and for whom broker-like tax reporting requirements are logistically impossible.

In other words, the crypto space is arguing for smart, nuanced regulation that puts the right burdens on the right parties. Tax compliance and fostering innovation need not be mutually exclusive. The crypto space is also urging Congress to take the time to learn about these new technologies before drafting legislation that would stifle their growth.

So two competing amendments hit the Senate floor for debate, the WLT Amendment seeking to do the least amount of harm to the space by excluding non-broker-like actors from the definition of “broker,” and the Portman Amendment attempting to exclude only proof-of-work mining, while leaving proof-of-stake covered. For those unfamiliar, note that Ethereum, the second largest cryptocurrency and crypto ecosystem, is in the process of moving to a proof-of-stake protocol. Cardano, the fourth-largest cryptocurrency by market cap, is also proof-of-stake. So the Portman Amendment really matters for the future of development within these ecosystems.

An additional amendment was then made yesterday (Saturday) afternoon which specifically excluded both proof-of-work and proof-of-stake consensus mechanisms from the definition of “broker.” This leaves out a number of other consensus mechanisms used by different crypto protocols, and potentially includes consensus mechanisms that have not even been conceived yet. We’ll talk about what a consensus mechanism is in a subsequent issue, so don’t worry if that phrase throws you right now. The main point, simply put, is that this new, competing amendment would potentially limit innovation in the space, as proof-of-work and proof-of-stake are not the only two ways to do things.

The crypto community has continued to lobby hard for the WLT Amendment. As I write, currently, a vote on the infrastructure bill seems set for tonight, and this all remains very fluid. Senator Hagerty, as I write, is actually holding up the entire process because he doesn’t believe the bill is actually paid for. So we’ll see how this all goes. But getting the crypto amendment/provision correct is a major sticking point, something no senator, no reporter, and no seasoned lobbyist in D.C. could have predicted beforehand.

And this is precisely why, in my opinion, the major takeaway of all this is that crypto has affirmatively, emphatically arrived as a force to be reckoned with in Washington D.C. The idea that one of the biggest items on the legislative agenda of a United States president could be held up by debate over a provision relating to cryptocurrency or that United States senators (some of them at least) would be spending weekends discussing the details of how consensus mechanisms work, would have been utterly unfathomable a mere six months ago.

Moreover, the response of the crypto community to the initial provision put everyone on notice that there is a new constituency politicians ignore or demean at their very real peril: the crypto constituency. And these folks may have differing views on other issues, perhaps even divergent views on some, but they are united in their belief that crypto is a societally transformative technology, something worth protecting fiercely, and something worth fighting for. This cannot be understated.

Whatever the vote turns on the aforementioned amendments turns out to be later today, these debates, discussions, and skirmishes with legislators are sure to continue. In the case of the infrastructure bill, it’ll move to the House of Representatives. If eventually signed into law, any unfriendly crypto provision would almost certainly then be challenged in the courts.

Whatever happens, I’ll be following it here.

Bucket 2: Gary Gensler, the SEC Chair, makes comments about which digital assets may be securities.

On Tuesday, August 3, Gary Gensler gave a speech at the Aspen Security Forum about crypto and the frameworks the SEC may employ when considering how to regulate the space. It’s important to remember that Gensler actually taught a course on cryptocurrencies and blockchain technology at MIT. These lectures are available on YouTube and are quite good. So, unlike the overwhelming majority of Congress, Gensler is someone who understands the technology behind Bitcoin.

In fact, Gensler spent the first part of his speech waxing poetic about the invention of Bitcoin and the genius of its pseudonymous creator, Satoshi Nakamoto. Discussing his teaching at MIT, he said, “in that work, I came to believe that, though there was a lot of hype masquerading as reality in the crypto field, Nakamoto’s innovation is real. Further, it has been and could continue to be a catalyst for change in the fields of finance and money.” So this is a regulator with respect, even admiration, for Satoshi and for Bitcoin as a technology.

However, Gensler was quick to note that though he may admire the technology, he’s “anything but public policy-neutral.” He highlighted the SEC’s mission, core to which is investor protection, and opined that “we just don’t have enough investor protection in crypto,” before comparing the space to the “Wild West.”

Most interestingly (and troublingly), he said that many of the tokens being offered and sold in the crypto space are securities. And, for all non-lawyers out there, this is an important legal categorization. Any sale of securities has to be registered with the SEC or fall under an exemption to registration. Selling unregistered securities is illegal.

The issue of whether various cryptocurrencies are securities has been a relatively dormant one for a few years. Former SEC Chair Jay Clayton has previously stated that bitcoin is not a security. Gensler appears to agree with Clayton here. But Clayton was vocal about considering more or less every other token a security, and Gensler noted he generally agrees here, too.

And this comes down to the legal definition of a “security.”

The legal definition of a “security” comes to us from a 1946 U.S. Supreme Court case called SEC v. W.J. Howey Co. Earlier, in the 1930s, the SEC defined securities as a whole list of things, including stocks, bonds, notes, etc. One of the items on the list was something called an “investment contract.” The Howey case defined “investment contract,” stating that an investment contract exists when “a person invests his money in a common enterprise and is led to expect profits solely from the efforts of the promoter or a third party.” This decision has been reaffirmed a bunch of times.

So the Howey Test for an investment contract has four parts:

1. an investment of money

2. in a common enterprise

3. with the expectation of profit

4. to be derived from the efforts of others

If all four parts are satisfied we have an investment contract, which is a security. Gensler’s speech indicates that he has his sights set on the decentralized finance (DeFi) space and tends to think many non-bitcoin tokens satisfy the Howey Test, making them securities.

What separates Bitcoin from almost every other cryptocurrency is that Bitcoin never had an initial distribution of coins or an initial coin offering or anything like that. The first bitcoins were mined in the genesis block by Satoshi. We’ll talk about mining in subsequent issues, but the important distinction is that the first bitcoins were not just handed out to developers or given to investors in exchange for capital or offered to the public in an initial coin offering (which would seem to satisfy a few prongs of the Howey Test). They were mined, just like every bitcoin since.

Now, Gensler’s position is not the only position within the SEC. Hester Peirce, an SEC Commissioner and crypto ally, proposed a “safe harbor” rule for crypto projects earlier this year. This proposal would give projects a three-year grace period to become truly decentralized or functional, after which period projects failing to meet these standards would have to comply with existing securities laws. The proposal would also protect crypto investors by retaining anti-fraud provisions. Peirce has responded to Gensler by inviting him to collaborate on thoughtful ways to protect investors while still fostering innovation.

There’s another layer of intrigue to this Gensler development, however, and that’s the way in which the Commodity Futures Trading Commission (the CFTC) has stepped up to assert its authority over cryptocurrencies. Their position is that cryptocurrencies are commodities (not securities) and fall squarely within their domain, as opposed to the domain of the SEC. CFTC Commissioner Brian Quintenz, in response to SEC Chair Gensler’s speech this week, has been very vocal about this. And both Gensler and Quintenz seem to be responding to Janet Yellen and the Treasury Department who, at the urging, of lawmakers like Elizabeth Warren, seem to be not-so-subtly wading into the crypto regulation debate. So, in some ways, it seems like there’s a lot of territory-marking going on.

In any case, there’s obviously a lot at stake here. Both the SEC and the CFTC are more knowledgeable about crypto than the Treasury Department, which is comparatively (and at times, demonstratively) clueless. The CFTC has more experience and has been engaging with the crypto space more meaningfully for a longer time than the SEC. So we’ll see how this develops. But make no mistake, these legal classifications have important ramifications. Whether certain tokens are commodities or securities (or neither) matters. Again, selling unregistered securities is illegal, and compliance with the SEC is quite expensive.

Bucket 3: The Beyer bill and accusations it was Janet Yellen behind its authoring (are you seeing a theme here?)

I don’t want to spend too much time on this one since (1) this issue is getting a bit lengthy already and (2) this is still developing. Representative Don Beyer of Virginia, someone who has heretofore never demonstrated any interest in crypto, introduced a bill called the “Digital Asset Market Structure and Investor Protection Act,” which apparently seeks to create a pretty exhaustive regulatory regime for digital assets, attempting to define which ones are securities, which are commodities, wading into tax compliance, and more.

Everyone in crypto thought it was a bit weird that a congressman who has never expressed any interest with or demonstrated any knowledge of crypto would all the sudden come out with a bill like this. But then it was suggested by another congressman that perhaps Janet Yellen had tapped him on the shoulder, as a friend of the administration, to draft such a bill.

This bill will almost certainly get torn apart in the House, which has many friends of crypto. So it’s too early to get bothered about it and, frankly, there are much more pressing regulatory battles being fought at the moment.

Bucket 4: BlockFi’s legal peril

In another iteration of the what-are-securities morass, BlockFi, a crypto lending platform that offers crypto-interest-earning savings accounts, is finding itself in the regulatory crosshairs. Five states, as I write this, have alleged BlockFi’s interest-bearing accounts violate state securities laws. BlockFi for its part, has consistently maintained that it is not violating any such securities laws. We’ll keep an eye on this story.

Bucket 5: The battle of the narratives

In addition to the battles being fought over regulation and legislation, there’s a battle of narratives going on, as well, with some lawmakers seeking to shape the public perception of crypto.

Elizabeth Warren is a prime example of this. Two weeks ago, in a Senate hearing, she criticized crypto as being controlled by “shadowy super coders” who were no better than big banks. Senator Sherrod Brown chimed in on what he called crypto’s “phony populism.” Besides being factually incorrect, at least with respect to Bitcoin, these narrative jabs seem deeply misguided coming from folks, like Warren, who have spent entire careers excoriating financial intermediaries for exploitative behavior and fighting for increased financial access. Bitcoin removes financial intermediaries and allows anyone with a cell phone to bank themselves. In other words, Bitcoin effectively accomplishes, via its technology, what folks like Warren have been trying for years to accomplish via lawmaking, namely increasing financial access, removing exploitative intermediaries, and advancing economic justice.

And I’d be remiss if I didn’t point out, in response to Warren’s “shadowy super coders” allegation, that Bitcoin is not controlled by anyone or any group. No one controls Bitcoin. That’s just not how it works. It works on a decentralized consensus mechanism. Perhaps Senator Warren was aiming her ire at other crypto protocols, or perhaps she hasn’t done sufficient homework to understand Bitcoin. I suspect it’s the latter.

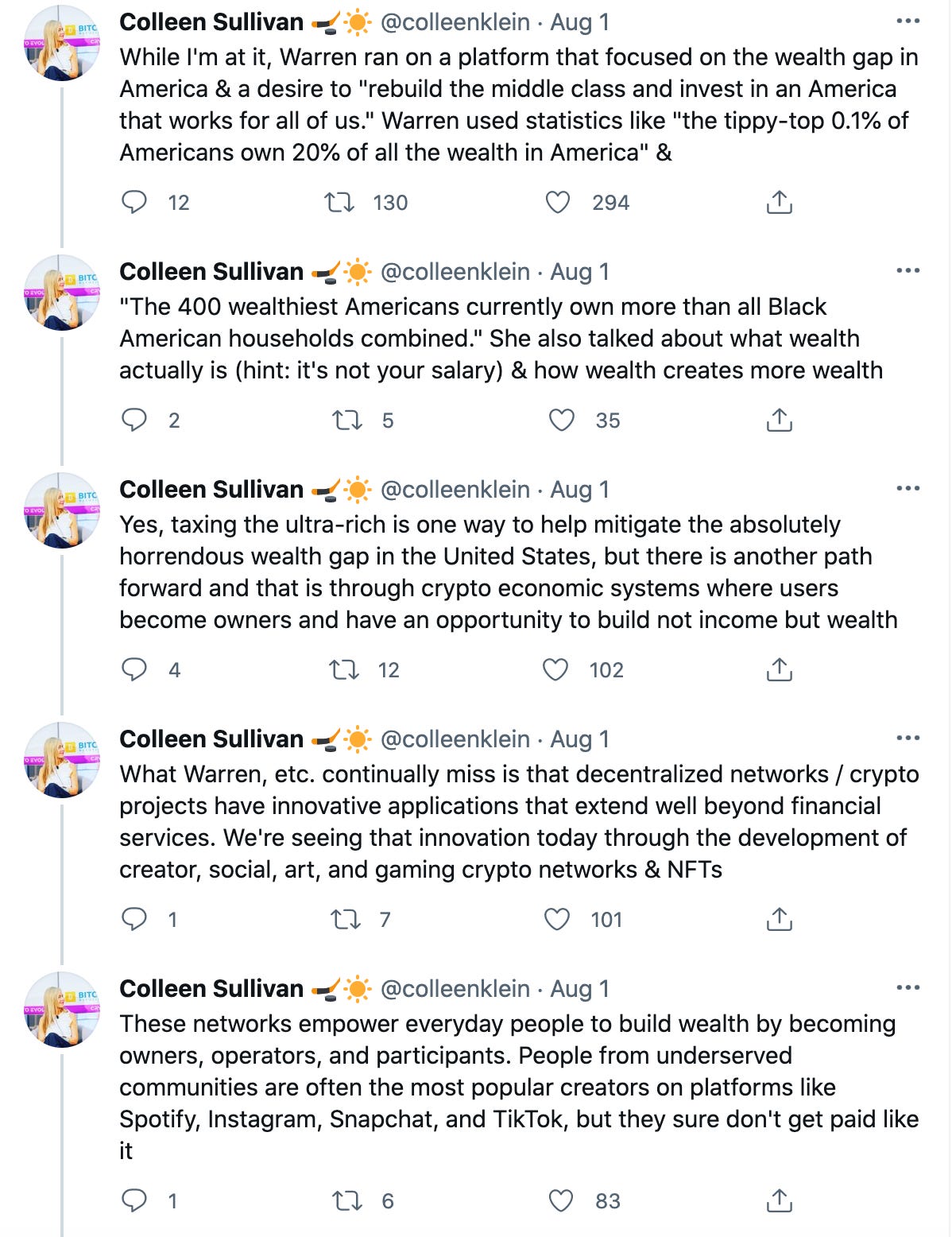

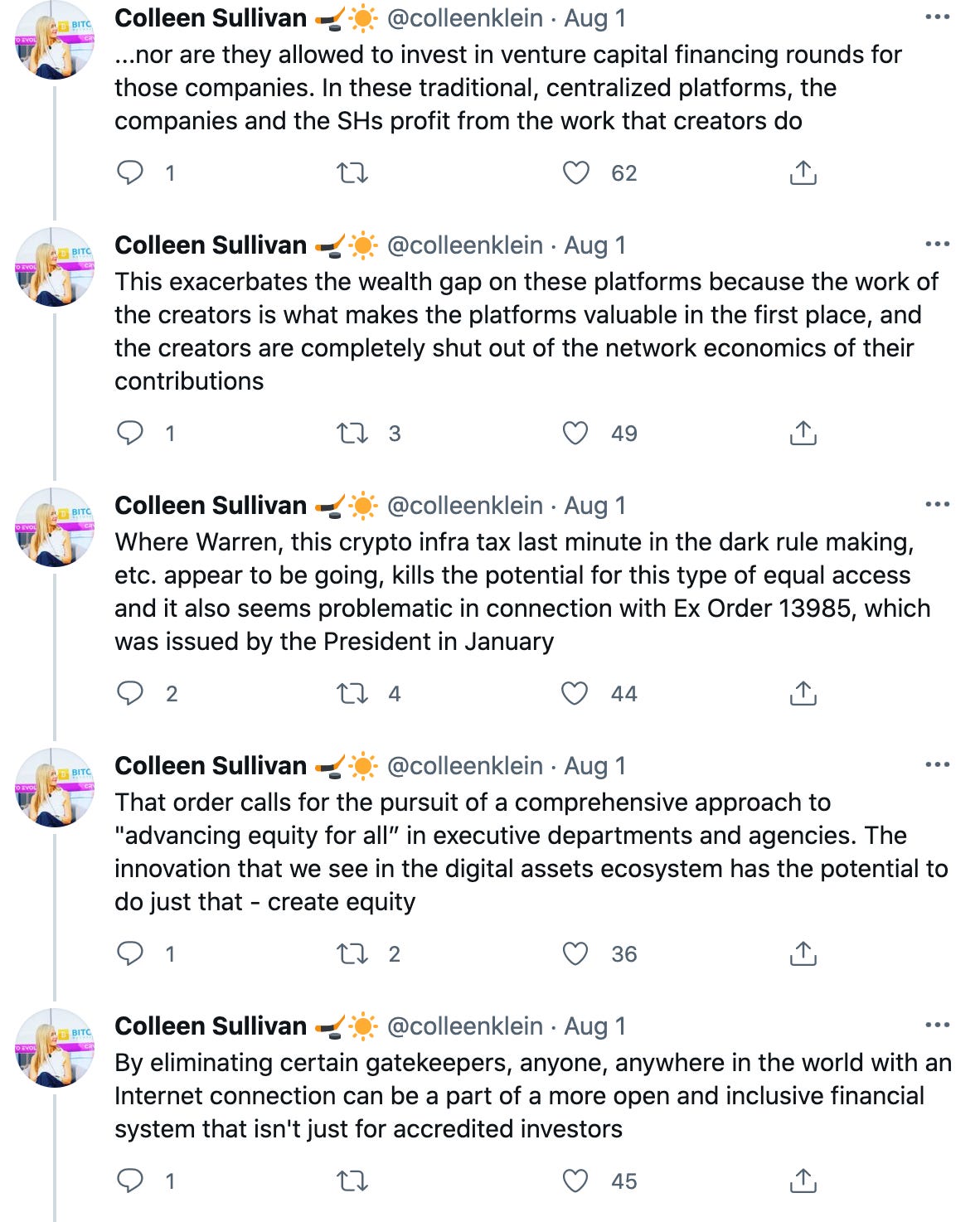

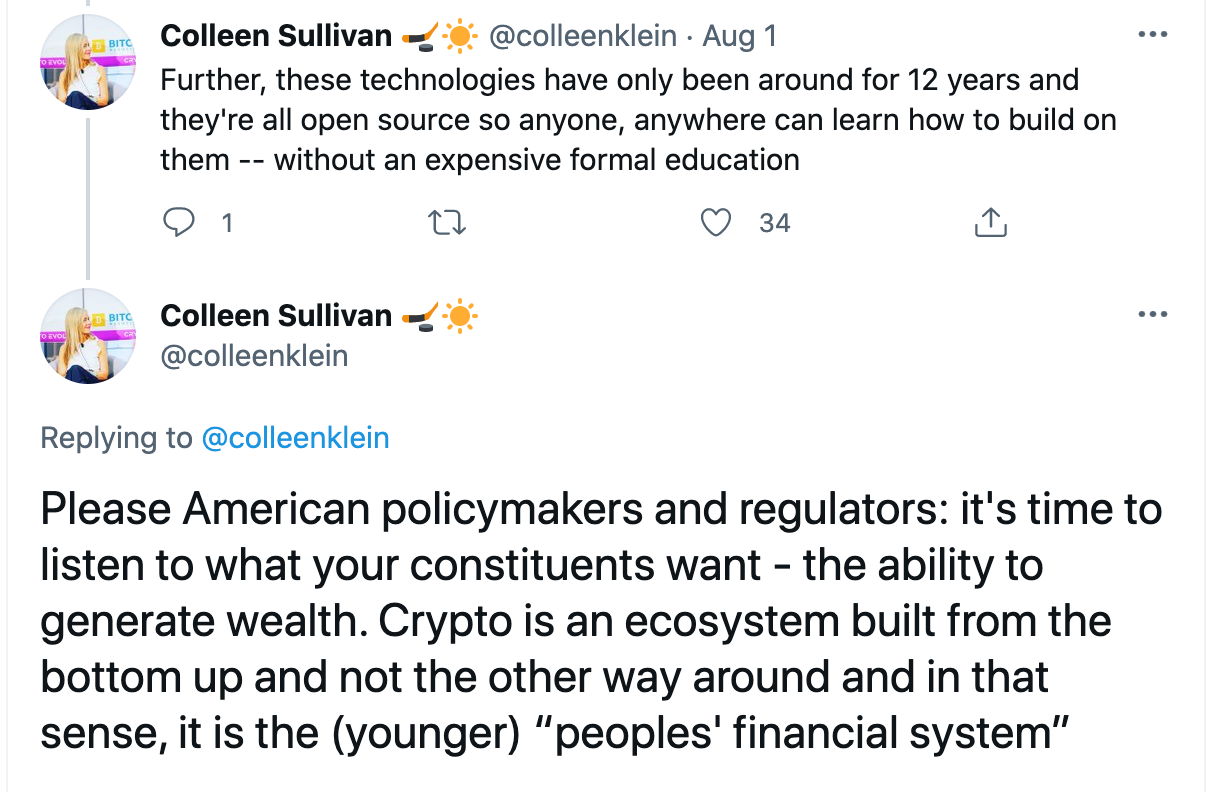

Warren’s comments generated a lot of responses. I think this one from Colleen Sullivan, co-founder and CEO at CMT Digital, is pretty accurate:

She goes on to reference the Cuy Sheffield article I flagged earlier in the content section. I would also direct folks to the work of Isaiah Jackson, author of Bitcoin and Black America, and Najah Roberts. In sum, and without dwelling on it too much, Senator Warren’s vehement opposition to Bitcoin and crypto is under-researched and, frankly, somewhat surprising, given her seeming devotion to ideas that Bitcoin actually advances.

Taken as a whole, I think all this regulatory news underlines and affirms the fact that crypto is here to stay, and regulators want to bring it within the parameters of public policy in various ways with varying intentions and motivations. Bitcoin, specifically, and crypto, generally, are no longer confined to a niche community on the internet. There are between 10 and 50 million crypto holders in the U.S. and over 220 million users worldwide. Governments and regulatory bodies have finally taken notice in a big way and want to exert control.

It’ll be fascinating to see how this all unfolds, and you can bet I’ll be covering it all here in the newsletter.

For the new and new-ish:

Alright, so let’s get started here. If you missed last week’s issue, there are two videos from an organization called Hello Bitcoin in there, which are pretty good, short intros that help you get a sense of Bitcoin’s value as a technology.

As I mentioned in the first issue, I want this section of the newsletter to essentially be an educational progression from zero to Bitcoin knowledge. So each week we’re going to walk through some fundamental concepts, each building on the next, each including some vocabulary that’ll be useful throughout.

Now, I think there are two distinct roads down which to proceed when it comes to understanding Bitcoin. These roads eventually intersect, but in terms of conceptually organizing the content we consume and marking the process of our understanding I think it’s helpful initially to think of these two roads as distinct, but equally important, starting points. They are:

1. Technology – Meaning, what actually is Bitcoin? How does it function? What problems is it addressing? What service does it seek to provide?

2. Macroeconomics – Meaning, how does Bitcoin fit into the global economy and why is it important?

We’re going to proceed down both of these paths. For some of you, one might click and resonate more than the other. For me, personally, the macroeconomic piece really clicked. The technological piece was more difficult.

We are going to start with the technological piece to get a basic understanding there. After all, before we go any further, we should at least be able to answer what Bitcoin is and what it does. So we’ll begin that process today by talking about decentralization and ledgers.

And I know this sounds boring, but I promise, bear with me and the value will become apparent.

BUT FIRST.

Some history. Where did Bitcoin come from? How did it start? Who invented it? Bitcoin was invented in 2008 by a person or group of persons using the pseudonym, Satoshi Nakamoto. Nobody knows the real identity (or identities) of Satoshi, and Satoshi hasn’t been heard from since 2011.

In 2008, Satoshi published a whitepaper on Bitcoin, which described this newly invented peer-to-peer system of electronic cash. Peer-to-peer means without a middleman/intermediary. In other words, I can transact with you without going through, for example, my or your bank as an intermediary.

Satoshi’s invention came in the wake of the financial crisis and the subsequent bank bailout. In emails, he/she/they stressed that the current financial system is based entirely on trust of centralized entities.

Satoshi said the following:

“The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve. We have to trust them with our privacy, trust them not to let identity thieves drain our accounts. Their massive overhead costs make micropayments impossible.”

Now, there’s a lot to unpack here. But let’s start by stating, in simplest terms, what Satoshi wanted to do with Bitcoin. The aim, put simply, was to remove “trusted” intermediaries from transactions (and from the system, generally) because these intermediaries wield too much power and have repeatedly betrayed our trust in myriad ways. Put even more simply, Satoshi’s aim was to remove the middlemen.

It’s important to note that Satoshi says “the central bank must be trusted not to debase the currency…” This is getting a little bit ahead of ourselves, but just as a teaser of things to come, how might the central bank debase the currency, and what does that even mean? The central bank debases the currency when it increases the money supply and when it performs quantitative easing. Satoshi saw this happening in 2008 with the bailouts, but he/she/they could never have predicted the historic increase in the money supply in 2020 as part of the response to COVID-19. Increasing the money supply makes the money in existence worth less, thereby debasing the currency and decreasing its purchasing power. Let’s leave this macroeconomic thread alone for now, though. We will pick it up again later when we discuss what makes Bitcoin valuable.

Back to the idea of trust and trusted intermediaries. Satoshi notes that we have to trust banks with our deposits, but banks lend those deposits out. In other words, banks don’t actually hold the dollars you deposit. Banks have what are called fractional reserves, meaning they only hold a fraction of actual deposits. So, if every person went to his or her bank tomorrow and asked for all of his or her cash, the banks could not honor those requests.

We also trust banks to protect our privacy.

Why do we give banks, these trusted, centralized intermediaries, so much power? Well, they control the ledgers of our transactions. The majority of transactions now take place with credit cards or through things like PayPal, Apple Pay, etc. Our money essentially exists as an electronic ledger maintained by our banks. I pay you $10 electronically, and I trust a bank to make an entry onto my ledger subtracting $10. You expect yours to make an entry to your ledger adding $10.

At a fundamental level, Bitcoin is a technology enabling the removal of intermediaries that manage ledgers in a centralized way. Instead of having to go through a bank, which controls ledgers, folks can transact directly.

The first question that should pop up into your head is, well, that sounds great, but who holds or manages the ledger(s) then?

And this is where decentralization enters the picture. With Bitcoin, every member of the network holds a copy of the ledger of transactions, which is just a long chain of blocks called a blockchain, with each block holding a certain amount of transactions that have been verified. Instead of banks holding huge databases of our transactions, everyone in the Bitcoin network holds a copy of this long, constantly growing chain of transactions. Instead of a central party holding this giant ledger, ownership is decentralized, meaning everyone has a copy.

The “network” is everyone running what’s called a Bitcoin node, which is used to verify transactions. We’ll get into nodes in a subsequent issue. For now, what you need to know is that Bitcoin removes the centralized trusted intermediary. Instead of these centralized entities being trusted with all the ledgers of transactions, one ledger is kept by an entire network of users, a network anyone can join.

In other words, no one individual or single entity “controls” the Bitcoin network. Each node in the network holds the same ledger, and this ledger is open and transparent.

Removing the middleman may sound like a horrible idea to you. But think for a moment about how these centralized intermediaries have financialized the world. Think for a moment about the truly immense power they wield. Think about the financial crisis of 2008. Think about the hundreds of millions of dollars in settlements these intermediaries have paid out as a result of racial discrimination, predatory lending, and fraud.

But still, removing the middleman creates problems. And this is because we trust these intermediaries. I don’t mean this casually. I mean we trust them to maintain ledgers of transactions because we don’t feel like we can trust each other. For example, if I go to a store and buy $50 worth of groceries using my debit card or Apple Pay or something like that, trust is placed in a centralized ledger-keeper to deduct that $50 from my account. Otherwise, what’s to stop me from trying to spend that same $50 at another store? And then again at another? The middleman keeps track of each transaction to ensure I don’t do that. We, as a society, place this great trust in these middlemen. Centralization, it seems, is necessary.

So when we remove the middlemen – when we decentralize - where or who do we trust to keep the ledger? If we trust a single party or set of parties, we’re still relying on centralized intermediaries. But how can we have any trust with no centralized intermediaries? How can we possibly trust each other? How can we trust parties we don’t know? Parties with bad intentions? A host of problems present themselves. We may not love giving financial intermediaries so much power, but what is the alternative? We have to trust some central, “objective” third party, right?

Satoshi looked at this problem and said well, what if we could create a system where trust is not required at all? In other words, how can we create a system where no one needs to trust anyone? How would we do that?

We’ll dive into the ways Bitcoin solves this problem next time. The big takeaway today is that Bitcoin is fundamentally about creating a system with no centralized intermediaries, a system in which trust is not required to transact.

Bonus/Miscellaneous:

Megan Thee Stallion explains Bitcoin.

In doing so, she correctly and poetically states, “Like a wild stallion, it can’t be controlled by anyone.”

Thanks for reading, this week! I know we covered a lot, but hopefully you found it useful. Obviously this newsletter takes me quite a bit of time to research and write. I’d love if you could share it with anyone you think might be interested. Maybe you have friends who are crypto-curious, maybe you have family members who ask you about Bitcoin, maybe you have coworkers who are into FI/RE. Share this widely and freely. The goal of this newsletter is to spread knowledge, education, and interest in Bitcoin (and crypto, generally) to as many people as possible. Let’s grow this space and get this into as many hands as possible.

Never stop learning.

See you next week,

Logan

DISCLAIMER: I am not investment advisor and this is not investment advice. This is not, nor is it intended to be, a recommendation to buy or sell any security or digital asset. This newsletter exists for educational and informational purposes. Do your own research before making any investment decisions.

Copyright The Why of FI.